This week’s Long Idea report features an industry leader with diversified assets, a robust shareholder return program, and a strong balance sheet.

With demand for oil and gas expected to persist for the next two decades and a strong development pipeline through 2030, this business has room to grow and return cash to shareholders. Yet, the stock remains undervalued.

Below, we provide an excerpt from our latest Long Idea report. You can buy the full report a la carte here.

We’re not giving you the ticker for this pick, but we are happy to share this preview so you can see how we operate.

This stock presents quality Risk/Reward based on the company’s:

- position to profit from growing oil and gas demand,

- diversified energy assets,

- robust shareholder returns,

- strong balance sheet, and

- cheap valuation.

Higher Demand for Longer

It’s no secret that oil production is on the rise. Despite best efforts around the world to minimize fossil fuel use, the latest projections show oil and liquid fuel demand persisting for years into the future.

In the short-term, the EIA projects global oil and liquid fuel consumption will grow 1% YoY in both 2026 and 2027.

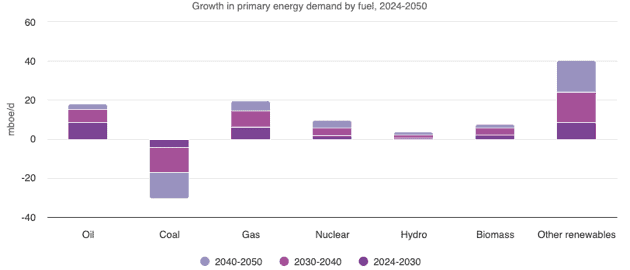

Longer-term, OPEC’s World Oil Outlook projects global primary energy demand will rise from 308 million barrels of oil equivalent per day (mboe/d) in 2024 to 378 mboe/d by 2050, or an increase of 23%.

This growth is spread across all fuel types, except coal, the only fuel type projected to see a drop in demand through 2050. Oil demand is expected to rise by 18 mboe/d, and natural gas demand is expected to grow by 20 mboe/d through 2050. See Figure 2 from the report.

Figure 2: Growth in Global Energy Demand by Fuel Type: 2024 – 2050

Sources: OPEC

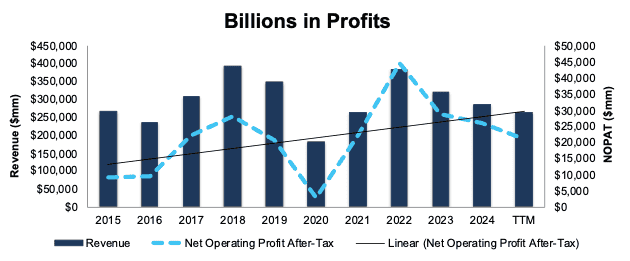

Billions in Profits Across Cycles

This company’s profits fluctuate with oil prices. But even in “down” years, the company still generates billions in profit.

The company has grown net operating profit after-tax (NOPAT) by 9% compounded annually since 2015. The company’s NOPAT margin improved from 3% in 2015 to 8% in the TTM, while invested capital turns were flat at 0.8. Rising NOPAT margins and steady invested capital turns drive the company’s return on invested capital (ROIC) from 3% in 2015 to 6% in the TTM.

Figure 4: Revenue and NOPAT: 2015 – TTM ended 3Q25

Sources: New Constructs, LLC and company filings

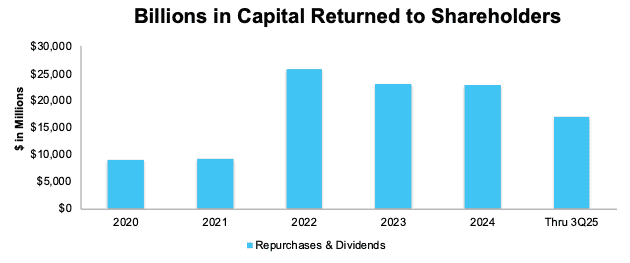

Taking Care of Shareholders with ~10%+ Yield

We like companies that choose to return capital to shareholders instead of spending it on costly acquisitions or executive bonuses that rarely drive shareholder value creation.

The company consistently returns billions in profits to shareholders through dividends and share repurchases. In fact, on the company’s earnings call, the CEO noted that returning 40-50% of cash flow from operations is “sacrosanct.”

The company has increased its dividend from $0.33/share in 1Q21 to $0.74/share in 1Q26. When annualized, the current dividend gives investors a 3.7% yield. From 2020 through 3Q25, the company paid out nearly $45 billion in dividends.

The company also returns additional capital to shareholders via share repurchases. The company repurchased $14.6 billion and $13.9 billion of shares in 2023 and 2024, respectively. In the first nine months of 2025, the company repurchased $10.5 billion of shares. In its 4Q25 earnings release, the company announced a $3.5 billion repurchase program, which it expects to complete by Q1 results in May 2026. This announcement marks the 17th consecutive quarter in which the company announced $3 billion or more in buybacks.

If the company repurchases shares at the TTM pace ($14 billion), it would repurchase 6.0% of the current market cap over the next 12 months. The combined dividend and repurchase yield would be an impressive 9.7%.

Figure 5: Repurchases & Dividends: 2020 – 3Q25

Sources: New Constructs, LLC and company filings

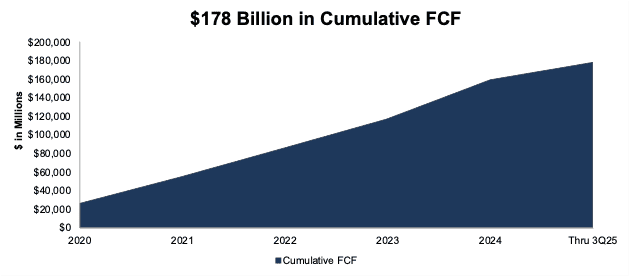

Strong Cash Flows Support Capital Return

The company generated a cumulative $178 billion (63% of enterprise value) in free cash flow (FCF) from 2020 through 3Q25. See Figure 6. Over the same time, the company returned $107 billion to shareholders through dividends and repurchases.

Figure 6: Cumulative Free Cash Flow Since 2020

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

I’ll keep sending information on quality sectors, industries, or specific companies until you’re ready to start your membership.

Interested in starting your membership to get access to all our Long Ideas? Get more details here.