Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

With the growth in services and applications moving to the cloud, investors have been quick to buy the stocks of companies that offer cloud-based products, often times regardless of valuation. But what happens when a once profitable company makes the transition to the cloud and has become unprofitable? That company, Interactive Intelligence (ININ: $46/share) is in the Danger Zone this week.

Transition To The Cloud Has Not Fared Well

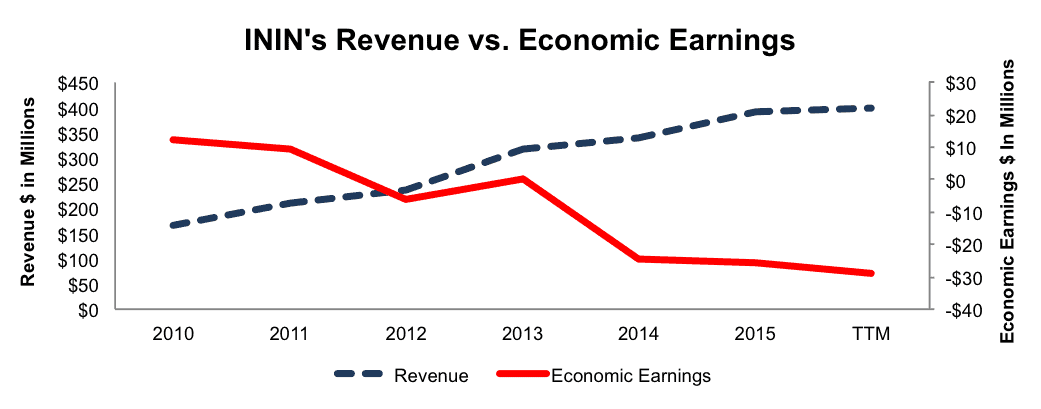

Interactive Intelligence has been around long before some of the new upstart technology companies. In fact, ININ was once a profitable business, and it grew economic earnings, the true cash flows of the business, throughout 2000-2010. This trend changed in 2010 when the company introduced its first cloud-based product, and the fundamentals of the business have only deteriorated since. ININ’s economic earnings have declined from $12 million in 2010 to -$29 million over the last twelve months. Conversely, the company’s revenue has grown from $166 million in 2010 to $401 million over the last twelve months. Figure 1 highlights the divergence of revenue and economic earnings. See the reconciliation of Interactive Intelligence’s GAAP net income to economic earnings here.

Figure 1: Disconnect Between Revenue and Profits

Sources: New Constructs, LLC and company filings

Following the downward trend, Interactive Intelligence’s return on invested capital (ROIC) has declined from an impressive 40% in 2010 to a bottom-quintile -6% over the last twelve months. In a quest to move services to the cloud, Interactive’s profitability has cratered. ININ has also lost a cumulative -$188 million in free cash flow from 2010 to 2015.

Non-GAAP Earnings Can’t Hide Issues

Non-GAAP earnings are not a reliable indicator of a company’s operations and are often used to portray a better business than exists in reality. Here are the expenses ININ removes to calculate its non-GAAP metrics, including non-GAAP gross profit, non-GAAP operating income, adjusted EBITDA, and non-GAAP net income:

- Stock-based compensation expense

- Acquisition-related expense

- Amortization of debt discount and issuance costs

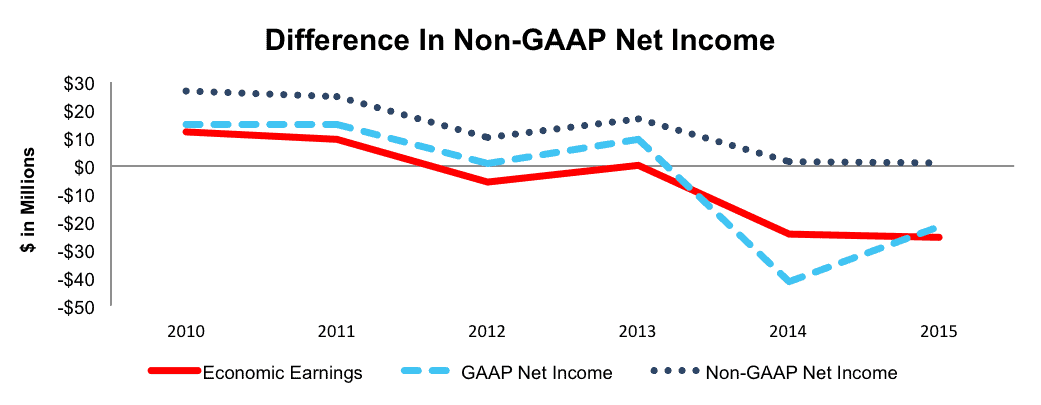

By removing these costs, ININ is able to understate the profit decline that has occurred since 2010. For example, since 2010, ININ’s non-GAAP net income has declined from $26 million to $1 million in 2015. While trending downwards, ININ still reported a positive non-GAAP net income in 2015. In contrast, ININ’s GAAP net income has fallen from $15 million in 2010 to -$22 million in 2015 and economic earnings have declined from $12 million in 2010 to -$26 million in 2015. See Figure 2.

Figure 2: Intelligence Interactive’s Non-GAAP Distorts Reality

Sources: New Constructs, LLC and company filings

Negative Profitability Creates Competitive Disadvantages

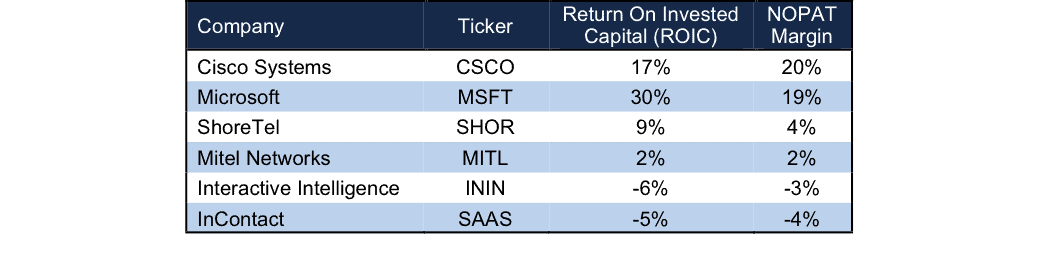

ININ provides on-site solutions as well as cloud based services to the contact center/customer engagement industry. By operating across multiple facets of the industry, ININ faces tough competition from large industry incumbents to smaller startups. Some of ININ’s main competition, as noted in the company’s 10-K, comes from the likes of Cisco (CSCO), Microsoft (MSFT), InContact (SAAS), Mitel Networks (MITL), ShoreTel (SHOR), Five9 (FIVN) and privately held firms Genesys Telecommunications, Avaya, and Aspect Software. Of the competitors covered by New Constructs, each earns a higher ROIC than Interactive Intelligence and all but one have a higher NOPAT margin, per Figure 3. Having a lower margin and ROIC than most of its competition means that ININ cannot compete as well on price. ININ needs to charge higher prices to get margins positive. It cannot afford to lower prices as many of its more profitable competitors can.

Lower margins and ROIC also mean the firm has less ability to invest in R&D and improvement of its offerings.

Figure 3: ININ’s Profitability Lags Behind Competition

Sources: New Constructs, LLC and company filings

Bull Hopes Tied to The Cloud, Acquisition Risk Against The Bear Case

As we’ve seen with many cloud companies placed in the Danger Zone, such as Marketo (MKTO), ServiceNow (NOW), and Splunk (SPLK), the bull case rests largely on revenue growth exceeding expectations and hopes of future profitability. In the case of Intelligence Interactive, the bull case is no different. Bulls believe that as ININ transitions to the cloud, and cloud adoption increases, ININ will be able to reap large profits from operations that have been largely unprofitable to this point. Unfortunately, this belief is hard to justify when looking at the fundamentals of the business, particularly, rising costs and lack of profitability when compared to competition.

Most concerning for bull arguments, apart from the growing losses noted in Figure 1, is the pace at which the costs of transitioning to a cloud provider have grown. Recurring revenue, a staple of cloud based service providers, has grown by 27% compounded annually since 2010. Meanwhile, the costs of recurring revenue have grown by 37% compounded annually over this same time. As ININ has expanded into more cloud services, the costs of these services have overshadowed any increase in revenue.

Across the entire business, not just recurring services, costs are rising faster than revenues as well. Research & development costs, sales & marketing costs, and general & administrative costs grew by 23%, 21%, and 24% compounded annually from 2010-2015 – all of which are higher than Interactive Intelligence’s 19% overall revenue CAGR over this same time.

Further undermining the bull case, the stock is already priced for perfection. The current stock valuation implies that Interactive Intelligence will grow revenues at a significantly faster pace than consensus expectations for over two decades. We’ll highlight Interactive Intelligence’s overvaluation in greater detail below.

The biggest risk to our thesis is that a larger competitor acquires ININ at a value at or above today’s price. As we’ll show below, unless a competitor is willing to destroy shareholder value, an acquisition at current prices would be ill advised.

Acquisition Hopes Rest On Overpayment

We don’t think ININ is an attractive acquisition target at its current price. To begin, ININ has liabilities that investors may not be aware of that make it more expensive than the accounting numbers suggest.

- $73 million in off-balance-sheet operating leases (7% of market cap)

- $19 million in outstanding employee stock options (2% of market cap)

After adjusting for these liabilities we can model multiple purchase price scenarios. Unfortunately for investors, only in the most optimistic of scenarios is ININ worth more than the current share price.

Figures 4 and 5 show what we think Cisco (CSCO) should pay for ININ to ensure the deal is truly accretive to CSCO’s shareholder value. Cisco could be a potential acquirer of Interactive Intelligence to bolster its cloud contact center business. However, there are limits on how much CSCO would pay for ININ to earn a proper return, given the NOPAT or free cash flows being acquired.

Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. In each scenario, we conservatively assume that Cisco can grow ININ’s revenue and NOPAT without spending on working capital or fixed assets. We also assume ININ achieves an 8% NOPAT margin, which is the average of the competition in Figure 3. ININ’s current NOPAT margin is -3%

Figure 4: Implied Acquisition Prices For CSCO To Achieve 7% ROIC

Sources: New Constructs, LLC and company filings.

Figure 4 shows the ‘goal ROIC’ for CSCO as its weighted average cost of capital (WACC) or 7%. Only if Interactive Intelligence can grow revenue 20% each year for the next five years while also immediately raising its NOPAT margin from -3% to 8% over the next five years is the firm worth more than its current price of $46/share. For reference, consensus estimates expect Interactive Intelligence to grow revenue by 11% in 2016 and 13% in 2017. We include the 20% scenario to provide a best-case view. Note that any deal that only achieves a 7% ROIC would be only value neutral and not accretive, as the return on the deal would equal CSCO’s WACC.

Figure 5: Implied Acquisition Prices For CSCO To Achieve 17% ROIC

Sources: New Constructs, LLC and company filings.

Figure 5 shows the next ‘goal ROIC’ of 17%, which is Cisco’s current ROIC. Acquisitions completed at these prices would be truly accretive to CSCO shareholders. Even in the best-case growth scenario, the most CSCO should pay for ININ is $19/share (59% downside). Any deal above $19/share would lower CSCO’s ROIC.

Without A Takeover, Growth Expectations Remain Overly Optimistic

Barring acquisition, to justify its current stock price of $46/share, ININ must immediately achieve positive NOPAT margins of 2.3% (average of last five years, compared to -3.4% TTM) and grow revenue by 20% compounded annually for the next 14 years.

Even if we assume ININ can reach scale with its cloud products and achieve a 4% NOPAT margins, above current margins but below competition with other, more profitable business lines, the stock is still overvalued. If ININ can achieve 4% NOPAT margins and grow revenue by 14% compounded annually for the next decade, the stock is worth only $31/share today – a 33% downside. Each of these scenarios also assumes the company is able to grow revenue and NOPAT without spending on working capital or fixed assets, an assumption that is unlikely, but allows us to create a very optimistic scenario. For reference, since 2010, ININ’s invested capital has grown by about $40 million (13% of revenue) per year.

Catalyst: Revenue Expectations Fall Short

We don’t need to look far for evidence that investor sentiment can change quickly in regards to ININ. In 2014, ININ fell nearly 50% from March to October as revenue came in below expectations and guidance was lowered. After falling further through 2015, ININ is up 44% year-to-date and investors have bought into the cloud hype once again. The only difference between then and now is that ININ is losing more money now as more people pay attention to non-GAAP metrics.

ININ reported 1Q16 revenue that came in below expectations, but the stock did not react nearly as negatively as in the past. If ININ reports another revenue miss, especially after the miss in Q1, the market could quickly realize that the hopes behind the bull case just aren’t enough to support the stock at its current valuation. Investors are willing to look past losses when revenue is growing at an impressive pace, but when the revenue growth slows, those same investors are quick to jump ship.

A longer-term catalyst to watch for is whether ININ can continue to develop cloud services that meet customer needs given the investment that will be required. We mention this possible catalyst after Aspect Software, a competitor in the contact center industry, filed bankruptcy in March 2016. During bankruptcy proceedings, Aspect Software CEO noted that “staying on the cutting edge of software solutions has been especially challenging.” In light of this bankruptcy, it’s worth noting that since 2010, Interactive Intelligence’s debt, including off balance sheet debt, has grown from $29 million to $192 million over the last twelve months. While Aspect Software held more debt than ININ, the bankruptcy is a warning sign for the industry that being profitable is not easy. With debt adding up and losses growing, one must question whether it’s only a matter of time before ININ is unable to stay up to date with the latest technology and risk losing customers, revenue, and ultimately, any hopes of profitability.

Insider Sales and Short Interest Remains Low

Over the past 12 months 33 thousand shares have been purchased and 48 thousand have been sold for a net effect of 15 thousand insider shares sold. These sales represent <1% of shares outstanding. Additionally, there are 2.2 million shares sold short, or 10% of shares outstanding.

Executives Are Incentivized With Poor Target Goals

Apart from base salaries, executives at Interactive Intelligence receive cash bonuses, paid quarterly, for achieving “gross profits on orders” and operating cash flow targets. The gross profit bonus is paid provided executives achieve only 85% of the target goal. Similarly, the cash flow bonus is paid provided OCF is no worse than $10 million below the target. In either manner, executives are given bonuses in instances where they don’t actually meet the target. Long-term stock awards are given in the form of time based RSUs and performance based RSUs. The performance based RSUs vest according to the target goals established for cash bonuses.

In either case, bonuses are given based on metrics that don’t directly equate to profits or shareholder value creation. The best way to create shareholder value, and align executives with the best interest of shareholders, is to tie performance bonuses to ROIC. The reason for using ROIC as the target metric is that there is a clear correlation between ROIC and shareholder value.

Impact of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to Interactive Intelligence’s 2015 10-K:

Income Statement: we made $13 million of adjustments with a net effect of removing $13 million in non-operating expenses (3% of revenue). We removed $13 million related to non-operating expenses and made no adjustments related to non-operating income. See all adjustments made to ININ’s income statement here.

Balance Sheet: we made $259 million of adjustments to calculate invested capital with a net decrease of $85 million. The most notable adjustment was $73 million (22% of net assets) related to operating leases. See all adjustments to ININ’s balance sheet here.

Valuation: we made $390 million of adjustments with a net effect of decreasing shareholder value by $34 million. One of the largest adjustments was the removal of $191 million (19% of market cap) due to total debt, which includes $72 million in off-balance sheet debt.

Dangerous Funds That Hold ININ

The following funds receive our Dangerous-or-worse rating and allocate significantly to Interactive Intelligence

- Brown Advisory Small-Cap Growth Fund (BAFSX) – 2.1% allocation and Dangerous rating.

- RBC Enterprise Fund (TETAX) – 1.9% allocation and Very Dangerous rating.

This article originally published here on June 13, 2016

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Photo Credit: wikipedia