We joined Benzinga's PreMarket Prep on October 14, 2020 to discuss some of the stocks featured in our Earnings Distortion Scorecard and what to expect during the 3Q20 earnings season.

Investors deserve more diligence from fund managers, so we are putting those that don’t read SEC filings or lack the technology needed to thoroughly analyze those filings in the Danger Zone.

We found that Perrigo Company (PRGO), the firm Mr. Papa is leaving behind, exhibits many similarities to Valeant, including misleading non-GAAP measurements, aggressive, shareholder destructive acquisitions, and executive compensation misaligned with shareholders’ interests.

We calculate invested capital in two mathematically equivalent ways: financing and operating approach. Figure 1 shows the basic calculations. On page 2, we share the complete calculations for specific companies.

CEO David Trainer sat down with Chuck Jaffe of Money Life and MarketWatch.com to talk about our Danger Zone pick this past week: Danger Zone: Suspended Ratings.

We suspend our ratings on certain stocks when we feel the company's latest reported financials are no longer reliable or indicative of the risk/reward of the stock. For example, an announcement of an acquisition or spin-off means the current financial statements could change significantly.

Trading stocks sometimes feels like a very modern phenomenon, so it’s easy to forget that some of the companies we’re investing in go back a century or more.

JNJ is not a get rich quick stock that will double within a year, but it is a safe investment with limited downside risk and significant upside potential. A safe investment like JNJ could benefit a lot of investors in such a risky market.

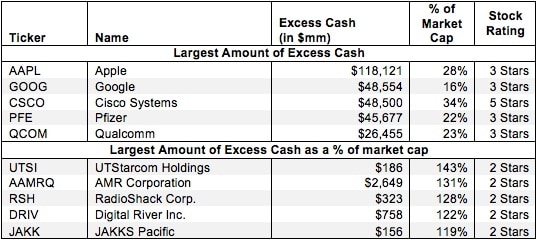

For most companies, we estimate the required amount of cash for normal business operations to be around 5% of sales. However, many companies hold cash or other liquid investments above and beyond this amount. We refer to this extra amount as excess cash. This surplus cash can be used for any number of purposes, including acquisitions, research and development, and cushioning the company against economic downturns. Excess cash is immediately available for distribution to shareholders, so we add a company’s excess cash to our calculation of shareholder value.

RAD is up against the ropes right now. The company has to contend with larger, more efficient competitors, significant debt, and declining sales. Don’t be fooled by the 150% growth in the share price this year. RAD is much worse off than its stock suggests.

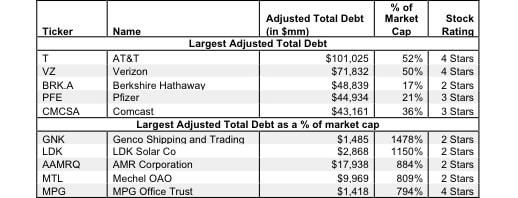

The fair value of a company’s total debt is the current amount the company would need to pay to retire the debt and settle the claims of the creditors. This fair value of debt is subtracted from shareholder value because the firm would need to settle these claims before it could return any cash to shareholders.