This week’s Long Idea features a company that steadily maintains leading market share, generates best-in-class profitability, returns capital to shareholders, and operates in the best markets. Despite some near-term uncertainty, long-term tailwinds should support years of profit growth.

Below, we provide an excerpt from our latest Long Idea report. You can buy the full report a la carte here.

We’re not giving you the ticker for this pick, but we are happy to share this preview so you can see how we operate.

This stock presents quality Risk/Reward based on the company’s:

- asset-light, lot-option business model,

- exposure to structurally undersupplied housing markets,

- focus on entry-level through first move-up buyers,

- best-in-class profitability and ROIC, and

- relatively cheap stock valuation.

Housing Shortage Persists

Despite years of modest homebuilding growth, the U.S. housing market has never fully recovered its pre-crisis supply dynamics from before the 2007–2009 Global Financial Crisis. The lack of supply creates a chronic shortage that continues to pressure affordability.

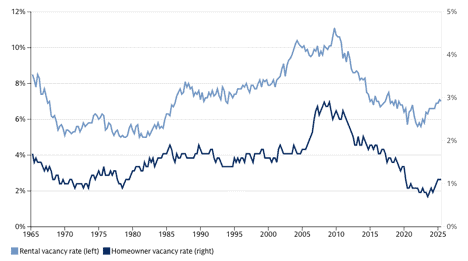

Goldman Sachs research shows that vacancy rates for both rental and homeowner listings are below levels seen in the two decades before the crisis, which reflect a long-term under-supply relative to demand. See Figure 1. This dynamic is great for landlords but hurts affordability for buyers and renters.

Goldman Sachs further estimates the U.S. needs roughly 3–4 million additional housing units, or ~2-3% of the current housing stock, just to alleviate the shortage and restore affordability.

Figure 1: Rental and Homeowner Vacancy (1965-2025)

Sources: Goldman Sachs

Strong Profit and Revenue Growth

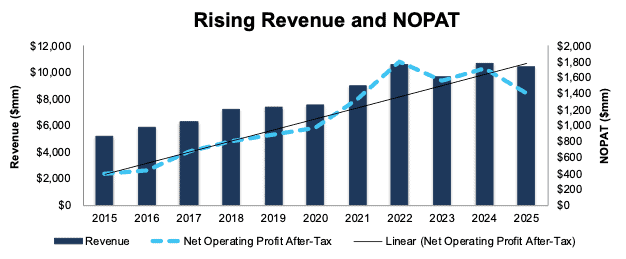

This company has grown revenue and net operating profit after-tax (NOPAT) by 7% and 13% compounded annually, respectively, from 2015 through 2025. The company’s NOPAT margin improved from 7.7% in 2015 to 13.5% in 2025, while invested capital turns improved from 3.9 to 4.1 over the same time. Rising NOPAT margins and invested capital turns drives the company’s ROIC from 30% in 2015 to 55% in 2025.

Figure 5: Revenue and NOPAT: 2015 – 2025

Sources: New Constructs, LLC and company filings

Consistent Cash Flow Generation

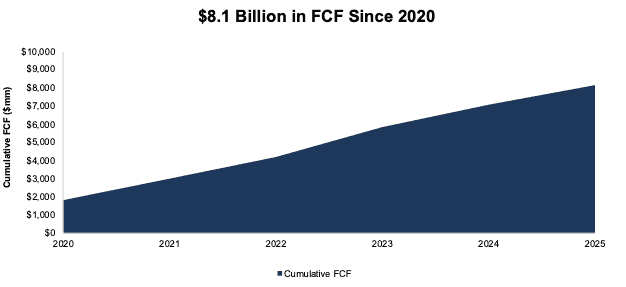

The company generates strong free cash flow (FCF) throughout its history. In fact, the company has only generated negative FCF in two years of our model, 2010 and 2011. Since 2020, the company generated $8.1 billion in FCF, which equals 36% of its enterprise value. See Figure 8.

The company generated $1 billion in FCF in 2025.

Figure 8: Cumulative Free Cash Flow Since 2020

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

I’ll keep sending information on quality sectors, industries, or specific companies until you’re ready to start your membership.

Interested in starting your membership to get access to all our Long Ideas? Get more details here.