This week’s Long Idea features a leading energy company that is expanding its asset base, improving efficiencies, and driving down costs across its operations. As a result, it is the most profitable company amongst its peers.

The current geopolitical environment and resulting upheaval in global energy markets looks likely to drive higher oil prices and restrict supply for the foreseeable future, which further boosts this company’s profit growth potential.

However, the stock price implies the company’s profits will never grow again. We believe the market has failed to recognize the strength of this business, which creates opportunity for our clients.

Below, we provide an excerpt from our latest Long Idea report. You can buy the full report a la carte here.

We’re not giving you the ticker for this pick, but we are happy to share this preview so you can see how we operate.

This stock presents quality Risk/Reward based on the company’s:

- position to profit from persistent demand and higher prices,

- plant and well investments to lower costs, expand margins, and increase capacity,

- industry-leading profitability,

- quality yield supported by strong cash flows, and

- cheap valuation.

Oil & Gas Pumped Up by Geopolitical Risk

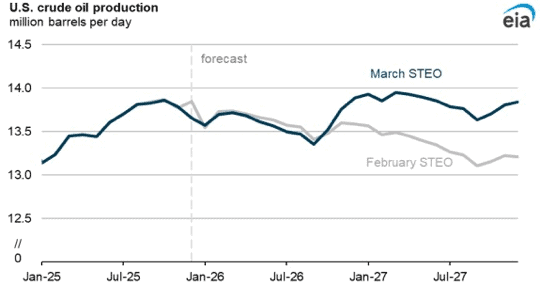

It’s no secret that countries across the globe are producing more oil and gas – a point we’ve highlighted in recent reports such as Energy Demand Isn’t Going Away, But This Opportunity Might. The U.S. Energy Information Administration (EIA), in its March 2026 Short-Term Energy Outlook, projects U.S. crude oil production to continue expanding to an average of 13.6 million barrels per day (b/d) in 2026 and 13.8 million b/d in 2027. See Figure 1.

In the most notable departure from past projections, the outlook now projects higher crude prices moving forward due to the U.S. – Iran war. In the latest update, the EIA projects Brent Crude oil will remain above $95/barrel over the next two months before falling below $80/barrel in third quarter and ~$70/barrel by the end of the year. The EIA projects prices will average $64/barrel in 2027.

Figure 1: U.S Crude Oil Production Estimate: 2025-2027

Sources: U.S. Energy Information Administration

Industry Leading Efficiency

This company continues to demonstrate that operational excellence can drive increased efficiency, materially lower costs, and sustain strong profitability.

The company reduced average well costs and operating costs by 7% and 4%, respectively, in 2025.

More specifically, in the Delaware Basin, the company reduced well costs 20% from 2023 to 2025 and increased average lateral length 30%, which provides increased efficiency and productivity.

The company notes in its 4Q25 earnings presentation that, in the Delaware Basin, it operates with the lowest per-well capex, operating costs, days to drill, days to complete, and breakeven price amongst its peers.

In the Eagle Ford region, the company cut well costs by 15% from 2023-2025 and increased completed lateral feet per day by 30% over the same time. The company notes it has the second lowest breakeven price amongst peers operating in the region.

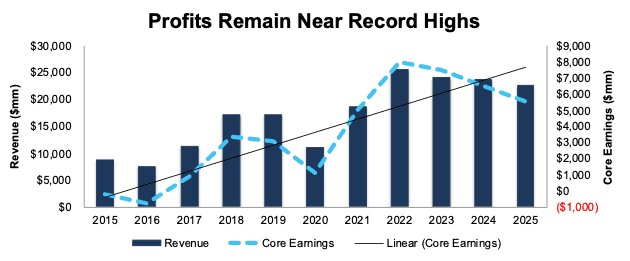

Profits Still Near Records

While profits are down from record 2022 levels, the company continues to generate strong Core Earnings. In 2025, the company’s Core Earnings were $5.5 billion, down from 2022 levels, but still nearly five times higher than 2020.

The company has grown revenue and Core Earnings by 15% and 37% compounded annually, respectively, over the past five years. Longer-term, the company has grown revenue by 10% compounded annually since 2015 and Core Earnings from -$180 million to $5.5 billion over the same time. See Figure 3 from the full report.

Figure 3: Revenue and Core Earnings: 2015 – 2025

Sources: New Constructs, LLC and company filings

High Efficiency and ROIC Are Part of the Culture

The company didn’t just luck into a highly efficient and productive operation. Instead, industry leading ROIC is a result of quality corporate governance and, in particular, the company’s focus on improving its return on capital employed (ROCE), a variant of ROIC.

Quality corporate governance holds executives accountable to shareholders by incentivizing prudent capital allocation. There is also a strong correlation between improving ROIC and increasing shareholder value. By evaluating executive compensation plans, investors can find the few companies that align executives’ interests with shareholders’ interests.

The company’s performance compensation includes a return on capital employed modifier. The modifier can adjust the performance unit payouts by anywhere from -70% to +70% based on the company’s three-year average ROCE. ROCE is similar to our measure of ROIC, in that the company adjusts for items such as impairments, gains on asset sales, short and long-term debt, and cash on hand, to derive a return metric more reliable than a traditional return on capital employed.

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.