Most investors know us for our Core Earnings research, a proprietary measure of earnings that adjusts for accounting tricks that mislead investors about corporate profits. The Core Earnings Leaders Index (ticker: BCORET:IND) beat (up 27% vs 18%) the S&P 500 by 9% in 2025 and provides solid evidence that there’s alpha in our Core Earnings research.

Today, we’re sharing our proprietary measure of Free Cash Flow (FCF) and delivering unrivalled insights into the winners and losers of the AI race. Our FCF, like Core Earnings, is proprietary and incorporates critical data from footnotes. Unlike Core Earnings, FCF accounts for capex and balance sheet changes and, therefore, provides a comprehensive assessment of cash flow available to all stakeholders.

Our FCF research shows that some companies are using accounting tricks to hide how much capital they are risking to stay in the AI race. We think certain companies do not want investors to know just how much money they’re spending on AI because the numbers are huge, and at least two companies cannot keep up the pace for much longer.

In other words, they will have to drop out of the race in as little as a few months, unless they plan to seriously dilute current investors, a message that would likely knock a few percentage points off their stock price. So, we can see why they want to keep the numbers hidden. And, we’re here to give them to you anyway.

Don’t Trust the Media’s Version of Free Cash Flow

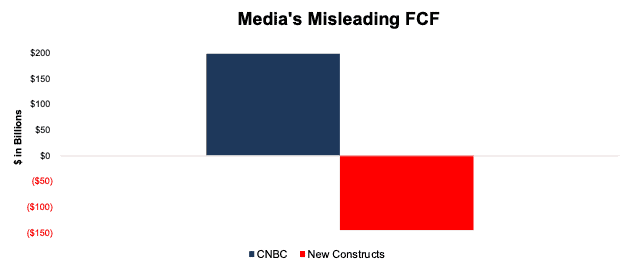

Before we get into our numbers, let’s take a look at what the media says about FCF. Those investors that trust the media are probably not aware of the tech giants’ heavy cash burn in 2025. For example, CNBC reported that Alphabet (GOOGL), Microsoft (MSFT), Meta (META), and Amazon (AMZN) “generated a combined $200 billion in free cash flow” in 2025.

Meanwhile, our more comprehensive calculation of FCF reveals these four companies burned a combined $146 billion in FCF in 2025. See Figure 1. We’re able to get the true FCF results because of our careful footnotes research. The results are not as positive as what you see from other sources.

Figure 1: Media’s 2025 FCF For Alphabet, Microsoft, Meta, & Amazon Is Off by $346 Billion

Sources: New Constructs, LLC and company filings

What’s the Problem?

Last November, our AI Winners & Losers report posited that the early winners of the AI arms race were the companies that generate the most cash to fuel continued AI spending. Since then, AI competition has heated up considerably and spending plans have ramped up, to say the least!

Big tech companies Alphabet, Microsoft, Meta, and Amazon recently guided for $650 billion (at midpoint of estimates) in capital expenditures on AI in 2026.

These companies can’t keep up this massive spending forever, and this report will show you exactly which of these tech emperors lack the cash to stay in the race.

Exposing The Devil in the Footnotes

We’ll reveal the big losers in the AI race below, but first let us explain how we reversed a new accounting trick to uncover the truth. We had to go beyond reported earnings, income statements, balance sheets, and cash flow statements to find monstrously high hidden costs.

You won’t find research like this from other firms. Most of them do not want you to know or even think about balance sheets and FCF. They want you to just keep buying; so they keep dancing to the same bullish beat that’s dominated headlines for years. Investors only looking at reported earnings are victim of the accounting tricks that Wall Street uses to support the bullish narratives.

But, a look under the hood reveals the devil is in the balance sheet details.

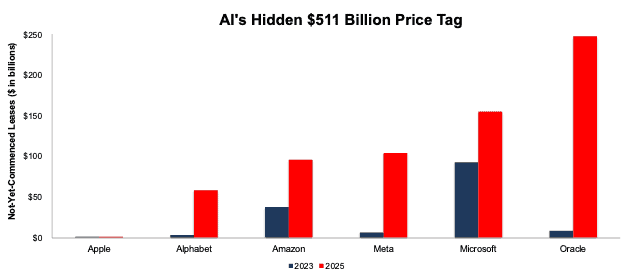

Each of the companies mentioned above reported billions in earnings in 2025. Their debt levels look normal, under control. So, what’s the big deal? Reported earnings and balance sheets overlook a new accounting trick that adds ~$427 billion in capex hidden in off-balance sheet debt in 2025 alone.

Off-Balance Sheet Debt Is Exploding

From 2023-2025, the total debt for each of the companies in Figure 2 jumped by $561 billion. Given that most, $511 billion, of the increase in total debt comes from off-balance sheet debt, we think most investors are unaware of the huge increase in liabilities for these companies. They also likely not aware of the huge drain these liabilities are on cash flow and profitability. In other words, this hidden debt changes the game.

Figure 2: Not-Yet-Commenced Leases: AI Spenders: 2023-2025

Sources: New Constructs, LLC and company filings

Due to Oracle’s fiscal year, data is from November 2023 through November 2025. All other data is from December 2023 through December 2025

Take Oracle, for example. In its fiscal 2Q26 10-Q, the company disclosed $248 billion in not-yet-commenced leases, up from $26 billion in fiscal 2Q25. These leases, “substantially all related to data centers and cloud capacity arrangements” are not included on Oracle’s balance sheet…yet. But, they do represent real capital allocated.

Oracle isn’t alone. All of the companies in Figure 2 (except for Apple) reported significant increases in not-yet-commenced leases:

- Amazon: $96 billion in 2025, up from $38 billion in 2023.

- Alphabet: $59 billion in 2025, up from $4 billion in 2023.

- Meta: $104 billion in 2025, up from $7 billion in 2023.

- Microsoft: $155 billion in 2025, up from $93 billion in 2023.

Not-yet-commenced leases are a new way to hide debt off the balance sheet post recent accounting rule changes (ASC 842 and IFRS 16). We find and include these lease obligations in our total debt and invested capital calculations to ensure we capture all the capital companies employ to generate revenue.

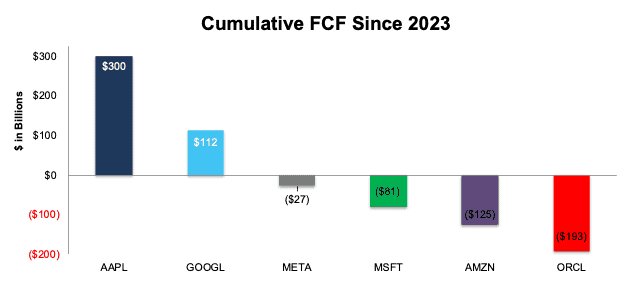

Free Cash Flows Are Cratering

For the same reasons most investors are not aware of the massive increases in debt, they are likely not aware of the massive declines in FCF. Figure 3 updates our analysis from last November and reveals that the companies struggling to stay in the AI race back then are struggling even more to maintain AI spending now.

Apple and Alphabet are the only two companies in the group to generate positive FCF in 2025.

In contrast, Microsoft, Amazon, Meta, and Oracle burned $350 billion in FCF in 2025.

Looking at FCF from calendar 2023 through 2025, we see the divergence between the FCF winners and losers is growing.

See Figure 3. Apple and Alphabet generate strong cash flows consistently and have a clear advantage in funding long-term AI goals. Meanwhile, businesses like Amazon and Oracle, with billions in negative FCF, face substantial challenges.

Figure 3: AI Spenders’ Cumulative FCF: 2023 – 2025

Sources: New Constructs, LLC and company filings

Due to Oracle’s fiscal year, data is from November 2023 through November 2025. All other data is from December 2023 through December 2025

Who Will Be AI Winner(s) and Loser(s)?

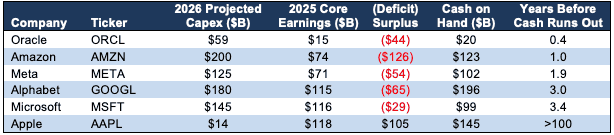

Per Figure 4, Amazon and Oracle look to be the early AI losers. Oracle can’t maintain its projected AI spend for even one year, while Amazon can only maintain its spend for one year, without substantially diluting investors.

Our take is that the AI winner(s) will be the company(ies) that can sustain massive AI expenditures the longest and outlast the competition. Though we are in the early stages of the AI race, we are already seeing losers emerge.

To identify the losers and winners, we subtract projected AI spend from the companies’ Core Earnings and cash on hand. This approach allows us to get a good measure of how long each company can sustain its current AI spend levels without the need for additional capital.

For this analysis, we make the following assumptions:

- Future years’ AI spend equals projected 2026 levels.

- All capex is for AI.

- Core Earnings equal 2025 levels each year in the future.

- Any deficit after subtracting AI spend from Core Earnings is met with cash on hand (when available).

You might not agree with these assumptions, and we’re not sure they’re right, either. But, we think they are close enough to give us a vaguely right perspective for measuring how long these companies can sustain their current AI spending.

Figure 4: How Long to Sustain 2026 Capex Without Diluting Investors

Sources: New Constructs, LLC and company filings

Due to Oracle’s fiscal year, cash on hand and Core Earnings data is for the 12 months ended November 30, 2025. Apple’s data is for the 12 months ended December 27, 2025. All other data is for the 12 months ended December 31, 2025.

Over the next 12 months, Oracle is projected to spend $59 billion on AI (annualized estimate based on expected spending in the second half of fiscal 2026). Meanwhile, the company generated just $15 billion in Core Earnings in 2025. So, it needs $44 billion to fund its projected capex. With just $20 billion in cash on hand, Oracle lacks the funds to support its projected spend. Either it cuts spending and drops out of the AI race, or it raises additional debt or equity capital. Not surprisingly, on February 1, 2026, Oracle announced plans to raise $45-$50 billion in cash during 2026.

Amazon has a similar story. Management guided for $200 billion in capex in 2026, and the company generated $74 billion in Core Earnings in 2025. The gap, $126 billion, can be filled by Amazon’s $123 billion in cash on hand, but then Amazon would have no more cash on hand. Not surprisingly, Amazon filed a mixed shelf registration with the SEC on February 6, 2026, which lets investors know the company plans to raise additional capital.

Alphabet and Microsoft are in much stronger positions, as each company can sustain their projected 2026 capex spend for three more years before needing additional capital.

Apple, with its more modest approach to AI spending, is the clear outlier in Figure 5. Analyst’s project the company’s capital expenditures will grow to $14 billion in 2026. However, with $118 billion in Core Earnings, Apple’s free cash flow remains strongly positive. The company can maintain that low capex forever, if needed. More likely, Apple will use its cash hoard to license technology from or buy one of the other winners.

Wait…We Still Have to Account for Spending on Data, Which Will Be Huge, Too

If you think Oracle and Amazon are hurting now, we think their ability to stay in the AI race only weakens because we are in the early stages of big AI spending.

Until recently, the AI race focused on hardware infrastructure to run the AI with little attention paid to the data we give the AI.

Every day, more and more people are realizing that the most essential ingredient in building reliable AI systems is high-quality data. The saying “garbage in, garbage out” applies to AI models as much or more than any other model. No matter how much infrastructure or large the language model, an AI system trained on unreliable data will be unreliable.

We’ve written extensively on why high quality training data is an essential input for building truly reliable AI. And, now, we’re seeing more people make the same points every day, especially on social media.

I would bet that anyone who’s used AI a decent amount has experienced an alarmingly incorrect hallucination. The time lost on dealing with hallucinations drives experts to ignore AI for truly expert-level tasks until they know they can trust it to be truly accretive to their work. As a result, users limit how much they trust and rely on the AI and remain focused on developing their own insights. Those work habits will not change until AI gets a lot better at delivering expert-level insights.

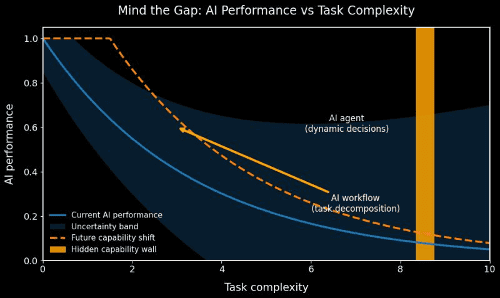

The fact is, at this point in time, AI systems get more unhelpful, as they hallucinate more as task complexity rises.

Figure 5: AI Performance as Task Complexity Rises

Sources: Arman Khaledian, Zanista AI

How Will AI Generate the ROI Needed to Justify the Huge Capex? Better data.

Until users can trust AI to reliably perform complex tasks, we do not see them paying much for access to AI. If users are not willing to pay substantially more for access to AI, the gigantic AI capex detailed above will not earn its spenders an adequate return on investment. In which case, those stocks might not just plummet, they could go to zero.

Consequently, we expect an entirely new AI spending spree to acquire high-quality datasets that truly endow machines with deep subject matter expertise. When AI can deliver correct, truthful answers to questions that experts would ask or that require deep subject matter expertise, then we can expect an explosion in AI-driven revenue and profits. Until then, we see AI’s utility as far below what’s needed to generate an adequate return on the gigantic AI spend.

I do not think it’s controversial to assert that the companies that can add the highest quality training datasets to their AI infrastructure will be the best positioned to win the AI race.

This kind of marriage is not some distant “dream” scenario. We’ve demonstrated the unrivaled power of AI when high quality datasets are married with cutting-edge technology. See what Google Cloud created in FinSights.

Unfortunately, there are not many other examples of AI Agents like FinSights, and we believe AI companies will have to spend comparable amounts of money to develop or acquire good AI-worthy datasets as they are spending on infrastructure already.

Today’s Winners Could be Tomorrow Losers

We’re still early in the AI race, and we are already seeing firms look like they will run out of cash and fall out of the race. Apple and Alphabet look like the early winners.

One could hypothesize that, once certain competitors run out of cash and fall out of the race, Alphabet can cut back on spending, too. It could use some leftover cash to buy capabilities from fallen competitors. Or, the company could keep spending at today’s rates. As the number of firms in the race declines, the stronger the competitive position and the ability to raise capital for the remaining firms.

Given the limited success Apple has seen from its internal AI initiative, it appears that its strategy is to buy versus build. With its huge cash hoard and strong cash flows, Apple is in position to pay handsomely for AI capabilities.

One thing is for sure, the AI race will remain a very interesting one to watch.

Our next report will focus on the impact of the AI race on return on invested capital (ROIC) and FCF Margins, as well as our assessment of the valuation of AI stocks and the Mag 7. Preview…our initial work shows major changes are happening and that the tech sector’s long leadership reign might be coming to an end soon.

This article was originally published on February 18, 2026.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.