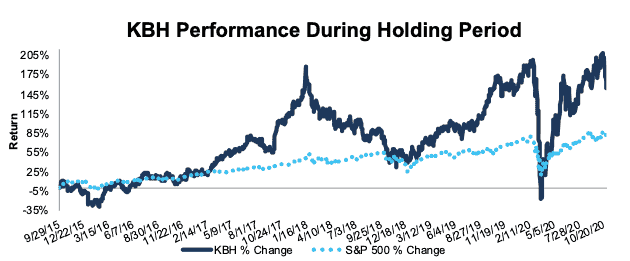

KB Home (KBH) – Closing Short Position – up 155% vs. S&P up 80%

We put KB Home (KBH: $34/share) in the Danger Zone on September 29, 2015. At the time, KBH received a Very Unattractive rating. Our short thesis noted the firm’s declining economic earnings, lagging profitability in a competitive market, and overvalued stock price.

This report, along with all of our research[1], utilizes our superior data[2] to get the truth about earnings, as shown in the Harvard Business School and MIT Sloan paper, “Core Earnings: New Data and Evidence.”

During the five-year holding period, KBH underperformed as a short position, rising 155% compared to an 80% gain for the S&P 500.

KB Home’s fundamentals have improved since our original report. Its return on invested capital (ROIC) increased from 1% at the time of our report to 6% TTM and its economic earnings were positive in both 2018 and the TTM period. Improved fundamentals mean KBH now earns an Attractive rating (from Very Unattractive) and no longer presents the same risk/reward, especially considering the tailwinds in the new home market. As a result, we are closing this short position.

Figure 1: KBH vs. S&P 500 – Price Return – Unsuccessful Short Call

Sources: New Constructs, LLC and company filings

Note: Gain/Decline performance analysis excludes transaction costs and dividends.

This article originally published on October 27, 2020.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

[2] Our core earnings are a superior measure of profits, as demonstrated in Core Earnings: New Data & Evidence a paper by professors at Harvard Business School (HBS) & MIT Sloan. The paper empirically shows that our data is superior to “Operating Income After Depreciation” and “Income Before Special Items” from Compustat, owned by S&P Global (SPGI).