Structural underinvestment left global oil supply one shock away from a crisis, and the Hormuz blockage is that shock. With no quick fix to supply constraints, high and volatile oil prices aren’t going away, and neither is the incentive to invest in oil and gas.

This week’s Long Idea features a leading manufacturer that supplies the “picks-and-shovels” that oil and gas drilling programs require. With a differentiated service model, high profitability, and strong shareholder return, the company offers Attractive risk/reward in an industry with long-term growth prospects.

Below, we provide an excerpt from our latest Long Idea report. You can buy the full report a la carte here.

We’re not giving you the ticker for this pick, but this excerpt shows how thorough we are.

This stock presents quality Risk/Reward based on the company’s:

- global manufacturing footprint positions it as the dominant supplier in a growing market,

- differentiated service model that creates high switching costs,

- high profitability, including an ROIC nearly double peer averages,

- attractive capital return and shareholder yield, and

- cheap valuation that implies just 10% profit growth despite structural tailwinds.

Higher Oil Prices Are Back

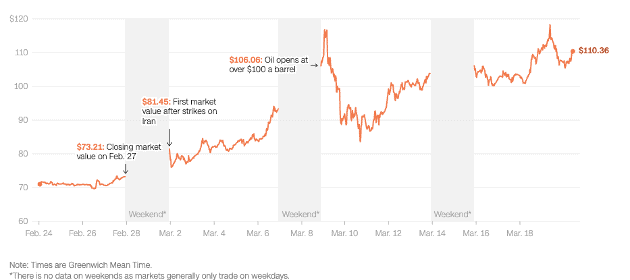

The February 28, 2026 U.S.-Israeli strikes on Iran and the subsequent closure/blockage of the Strait of Hormuz have created what the International Energy Agency (IEA) has called, “the largest supply disruption in the history of the global oil market”.

Approximately 20 million barrels per day (mb/d) of crude oil and petroleum products normally transit The Strait. The IEA estimates global oil supply is down ~8 mb/d in March. Chevron CEO Mike Wirth recently noted that the oil futures market has not fully priced in the scale of the supply disruption.

Brent crude has surged from $72 per barrel (bbl) the day before the war to ~$100/bbl, with some analysts projecting spikes to as much as $200/bbl if the disruption persists.

Figure 1: Brent Crude Oil Price: Feb-Mar 2026

Sources: CNN

Elevated Prices Drive Investment

Higher and more volatile oil prices drive drilling activity and accelerate inventory restocking. At $100+ oil, virtually every shale play in the U.S. is economically profitable, offshore deepwater projects attract fresh capital, and national oil companies in the Middle East and Latin America accelerate capacity expansion.

These actions drive orders straight to this company.

Even prior to the Iran War, Goldman Sachs estimated that the average Brent/WTI crude prices would recover to $80/$76/bbl by late 2028 and spark investment to:

- bring supply in line with demand by the early 2030s,

- make up for natural declines of old fields, and

- meet demand expected to grow through 2040.

A multi-year period of elevated prices, even if below the current $100+ spike, would drive sustained drilling activity and demand at levels well above the cyclical trough.

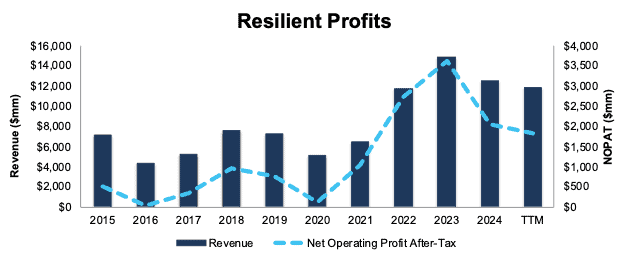

Persistent Profits Throughout Cycles

Through three major oil price shocks, the 2014-2016 OPEC price war, the 2020 COVID collapse, and the 2022 Ukraine war spike, this company remained profitable when prices fell and its profits soared when prices rose.

At the 2016 trough, when WTI averaged $43/bbl, the company’s net operating profit after-tax (NOPAT) fell to $47 million but never turned negative. The company’s NOPAT surged from $122 million in 2020 to $3.6 billion in 2023. Most impressively, the company has generated positive NOPAT in every year back to 2004, the first year we have data.

Over the past decade, the company has grown revenue and NOPAT by 5% and 13% compounded annually, respectively. The company’s NOPAT margin improved from 7% in 2015 to 16% over the TTM while invested capital turns improved from 0.5 to 0.7 over the same time. Rising margins and IC turns drive return on invested capital (ROIC) from 4% in 2015 to 11% over the TTM.

Figure 5: Revenue and NOPAT: 2015-TTM

Sources: New Constructs, LLC and company filings

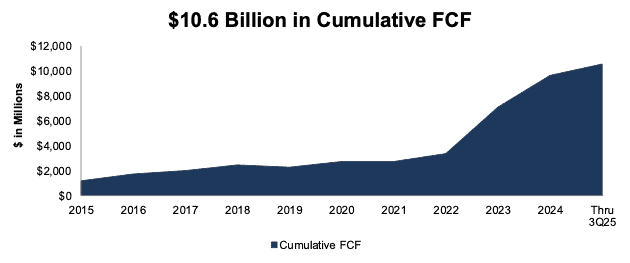

A Cash Flow Machine

Over the past decade, this company has generated $10.6 billion (40% of enterprise value) in cumulative free cash flow (FCF).

Over the TTM, the company generated $1.6 billion in FCF.

Figure 7: Cumulative FCF: 2015-3Q25

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.