Editor’s Note: Accounting Standards Update 2016-02 (Topic 842), which requires companies to record operating lease assets and liabilities on the balance sheet, went into effect for calendar year 2019. The adjustments/treatment of operating leases described below pertain to periods prior to 2019. For periods after 2019, we account for operating leases as explained here. Since ASU 2016-02 went into effect, companies have found other ways to continue to hide lease debt from their balance sheets as detailed in Variable Leases Under ASC 842: First Evidence on Properties and Consequences. As a result, we’ve further updated our models to ensure they capture all liabilities related to operating leases, both on and off-balance sheet. Details here.

This report is one of a series on the adjustments we make to convert GAAP data to economic earnings. This report focuses on an adjustment we make to convert the reported balance sheet assets into invested capital.

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rules provide numerous loopholes that companies can exploit to hide balance sheet issues and obscure the true amount of capital invested in a business.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivaled due diligence on 5,500 10-Ks every year for the past decade.

Operating leases, unlike capital leases or debt-financed purchases, are not recognized on the balance sheet. The only trace of operating leases on the financial statements is as a rental expense that is bundled with other items on the income statement (part of this rental expense is an implied interest expense that we remove).

Any lease not meeting all the specific criteria of a capital lease is classified as operating. The current accounting rules provides lots of leeway for companies to classify a lease as operating instead of capital.

These different accounting methods do not reflect operational differences, so we convert all operating leases to capital leases to ensure comparability despite different accounting. We make this adjustment by adding the discounted present value of all required operating lease payments to our calculation of invested capital. This adjustment also ensures that each company is held responsible for earning returns on all the capital invested in the business, not just the assets on the balance sheet.

Currently, the Financial Accounting Standards Board is considering a proposal to require all publicly traded companies in the U.S. to report the value of all operating leases longer than one year on their balance sheets. The proposed treatment would be similar, though not identical, to the way we treat operating leases.

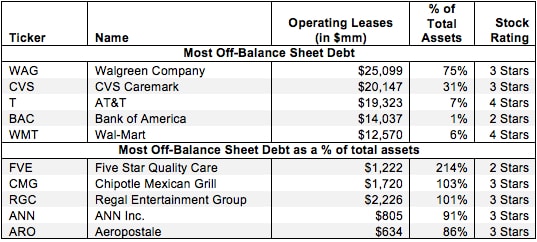

Figure 1 shows the five companies with the most off-balance sheet debt added to invested capital in 2012 and the five companies with the most off-balance sheet debt as a percent of total assets.

Figure 1: Companies With the Largest Off-Balance Sheet Debt Added Back to Invested Capital

Sources: New Constructs, LLC and company filings

Note: Figure 1 excludes companies with less than $500 million in total assets.

All ten companies in Figure 1 have physical stores all over the country that they lease, rather than buy. Airlines are also known for having significant off-balance sheet operating leases. Off-balance sheet debt affects a very broad range of companies. In the fiscal year 2012, 2,793 companies had off-balance sheet debt totaling nearly $760 billion. Dating back to 1996 we have found 33,749 instances of companies with off-balance sheet debt totaling over $7.3 trillion.

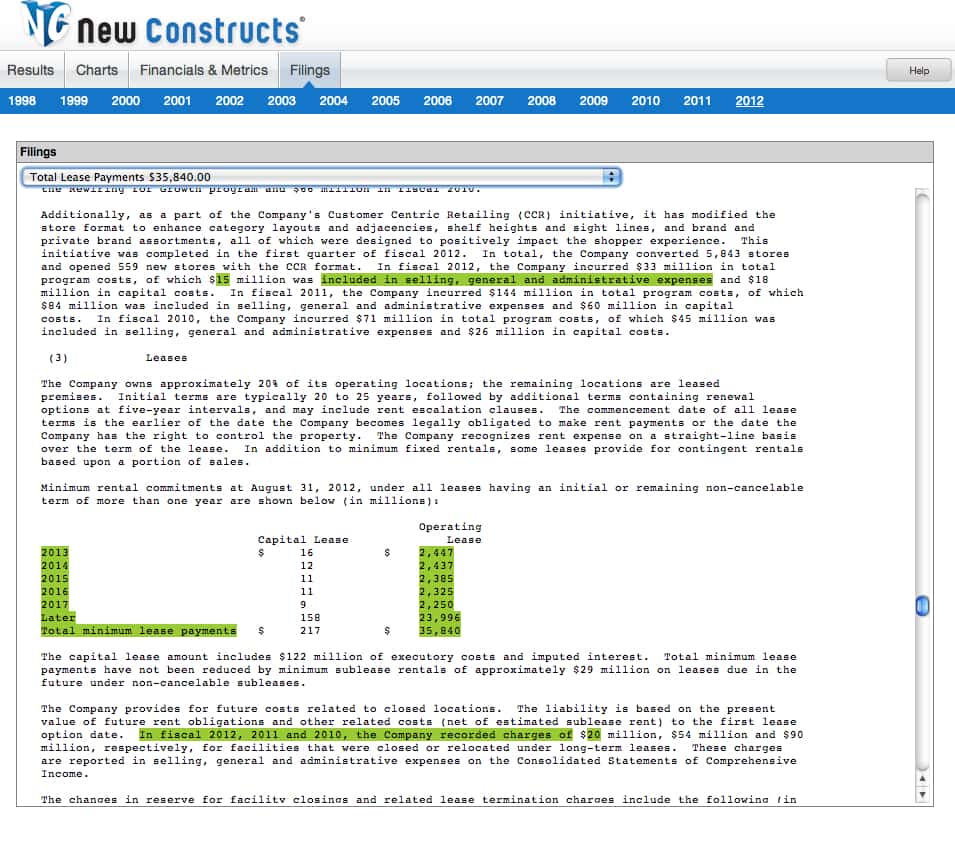

Having significant off-balance sheet debt does not always mean a company is a bad investment. Walgreen Company (WAG) had over $25 billion in off-balance sheet debt last year and earns our Neutral (3-Star) rating. According to its 2012 Form 10-K, WAG leased around 80% of its 8,385 locations. Its minimum obligations on these leases totals over $35.8 billion. By discounting these obligations to their present value, we arrive at WAG’s $25 billion in off-balance sheet debt.

{kind=link}

In certain cases, the presence of off balance sheet debt can significantly alter the investment outlook for a company. Five Star Quality Care (FVE) had the highest ratio of off-balance sheet debt to total assets in 2012. FVE’s $2.3 billion in lease obligations, equivalent to $1.2 billion in debt, were added back to invested capital. Without factoring in this off-balance sheet debt, FVE would have had a top-quintile return on invested capital (ROIC) of 17%. By holding FVE accountable for this capital however, we see that its true ROIC is a much lower 6%, less than its weighted average cost of capital (WACC). Looking at just GAAP data, FVE appears to be a profitable company. Factoring in the true amount of capital invested in the company reveals that on the contrary, it actually makes negative economic earnings.

Investors who ignore off-balance sheet debt are not holding companies accountable for all of the capital invested in their business. By adding back off-balance sheet debt to invested capital, one can get a true picture of the value that management is creating for shareholders. Diligence pays.

Sam McBride contributed to this report.

Disclosure: David Trainer is long WMT. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.

3 replies to "Off-Balance Sheet Debt – Invested Capital Adjustment"

Long-term notes payable or long-term liabilities are loans that are not due for more than a year. Often loans from banks or other financial institutions, these loans are secured by various assets on the balance sheet, such as inventories. Most companies will tell you in a footnote to this item when the debt will become due and the interest rate the company is paying on it.

Hi, thank you very much for these very helpful resources on invested capital. I have a conceptual questions please. Why do you deduct only NIBCL for the calculation of net working capital and not all short term liabilities in your invested capital formula

Thank you very much.

Regards,

Niharika

Niharika, Invested capital should reflect all the money invested in a company over the course of its life and is sourced from debt and/or equity. We include all interest bearing current liabilities in our calculation of invested capital to ensure we capture all debt invested in the business. NIBCLs, on the other hand, aren’t included in invested capital because there is no cost of capital associated with them. Thanks for the question!