As discussed in “The Real Earnings Season Starts Now”, annual reports are the best source for developing investment ideas. I provided my clients with dozens of insights in 2011 that delivered impressive returns, and I am continuing that trend today with my recommendation to buy Altria Group [s: MO], which I recently upgraded from a Neutral to Very Attractive rating after reviewing the company’s 2011 10-K.

Focusing on the reported accounting earnings of MO leads investors down the wrong path. According to its 2011 10-K filed on February 16, 2012, MO’s GAAP earnings dropped by over $500 million or 13% compared to 2010.

The problem with relying on those results is that they are distorted by about $700 million in non-operating charges that inappropriately depress accounting earnings. Removing those items reveals that economic earnings that rose by 11% or $278 million in 2011.

These hidden charges are normally buried in “Cost of sales” or “Marketing and administration costs”. In our detailed report on the topic last year, we noted over 13,000 hidden items that distorted reported accounting results over the last decade plus.

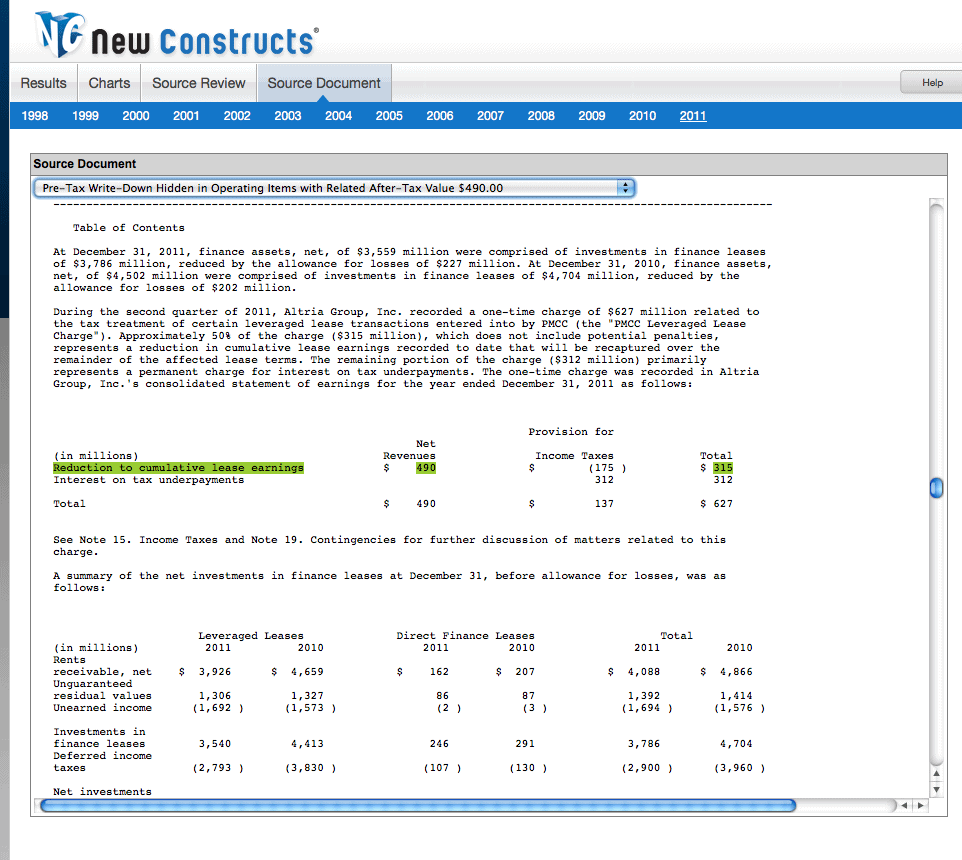

In Altria’s case, the largest one-time item is a $490 pre-tax charge related to the write-down of certain leveraged lease assets. Details are on page 23 of the 100-page 10-K filing. This charge is non-recurring in nature, and therefore, I exclude it (along with several other smaller charges) from the calculation of the company’s after-tax cash flow (NOPAT). These adjustments result in a higher NOPAT, which, in turn, drives an increase in the company’s ROIC from 13% in 2010 to 14% in 2011.

{kind=link}

Notably, we did not find any one-time income or revenue that inflated MO’s 2011 earnings.

The net impact of my detailed review of the footnotes in MO’s 2011 10-K is that the true, underlying profitability of the business is improving not declining. MO’s current 5.5% dividend is not only safe it could grow.

This performance underscores the strength of MO’s business and the ability of its management team to allocate capital intelligently.

My analysis underscores the potential futility in relying on accounting results, quarterly earnings and analysts’ estimates. Keep your eye on the cash flows not the “EPS”

Looking toward the future, one cannot deny the clouds on the growth horizon of tobacco companies. Cigarette smoking is on the decline in the United States, and may never grow again. MO’s smokeless tobacco business is growing, but slowly, and not fast enough to offset the entire decline in cigarettes.

I am not a smoker and never will be. However, I cannot deny the profit advantage that addictive products tend to have over products that are not addictive. And addictive products not only deliver higher profit margins, but they also maintain steadier revenues as large numbers of users are not likely to quit cold turkey even if they know the product is killing them. In other words, I doubt sales will fall off a cliff.

And yet, the stock market is pricing in a permanent 10% decline in the company’s after-tax cash flow (NOPAT) – at ~$29.65/share. The stock is worth over $32/share if the company’s NOPAT remains flat.

No matter the headwinds in the tobacco business, I trust Altria’s management team to grow profits. More of the growth may come from non-tobacco investments, such as wine and leasing. But management will continue its excellent track record for achieving high returns on the capital invested with it.

I expect management will continue to diversify into products, like wine and cigars, that will create value for shareholders just as they have in the past.

Do not fall asleep on this stock. A stock valuation that implies a permanent 10% contraction in NOPAT is too low. Though most investors may not have noticed, the company did grow profits last year. And I believe they will continue to do so in the future.

As my regular readers know, I also cover 7400+ ETFs and mutual funds. My predictive fund ratings leverage the deep research I do on all of the 3000+ stocks covered by my firm, New Constructs.

The funds that allocate the most (6.5%) to MO are DWS Value Series, Inc: DWS Strategic Value Fund (KDHIX) and Dreman Contrarian Funds: Dreman High Opportunity Fund (DRLLX). However, all classes of these funds get my Neutral rating or worse because, despite a rather large allocation to MO, they allocate too much of their capital to stocks that get my Neutral rating or worse.

The ETFs and funds that allocate 4% or more to MO and get an Attractive rating are:

- Consumer Staples Select Sector SPDR [s: XLP]

- Vanguard World Funds: Vanguard Consumer Staples Index Fund [s: VCSAX]

- Vanguard Consumer Staples ETF [s: VDC]

- Focus Morningstar Consumer Defensive Index ETF [s: FCD]

- ICON Funds: ICON Consumer Staples Fund [s: ICLEX] – note only the “E” shares get my Attractive rating.

New Constructs’ free fund screener provides free reports on 7400+ mutual funds and ETFs, including all of the funds mentioned in this article.

Disclosure: I receive no compensation to write about any specific stock, sector or theme.