Passive vehicle safety systems sit at the center of vehicle design, regulatory compliance, and occupant protection. They are not discretionary features. They are increasingly important, and safety standards tend only to rise over time, not decline.

This week’s Long Idea features a market leader in safety systems that operates from a position of real scale in a part of the vehicle that remains essential regardless of brand, drivetrain, or consumer trends. As a result, the company offers Very Attractive risk/reward in a steadily growing industry.

Below, we provide an excerpt from our latest Long Idea report. You can buy the full report a la carte here.

We’re not giving you the ticker for this pick, but this excerpt shows how thorough we are.

This stock presents quality Risk/Reward based on the company’s:

- global footprint as a leading auto safety product manufacturer,

- long-term contracts with leading automakers,

- high profitability, including an ROIC that leads peers,

- attractive capital return and shareholder yield, and

- cheap valuation that implies profits will permanently decline 10% despite long-term growth tailwinds.

A Business Built to Profit from Safety Across the Globe

This company’s performance over the past decade reflects a business that has held up well through a wide range of industry cycles. As a global automotive supplier, it is inevitably exposed to fluctuations in light vehicle production, supply-chain friction, and changes in regional demand. Even so, the company has remained on solid footing and grown revenue and profits across decades.

The company’s success is driven in part by its geographic diversification. The company is not overly dependent on any single auto market, which helps smooth out the volatility that comes with a cyclical industry.

In 4Q25, the company’s sales break down as follows:

- 30% from the Americas,

- 27% from Europe,

- 23% from China

- 12% from “Rest of Asia”, and

- 8% from Japan.

This global footprint gives the company exposure to major global auto markets while also positioning the company to profit from growth pockets outside the more mature Western markets.

FCF Supports Capital Return

The company’s cash reinforces a broader story of a business that not only generates consistent profits but also meaningful free cash flow (FCF).

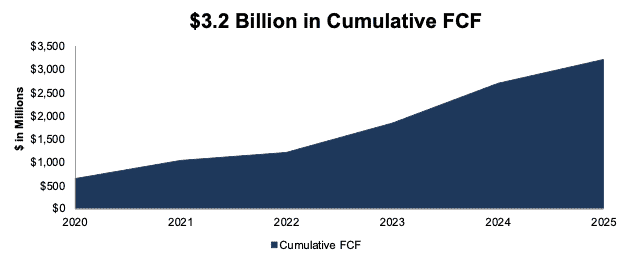

Since 2020, the company generated $3.2 billion (31% of enterprise value) in cumulative free cash flow. Over that same period, the company paid $1.1 billion in dividends and $1.4 billion in share repurchases, for a total shareholder return of $2.5 billion. In other words, the company generated significantly more FCF than it distributed to shareholders. See Figure 8 from the full report.

That balance is important in the context of a cyclical industry. It suggests that the company’s dividend and buyback programs have been supported by underlying cash generation rather than stretched financial resources. Consistent FCF generation also provides a cushion during weaker periods while still preserving the company’s ability to invest in operations, support new program launches, and maintain its position with global OEMs.

Figure 8: Cumulative FCF: 2020 – 2025

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.