Our Most Attractive and Most Dangerous stocks for November were made available to the public at midnight on Monday. Last month saw some strong performances from our picks. Universal Insurance Holdings (UVE) led the way for our Most Attractive stocks by gaining 12% in October. Deluxe Corporation (DLX) was our top performing Large/Mid cap with a 10% gain. On the Dangerous side, Healthways Inc. (HWAY) dropped by a whopping 47% while Bankrate (RATE) fell the most among the Large Cap stocks with a 20% drop.

The two stocks we highlighted in last month’s announcement both outperformed. Dun & Bradstreet (DNB) rose by 4.5%, while Sina (SINA) declined by 3.7%. The S&P 500 rose 3.7% last month. DNB remains on the Most Attractive list for November and SINA is still one of our Most Dangerous stocks.

November sees 13 new stocks make our Most Attractive list and 19 new stocks fall into the Most Dangerous category. Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

Most Attractive Stock Feature for November: CF

CF Industries Holdings (CF) is one of the new additions to the Most Attractive list this month. CF made the list due to the decrease in the attractiveness of other stocks on the list.

CF is a cash-flow-generating machine. CF has had a free cash flow yield of over 10% in four out of the past five years. The lone exception was in 2010 when CF acquired nitrogen fertilizer producer Terra Industries. CF’s steady cash flow generation allowed the firm to accrue $2.2 billion in excess cash (over 17% of the stock’s market cap). Large cash piles can be a point of concern for companies with low ROIC and poor track records of value creation. For a company like CF, they represent strategic flexibility and dividend potential.

CF has an ROIC of 27%, the highest of any agricultural fertilizer company that we cover. Over the past five years, CF has more than doubled its after tax profit (NOPAT) margin, from 15% in 2007 to 33% in 2012.

CF’s results have not been great this year due to the declining nitrogen market. The stock price fell sharply last week due to disappointing third quarter results. Some may see this fall as a warning sign, but we see it as a buying opportunity. At its current valuation of ~$220/share, CF has a price to economic book value ratio of only 0.6, which implies that the company’s NOPAT will permanently decline by 40%. CF is a large, stable company with a history of profit growth. Even with its declining profits this year, the company appears nowhere near incurring a permanent 40% decline in profits. The stock is priced for a worst-case scenario.

A strong track record of profit growth and extremely low expectations embedded in the stock valuation make CF one of our Most Attractive stocks for November.

Most Dangerous Stock Feature for November: EA

Electronic Arts (EA) is one of the new additions to the Most Dangerous list this month. EA made the list due to the 2.5% stock price increase last month that made its valuation even more dangerous.

As I wrote in September about Zynga (ZNGA), mobile gaming stocks are dangerous plays. The industry has almost no barriers to entry, and the success and failure of games can be very unpredictable. Unlike the console gaming industry where the large developers dominate and long running franchises rake in millions, new popular mobile games seem to come out of the woodwork every week.

EA has admittedly done better than most other console game developers at making the switch to mobile. It has created digital versions of popular games like FIFA and The Sims as well as original mobile games such as Plants Vs. Zombies.

On the other hand, EA has done a poor job at listening to and addressing the desires of its consumers. Readers of The Consumerist recently voted EA the worst company in America for the second straight year. Gamers continue to be unimpressed by the company’s poor customer support and attempts to get players to make in game purchases with real money.

In the short term, EA’s growing mobile revenue has failed to stem the decline from its console business. In the long term, EA’s unpopular practices and inability to respond to the demands of its customers could cost the company millions.

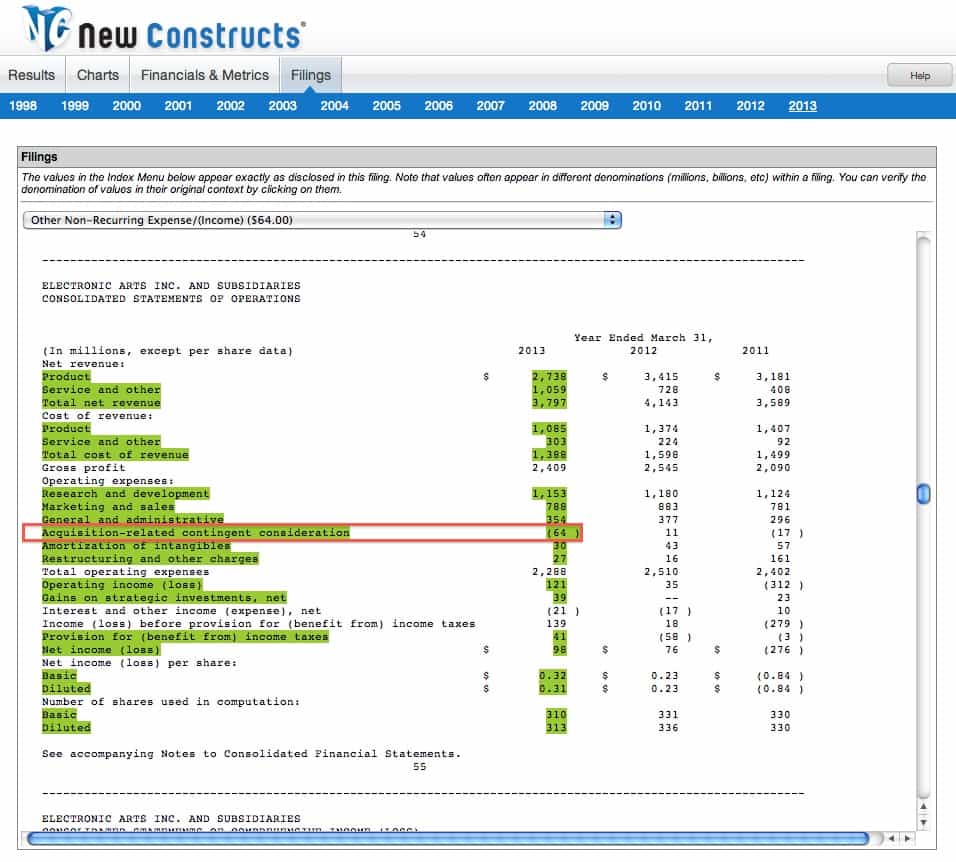

EA managed to retain the illusion of growth in the last fiscal year due to some creative accounting. The company recorded $64 million in pre-tax income due to a change in the fair value of contingent considerations. What this means is that EA acquired multiple companies and agreed to pay an extra amount if the companies met certain performance targets. In the last year, the probability of meeting the performance targets decreased, so the contingent consideration liability decreased, which EA was able to book as income. Essentially, EA reported $64 million of nonexistent income due to the underperformance of companies it acquired.

{kind=link}

After removing the contingent consideration income and other unusual items, we reveal that EA’s true operating profit (NOPAT) actually declined by 33% while reported earnings rose 38%. Investors need to look beyond the reported earnings to find the true profitability of a company.

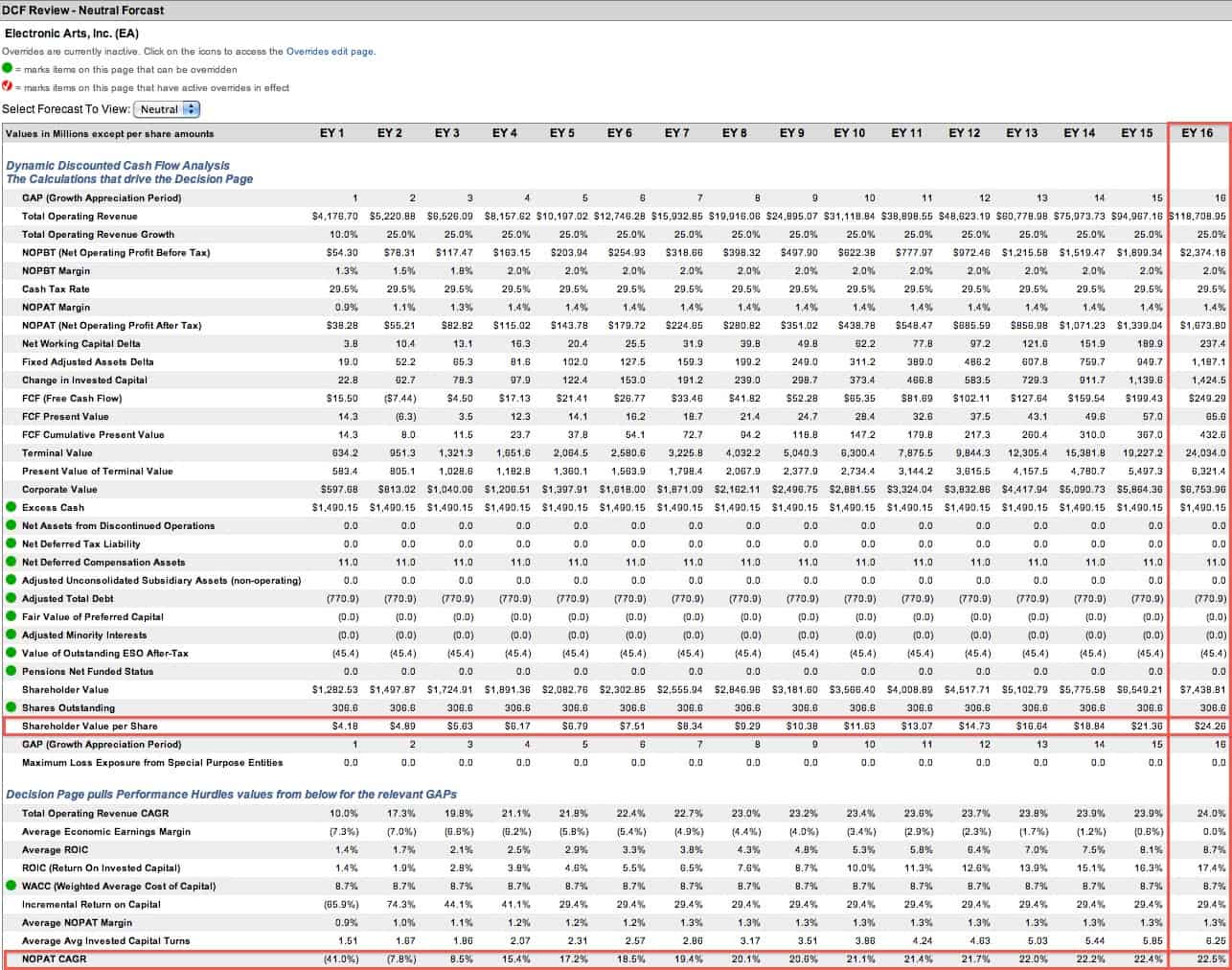

Even if mobile games turn into a huge success for EA, the company will still be hard pressed to fulfill the massive expectations embedded in its stock price. EA’s current valuation of ~$25/share implies that the company will grow NOPAT by 23% compounded annually for 16 years. EA is priced for the best-case scenario, which leaves little upside for the stock and a great deal of downside potential.

{kind=link}

Misleading earnings, poor public image, and a sky-high valuation lands EA squarely on our Most Dangerous Stocks list.

The Most Dangerous Stocks report for November can be purchased here, while the Most Attractive Stocks can be purchased here. To gain access to these reports one week earlier each month, e-mail us at subscriptions@newconstructs.com to request a subscription.

Sam McBride contributed to this report.

Disclosure: David Trainer owns CF. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.