This week’s Danger Zone is a company that claims consistent profitability and continued success, despite years of shareholder value destruction. Misleading non-GAAP results, large losses, and an overvalued stock price land 8x8 in the Danger Zone.

But what happens when a once profitable company makes the transition to the cloud and has become largely unprofitable? That company, Interactive Intelligence (ININ) is in the Danger Zone this week.

We’ve been sounding the alarm on non-GAAP earnings for several years now. Companies exploited the wide leeway granted by the SEC to present their business in a more favorable light.

To derive economic earnings, 30+ adjustments must be made to accounting earnings. These adjustments remove items hidden in the footnotes and MD&A of annual filings and close loopholes within GAAP accounting.

We know that Valeant is not the only company with misaligned executive incentives. There are many others, many of which have already been put in the Danger Zone and some who will go into the Danger Zone soon. This week, however, compensation committees land in the Danger Zone because of the role they play in creating the problems that lead to shareholder value destruction.

We’ve been highlighting the dangers of Valeant for over two years and we do not see them abating. As long as management is incentivized to destroy shareholder value, Valeant is in the Danger Zone.

It is almost becoming an expected event every quarter: Netflix releases quarterly earnings amid much speculation about its future, and the price soars.

This article is the third in a four part series that walks readers through how to rate and value a stock. Our third step to gauge the value of a company is to determine its economic earnings.

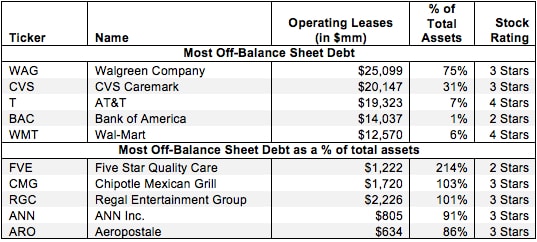

Investors who ignore off-balance sheet debt are not holding companies accountable for all of the capital invested in their business. By adding back off-balance sheet debt to invested capital, one can get a true picture of the value that management is creating for shareholders. Diligence pays.

This article details the uniquely rigorous diligence behind each of our ratings on 3000 stocks, 7000 mutual funds and 400 ETFs. It contains reports on all the adjustments we make to convert GAAP data to economic earnings and derive true shareholder value in a discounted cash flow model.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

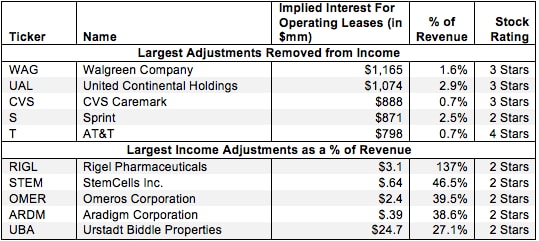

Non-operating items in operating income are unusual gains that don’t appear on the income statement because they are bundled in other line items. Without careful footnotes research, investors would never know that these non-recurring income items distort GAAP numbers by artificially raising operating earnings.

Listen in on my 15 minute interview describing the rigorous diligence New Constructs applies to every rating on the stocks, ETFs and mutual funds we cover.

David A. Geracioti, Editor-In-Chief of Registered Rep magazine, recently invited me for an interview on why economic earnings matter when selecting stocks, mutual funds and ETFs.

Most of my research and publishing tends to focus on companies manipulating accounting rules to make their reported earnings look better than the real economic cash flows of their business.

It is unfortunately rare that I find a company whose economic earnings are outpacing the reported accounting results and whose stock is cheap.

One such company is Lam Research (LRCX – very attractive rating). One of September’s most attractive stocks, LRCX offers investors hidden value.