This article details the uniquely rigorous diligence behind each of our ratings on 3000 stocks, 7000 mutual funds and 400 ETFs. It contains reports on all the adjustments we make to convert GAAP data to economic earnings and derive true shareholder value in a discounted cash flow model.

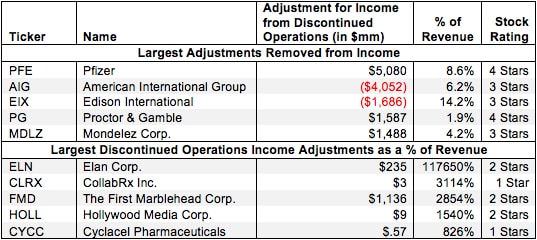

We remove all income and losses from discontinued operations in calculating operating profit because this income/loss will not recur in the future, and we are looking for the true profitability of the continuing and core operations of a company.

Reported earnings don’t tell the whole story of a company’s profits. They are based on accounting rules designed for debt investors, not equity investors, and are manipulated by companies to manage earnings. Only economic earnings provide a complete and unadulterated measure of profitability.

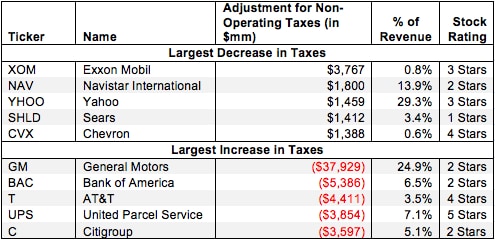

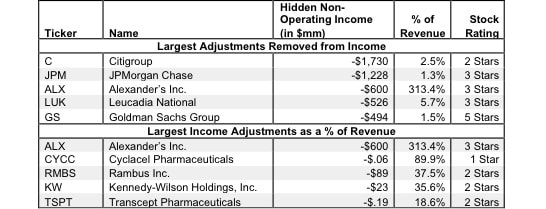

Non-operating items in operating income are unusual gains that don’t appear on the income statement because they are bundled in other line items. Without careful footnotes research, investors would never know that these non-recurring income items distort GAAP numbers by artificially raising operating earnings.

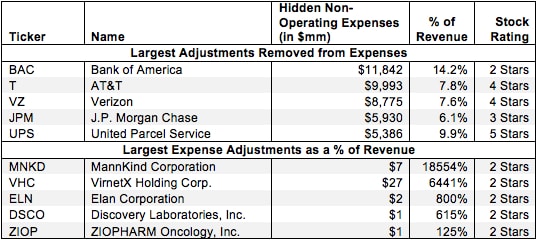

Non-operating expenses are unusual charges that don’t appear on the income statement because they are bundled in other line items. Without careful footnotes research, investors would never know that these non-recurring expenses distort GAAP numbers by lowering operating earnings.

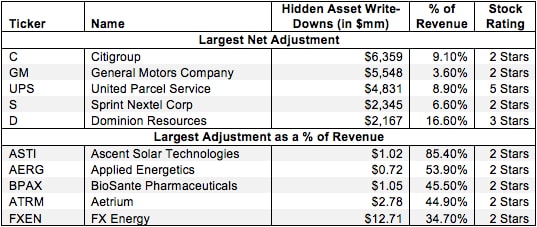

Asset write-downs are unusual charges that don’t appear on the income statement because they are bundled in other line items. Without careful footnotes research, investors would never know that these non-recurring items distort operating earnings by overstating core-operating costs.

This report summarizes our series of reports on how to convert GAAP data to economic earnings and derive true shareholder value in a discounted cash flow model as well as more accurate measures of economic

This article provides some empirical evidence behind my putting Apple (AAPL) in the Danger Zone last week because its return on invested capital (ROIC) is outrageously high. That fact underscores why valuing this company or any other with the expectation that such a high ROIC was sustainable would be a mistake.

If you bought Cisco Systems Inc (CSCO) last August when I recommended it to investors, or when I recommended it again in January, or any time between May 10, 2012 and now when the stock has had my Very Attractive rating, then today has been a good day for you.

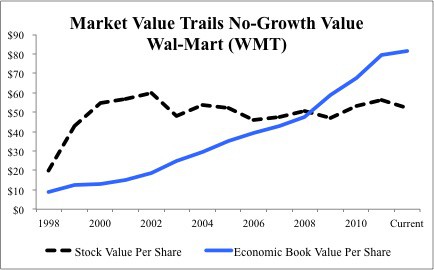

The difference between the stock price and Economic Book Value (EBV) of s stock measures the difference between the market's expectation for future profits and the no-growth value of the stock.

Our Company Valuation models are very sophisticated discounted cash flow and earnings quality models.

An enormous amount of works goes into every model. I wish I could offer a short-cut (beyond our ratings and reports) for understanding our models.

As discussed in “The Real Earnings Season Starts Now”, annual reports are the best source for developing investment ideas. I provided my clients with dozens of insights in 2011 that delivered impressive returns, and I continue that trend with my recommendation of MO.

Most of my research and publishing tends to focus on companies manipulating accounting rules to make their reported earnings look better than the real economic cash flows of their business.

It is unfortunately rare that I find a company whose economic earnings are outpacing the reported accounting results and whose stock is cheap.

One such company is Lam Research (LRCX – very attractive rating). One of September’s most attractive stocks, LRCX offers investors hidden value.

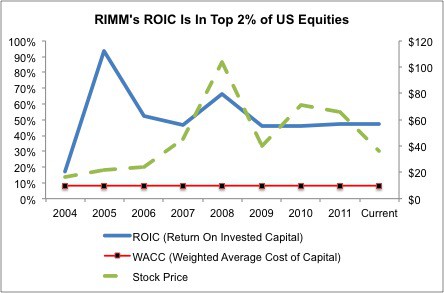

Here is a free copy of our report on RIMM for readers of Ask Matt.

The valuation of RIMM's stock implies the company's after-tax cash flow (NOPAT) will permanently decline by nearly 75%.

Yes, RIMM is losing market share and fast. Yes, RIMM’s Blackberry Playbook tablet is a dud. Yes, the stock has been a stinker recently. And yes, none of what I wrote at the beginning of this article would matter if the stock were not super cheap.