Sometimes, beating both top and bottom-line expectations is a good thing. Sometimes, it’s a head fake.

“Good” earnings results aren’t nearly enough to justify the expectations for future profit growth baked into the stock price of this week’s Danger Zone.

Expectations for future revenue and margins are so high for this stock that no serious analyst could make a straight-faced argument for the stock remaining at current levels.

Below, we provide an excerpt from our latest Danger Zone report to show how our research helps you see danger before it crushes your portfolio. Get the full report a la carte here.

This stock could fall further based on:

- slowing growth rates,

- misleading adjusted metrics,

- persistently high operating expenses,

- lagging profitability in an extremely competitive industry,

- consistent cash burn, and

- stock price that implies the company will grow profits nearly 36x TTM levels.

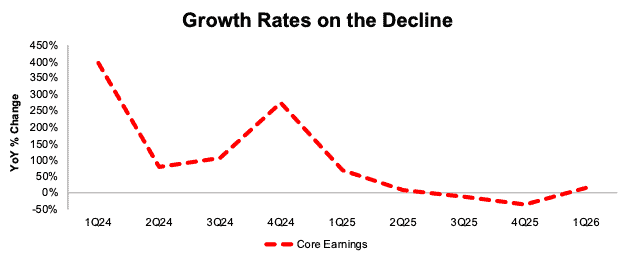

Growth Rates Slowing

The company’s once high-flying growth rates have fallen significantly. The YoY change in quarterly Core Earnings fell from 390% in 1Q24 to 14% in 1Q26. The YoY change in quarterly Core Earnings was -13% in 3Q25 and -37% in 4Q25.

Even the best businesses slow eventually, but this company’s valuation implies the exact opposite, as we show in the full report.

Figure 1: Quarterly Core Earnings: YoY Change 1Q24 – 1Q26

Sources: New Constructs, LLC and company filings

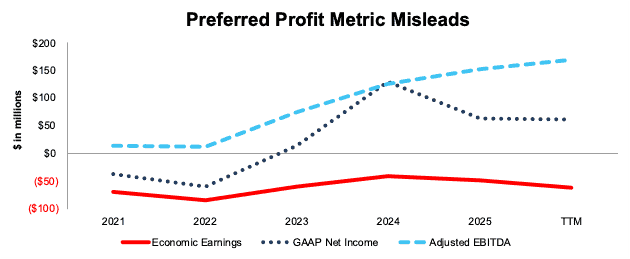

Misleading “Adjusted” Metrics

This company, like many growth businesses, presents multiple versions of profitability, all of which mask true earnings.

Investors can’t see that if they only follow the company’s non-GAAP metric, Adjusted EBITDA. The company’s Adjusted EBITDA increased from $126 million in 2024 to $170 million over the TTM. Over the same time, GAAP net income fell from $130 million to $62 million, while economic earnings declined from -$41 million to -$62 million over the same time.

It’s a big red flag when a company’s preferred profitability metric is positive and rising while economic earnings are negative and declining.

Figure 2: GAAP Net Income vs. Economic Earnings vs. Adjusted EBITDA

Sources: New Constructs, LLC and company filings

Burning Cash Since IPO

In our pre-IPO report on this company, we noted that the company was burning millions in free cash flow (FCF).

Little has changed. We realize a high growth business should burn cash, but there needs to be an end in sight.

The company burned a cumulative $461 million (5% of enterprise value) in FCF from 2021 through 1Q26. See Figure 4 in the full report for details.

Despite the large cash burn, the company does not qualify as a Zombie Stock because it has enough cash on hand to sustain its cash burn for more than 24 months.

However, avoiding the Zombie Stock list doesn’t mean all is well. The company burned -$122 million in FCF in 2025.

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Danger Zone reports.

Interested in starting your membership to get access to more of our research? Get more details here.