Last month, Fortune released its list of the top 50 businesspeople of the year. The recognition these CEO’s are receiving shows that the market cares about ROIC, even if many investors aren’t explicitly talking about it.

Both LF and ECL have seen significant bottom line growth in the past two years. However, the differences in the way the two companies achieved their growth and in their respective valuations make LF one our Most Attractive Stocks and ECL one of our Most Dangerous.

For a while, EA appeared to have cracked the code in the middle part of this decade. By delivering sports franchises like FIFA and games like The Sims, the company saw profits and returns on invested capital (ROIC), which peaked at 93% in 2004, grow to enviable heights. Unfortunately, that strategy has proven unsustainable as ROIC has plummeted.

November sees 13 new stocks make our Most Attractive list and 19 new stocks fall into the Most Dangerous category. Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

October sees 13 new stocks make our Most Attractive list and 16 new stocks fall into the Most Dangerous category. Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

The stock has been beat up since its much-hyped IPO in 2011, but even after losing 61% of its value the stock is still too expensive. ZNGA is competing in an immature market where the barriers to entry are almost nonexistent and brand loyalty is a foreign concept.

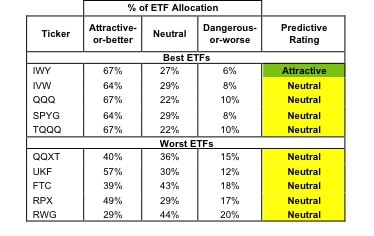

The large-cap growth style ranks second out of the twelve fund styles as detailed in my style roadmap. It gets my Neutral rating, which is based on aggregation of ratings