As incomes rise and tourism expands, air travel demand in Latin America is growing faster than airline seat supply due to aircraft delivery constraints and broader aerospace supply-chain bottlenecks. This imbalance supports improving passenger load factors (PLF), pricing power, and profit growth for this week’s Long Idea: Copa Holdings (CPA: $153/share).

The Panama-based airline’s hub-and-spoke network, single-plane fleet strategy, and industry-leading operational reliability position it to profitably meet growing regional demand. Despite these factors and the firm’s history of profitability, the stock price implies a permanent decline in profits. The best opportunities arise when strong profits and growth prospects collide with low expectations.

CPA presents quality Risk/Reward based on the company’s:

- strategically located international hub,

- ultra‑low‑cost operating structure with full‑service economics,

- industry‑leading on‑time performance and profitability,

- consistent profit growth,

- attractive capital return potential, and

- cheap stock valuation that implies a permanent profit decline.

Latin America’s Growing Appetite for Air Travel

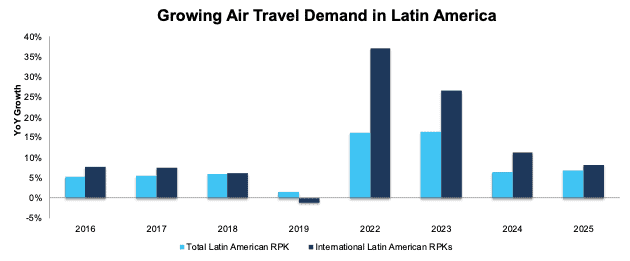

According to the International Air Transport Association (IATA), Latin American international revenue passenger kilometers (RPKs), a measure of passenger demand, grew by an average of 5.1% per year between 2016 and 2019, while total Latin American RPKs grew by an average of 4.5% per year over the same time.

From 2022-2025, after the global COVID-19 shut downs, Latin American international RPKs and total Latin American RPKs have grown by an average of 20.8% and 11.4%, respectively. See Figure 1.

Figure 1: Year-Over-Year Latin American RPK Growth: 2016-2025 – Excluding COVID (2020-2021)

Sources: IATA

*We exclude COVID’s impact in 2020 and 2021 on air travel for visualization purposes. For reference, total Latin American RPK fell 57% and 23% YoY in 2020 and 2021, respectively while Latin American International RPK fell 76% and 40% YoY over the same time.

Going forward, Airbus projects growth will continue in large part due to Latin America’s growing middle class, continued GDP growth, and ongoing urbanization.

They’re not alone.

- Boeing projects international tourist arrivals to grow by 40% in Latin America over the next decade and annual traffic growth (measured in RPK) of 4.3% through 2044.

- The International Air Transport Association projects annual growth of 3.2% through 2044 in Latin America, which would translate into an additional 218 million passengers over the next two decades.

One thing is clear: Latin American air travel has ample room to grow, especially considering Latin Americans make 0.5 air trips per capita compared to 2.2 for North Americans and 1.9 for Europeans.

A Supportive Geopolitical Setting Could Push Growth Even Higher

Latin America’s geopolitical outlook could provide additional upside to the region as well. The deepening involvement of the United States, the European Union, and China for a variety of reasons (nearshoring, energy investment, and trade diversification) can drive increased standards of living, business travel and intra-regional connectivity.

Panama is a main beneficiary of this attention, given its combination of dollarization and geographic centrality, which reinforces its role as a key transit hub for North-South and intra-Latin American traffic.

Supply Shocks Limit Capacity

While demand has recovered since 2022 (after the Boeing MAX issues and COVID-induced drop), global aircraft supply chain problems persist. In November 2025, IATA highlighted “capacity constraints stemming from challenges in the aerospace supply chain” and stated “manufacturers need to address production shortfalls” with a backlog of over 17,000 aircraft orders.

As a result of these constraints, available seat kilometers (ASK) have trailed demand. The good news for Copa is that Latin American PLF, which measures how efficiently an airline fills its available seats with paying passengers, increased from 80.8% in 2016 to 83.4% in 2025.

Even though both Airbus and Boeing plan to ramp up production, higher PLFs are likely to persist. Boeing projects Latin American airline traffic will grow >4% a year through 2044, but that the overall airline fleet will grow by just 3% a year over the same time.

Demand outstripping capacity provides support for higher PLF, pricing, and airline profitability for years to come.

Operating in The Hub of the Americas

In a region where seat demand is rising while supply is constrained, Copa is well-positioned to profit from growing traffic through the centrally located Panama.

As the hub in the airline’s hub-and-spoke model, Panama’s airport serves more destinations than other regional counterparts. For instance, Panama serves 98 international destinations, with its nearest competitor, Mexico, serving just 61.

Copa serves more than 85 destinations in 32 countries, with ~400 daily flights. Copa benefits from what is known as the 6th freedom of the air, or the right to move passengers from one country to another via a layover in a third country (Panama in this case). Copa estimates that ~80% of its city-pair (origin to destination airport) routes are too small for non-stop service. The centrally located Panama airport allows Copa to connect these smaller markets and provide service that would otherwise be unavailable without a hub like Panama.

Copa has also established a strong and defensible market position by connecting secondary cities that lack direct service from U.S. or big Latin carriers.

For example, Copa carries a large portion of traffic between Central and South America. LATAM, with over 20% of all Latin American airline capacity, serves more than 570 routes but does not have the ability to serve smaller markets. Avianca, with roughly half LATAM’s capacity, focuses on Bogotá and connections to North America and Europe.

U.S. carriers such as American Airlines (AAL) and United Airlines (UAL) hold large shares on North-South long-haul routes, but they do not compete for traffic between South American countries.

A Simple Fleet Strategy

Copa’s single-plane fleet of Boeing 737 aircraft creates operational and financial advantages. Specifically,

- it drives economies of scale in maintenance, pilot training, and spare parts.

- the fleet is relatively young and growing younger as new MAX deliveries arrive, which drives superior fuel efficiency, lower maintenance costs, and higher reliability.

- it creates flexibility, as Copa can swap aircraft in and out of routes based on demand without worrying about different crew or gate requirements.

These advantages are shared with the consumer, who enjoys lower-costs, and high performance.

In 2025, Copa’s existing fleet consisted of 124 Boeing 737 MAX and 737 Next Generation (NG) aircraft equipped with winglets and other cost-saving and safety features. Copa is expanding its fleet with an additional 46 Boeing 737 MAX aircraft, which will be delivered between 2026 and 2029.

International Routes Create Additional Competitive Advantages

International routes generally enjoy higher margins from selling more business and first-class tickets and higher average seat prices overall. They also have barriers to entry that you do not see in domestic networks such as:

- traffic right restrictions within bilateral air service agreements,

- uneven, and often partial “open skies” coverage,

- slowing entry into new cross-border markets compared with domestic additions,

- slot scarcity and congestion at major international gateways,

- ownership and control limits, and

- compliance and operating-cost hurdles.

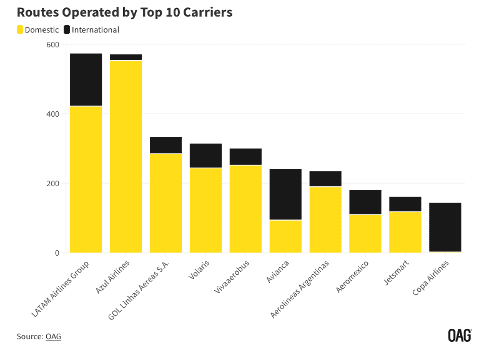

In other words, the more international an airliner, the less competition it faces, and the greater the RPKs they capture. As the most international of the Latin American airlines, Copa earns superior profits.

Figure 2: Domestic Vs. International Routes Operated by Top 10 Latin American Carriers

Sources: OAG

Consistently The Best Airline in the Region

Copa leads most peers in on-time performance (OTP), which measures arrivals within 14 minutes of scheduled arrival time, and completion.

As of November 2025, Copa had the second highest OTP at 88.7% and fourth highest completion factor in Latin America at 99.7%. For reference, the OTP for the region sits at 82.2%.

The company’s success hasn’t gone unnoticed. Copa was recognized by CIRIUM as “The Most Punctual Airline in Latin America” for the 11th time in 2025. Skytrax named it the best airline in Central America and the Caribbean for the tenth consecutive year in 2025. Additionally, in 2023, Copa won Condé Nast’s “Top International Airline” readers’ choice award.

Ultra-Low Cost Provider

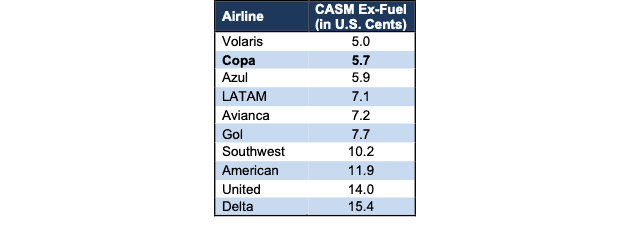

Over the TTM ended 3Q25, Copa’s operating cost per available seat mile (CASM) ex-fuel was 5.7 cents, or second best amongst its peers.

For reference, Delta Air Lines (DAL), United Airlines (UAL), American Airlines (AAL), and Southwest Airlines (LUV) have CASM ex-fuel of 15.4 cents, 14 cents, 11.9 cents, and 10.2 cents, respectively, over the TTM ended 3Q25. See Figure 3.

Copa manages costs effectively through its fleet optimization, efficient operations, and competitive cost of labor in the region.

Figure 3: Copa’s CASM Ex-Fuel vs. Peers: TTM ended 3Q25

Sources: New Constructs, LLC and company filings

Copa’s ultra-low-cost model is even more impressive because it supports a full-service model, whereas Volaris is a no-frills, discount airline with denser seating. Copa’s full-service offering, which includes free food and drinks, assigned seating, two-cabin service, and lounges, is more like legacy U.S. airlines.

Leading Profitability and Strong Growth

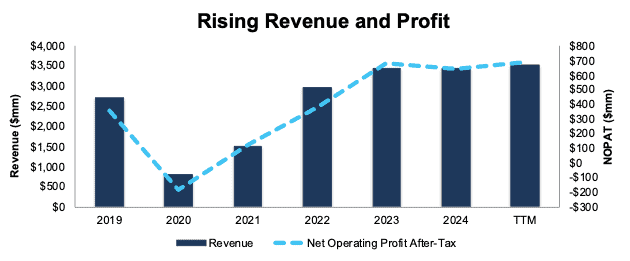

With its central location, international focus, and optimized fleet, Copa has a long history of profit growth.

Since the COVID-19 induced low of 2020, Copa has grown revenue 37% compounded annually through the trailing-twelve-months (TTM) ended 3Q25. Over the same time, Copa improved its net operating profit after-tax (NOPAT) from -$179 million to $689 million.

The company’s NOPAT margin increased from -22% in 2020 to 20% in the TTM ended 3Q25, while invested capital turns improved from 0.3 to 0.8 over the same time. Rising margins and IC turns drives the company’s return on invested capital (ROIC) from -6% in 2020 to 16% over the TTM ended 3Q25.

Longer term, Copa has grown both revenue and NOPAT by 5% compounded annually since 2011.

Figure 4: Copa’s Revenue and NOPAT: 2019-TTM ended 3Q25

Sources: New Constructs, LLC and company filings

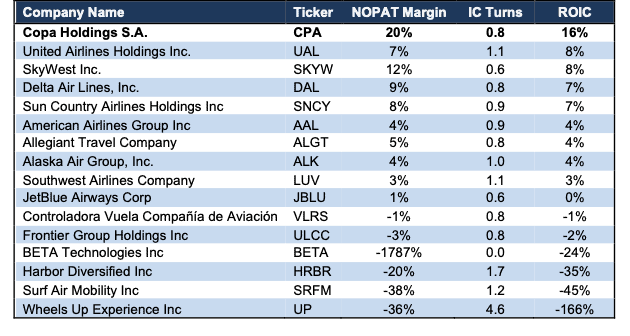

By keeping costs low, Copa not only delivers strong revenue and profit growth, but does so while operating as the most profitable, highest ROIC, company among its peers.

Over the TTM, Copa’s NOPAT margin of 20% and ROIC of 16% rank first among all airline operators under coverage. Markets reward the most efficient capital allocators, and Copa Holdings is poised to be the biggest winner. See Figure 5.

Figure 5: Copa’s Profitability Vs. Peers

Sources: New Constructs, LLC and company filings

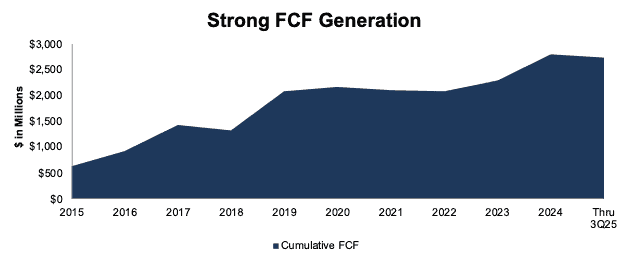

Consistent Cash Flow Generation

Since 2015, Copa has generated $2.7 billion (36% of enterprise value) in cumulative free cash flow (FCF). Over the TTM, Copa generated $73 million in FCF.

Figure 6: Copa’s Cumulative Free Cash Flow Since 2015

Sources: New Constructs, LLC and company filings

Potential for Nearly 5% Repurchase Yield

After reinstating its dividend in 2Q23 (suspended during COVID-19), Copa has increased it from $0.82/share in 2Q23 to $1.61/share in 4Q25. When annualized, the dividend equals $6.44/share and provides investors with a 4.2% yield.

The company also returns capital to shareholders through share repurchases. Since 2021, Copa has repurchased $410 million (6% of market cap) worth of shares.

Copa repurchased $87 million worth of shares in 2024 and $9 million worth of shares in the first three quarters of 2025. As of September 30, 2025, Copa has $104 million remaining under its current share repurchase program. There is no fixed expiration date given for the share repurchase program. It remains in effect until the Board modifies, extends, or terminates it. Should the company repurchase units at the TTM rate ($46 million), it would repurchase shares worth 0.7% of the current market cap over the next 12 months. The combined dividend and repurchase yield would be 4.9%.

It’s worth noting that Copa has repurchased more shares and paid more dividends than its current FCF could fund. Since air travel rebounded from the COVID lows, Copa paid $805 million in dividends and repurchases from 2023 through 3Q25 and generated $664 million in FCF over the same time. However, substantial cash on the balance sheet enables the company to continue to return capital to shareholders.

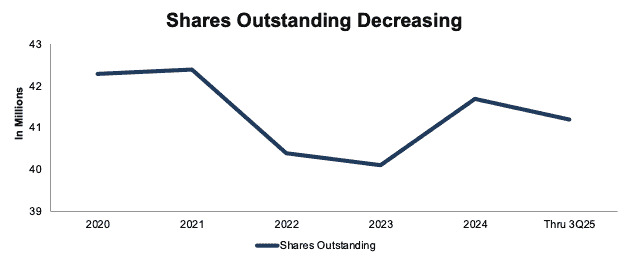

Reducing Shares Outstanding

Copa’s share buyback activity has reduced its shares outstanding from 42.3 million in 2020 to 41.2 million in 3Q25. See Figure 7.

We like companies that choose to return capital to shareholders instead of spending it on costly acquisitions or executive bonuses that rarely drive shareholder value creation.

Figure 7: Copa’s Shares Outstanding: 2020 – 3Q25

Sources: New Constructs, LLC and company filings

Airlines Don’t Have to Be Hazardous to Your Investment Health

Airline revenues are cyclical, and the industry has often been prone to the kind of price competition that gives investor’s nightmares. It is an industry that led Warren Buffett to say it is “hazardous” to one’s investment health. In the wake of the pandemic, the recovery of low-cost carriers (LCCs) and legacy carriers might be construed as reawakening competition for Copa.

Certainly, a revitalized Avianca will fight hard in overlapping markets. LATAM and Delta’s joint venture might funnel premium traffic away from Copa in the U.S.-Southern South America routes. Ultra-LCCs (ULCCs) such as JetSMART could start connecting flights that chip away at Copa’s passenger flows. Additionally, U.S. airlines might use new longer-range narrowbodies (A321XLR) to bypass the need for connections, flying deep into Latin America nonstop, undermining Copa’s one-stop offering.

However, all these threats are speculation at this time, and history has shown that Copa’s competitive advantages are not easily overcome. Avianca’s hub in Bogotá cannot serve all of Copa’s cities, with Bogotá only currently serving 54 destinations, compared to Panama’s 98. The costs to achieve parity, in terms of capital expenditures and time, make it unlikely that Avianca or any other airline can directly replace Copa’s hub-and-spoke model in the near-term. Copa’s niche shields it from much of the competition that it would ordinarily face.

In addition, rising industry consolidation stymies the argument that competition is growing. Rather, it is gradually diminishing, a phenomenon that not only slows price competition, but also supports a trend toward higher industry profitability.

Best of all, these concerns, and more, are already priced into Copa’s stock price. In fact, even if profits never grow as fast as historical rates, the stock has upside potential, as we’ll show below.

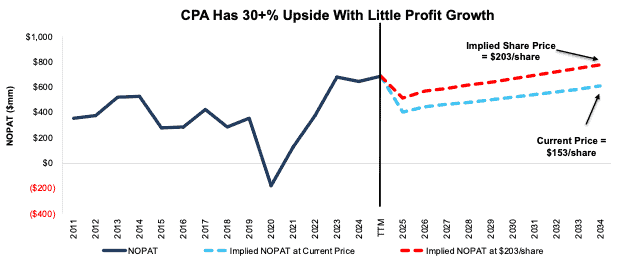

Current Price Implies a Permanent Collapse in Profits

At the current price of $153/share, Copa’s price-to-economic book value (PEBV) ratio is 0.8. This ratio means the market expects the company’s NOPAT to permanently decline 20% from TTM levels. This expectation seems overly pessimistic given constrained supply, strong unit economics, visible capacity growth, and Copa’s history of growing NOPAT by 5% compounded annually since 2011.

Below, we use our reverse discounted cash flow (DCF) model to analyze expectations for different stock price scenarios for CPA.

In the first scenario, we quantify the expectations baked into the current price. If we assume:

- NOPAT margin falls to 11% (compared to 19.5% in the TTM) from 2025 through 2034,

- revenue grows at consensus rates in 2025 (5.4%) and 2026 (10.3%), and

- revenue grows 4% (compared to 5% compounded annually since 2011) each year thereafter through 2034, then

the stock would be worth $153/share today — equal to the current price. In this scenario, Copa’s NOPAT would fall 1% compounded annually from 2024-2034. Contact us for the math behind this reverse DCF scenario.

Shares Could Go 30%+ Higher Even If Profits Grow Less Than Historical Rates

If we assume that:

- NOPAT margin immediately falls to 14% (below post-COVID annual average of 15%) through 2034,

- revenue grows at consensus rates in 2025 (5.4%) and 2026 (10.3%), and

- revenue grows 4% each year thereafter through 2034, then

the stock would be worth $203/share today – a 33% upside to the current price. In this scenario, Copa’s NOPAT would grow just 2% compounded annually from 2024-2034. Contact us for the math behind this reverse DCF scenario.

Should Copa’s NOPAT grow more in line with historical levels, then its stock has even more upside.

Figure 8 compares Copa’s historical NOPAT to the NOPAT implied in each of the above scenarios.

Figure 8: Copa’s Historical and Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

Sustainable Competitive Advantages That Will Drive Shareholder Value

Here’s a summary of why we believe the moat around Copa’s business will allow it to continue generating NOPAT above what the current market valuation implies:

- Panama’s central location makes Copa’s hub-and-spoke model more efficient.

- Copa’s full-service offerings supported by its ultra-low-cost structure is unique and enables the company to deliver a rare combination of higher quality service at very competitive prices.

- The company’s OTP and completion ratios rank among the best in Latin America and have for a decade.

- The airliner’s ability to serve smaller markets shields it from significant competition.

- Copa single-plane fleet strategy creates cost savings.

What Noise Traders Miss with Copa

These days, fewer investors focus on finding quality capital allocators with shareholder-aligned corporate governance. Due to the proliferation of noise traders, the focus is on short-term technical trading trends while more reliable fundamental research is overlooked. Here’s a quick summary of what noise traders are missing:

- the growing demand for air travel in Latin America,

- said demand outpacing airline fleet growth, and

- Copa’s valuation implies a permanent 20% drop in NOPAT.

Organic Growth Could Send Shares Higher

Copa Holdings is positioned to drive growth through disciplined organic investments and leveraging its Hub of the Americas in Panama. The company is expanding its fleet with Boeing 737 MAX 8, which will bring its aircraft count to 132 by the end of 2026.

These additional aircraft support management’s projected capacity growth of 11-13% in 2026. 40% of this projected growth is expected from frequency additions on high-demand routes and 10% from new market entries including.

These capacity additions are further supported by strong underlying demand, as evidenced by load factors averaging 88% in Q3 2025. Panama’s airport is also advancing its next phase of expansion, including T2 terminal expansion and airspace redesign over the next three to four years, which provides Copa with the infrastructure to continue scaling its hub model.

Beyond network expansion, Copa is pursuing revenue enhancement through improved digital merchandising of ancillary products, particularly baggage fees, business class upgrades, and its Economy Extra premium cabin. As these initiatives mature alongside fleet densification (increasing seating capacity within existing planes) the company can drive revenue and profit growth while maintaining its industry-leading unit costs and margins, which would drive shares even higher.

Exec Comp Could Be Improved

Copa awards restricted stock and stock options to executives, key employees, and directors, with awards typically vesting over three to five years. However, the program relies entirely on time-based vesting without explicit performance conditions.

We would prefer the company tie executive compensation to ROIC. Doing so ensures that executives’ interests are more aligned with shareholders’ interests as there is a strong correlation between improving ROIC and increasing shareholder value. Improving ROIC requires attention to all areas of the business, so including it in an executive compensation plan would incentivize executives to improve the entire business, not just the stock performance or one earnings number.

Despite using share-based compensation incentives, Copa’s management has grown economic earnings, the true cash flows of the business, from $134 million in 2015 to $384 million over the TTM.

Insider Trading and Short Interest Trends

NASDAQ has not recorded any insider purchases or sales in the last 12 months.

There are currently 1.7 million shares sold short, which equates to 4% of shares outstanding and six days to cover.

Attractive Funds That Hold CPA

There are no funds in our coverage universe that receive an Attractive-or-better rating and allocate significantly to CPA.

This article was originally published on February 11, 2026.

Disclosure: David Trainer, Kyle Guske II, and Joseph Noko receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.