Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and MarketWatch.com.

LinkedIn (LNKD) is in the Danger Zone this week. LNKD continues our theme of hot stocks that have overshot their fair valuations. So far this year, LNKD is up 110% while the S&P 500 (SPY) is only up 15%. LNKD is a high-momentum stock in a popular sector, so investors are turning a blind eye to its competitive weaknesses and high valuation. Most people are aware that LNKD is expensive compared to its current earnings, but few people seem to aware of its off-balance sheet liabilities and the alarming level of profit growth implied by its stock price.

Competitive Advantages…Not Really

There have been numerous articles like this one over the past few months arguing that LinkedIn is going to be a dominant web player in the near future. While LinkedIn certainly offers a useful service and boasts an impressive user base, it has a number of formidable competitors in the fields of professional networking and publishing.

Facebook (FB) and Twitter still boast higher use among job seekers than LNKD. Both these companies offer a multitude of apps and tools to help potential job seekers, and their user bases significantly exceed LNKD. Smaller companies such as Monster.com (MWW) also have many users. It doesn’t appear that LNKD has a major advantage in this space.

LNKD also faces significant competition as a tool for professional networking. LNKD is the biggest social media site for professionals, but it far from the only one. Just look at this list of 20 other sites offering similar services. More specialized sites that cater to professionals in specific industries could potentially take a bite out of LNKD’s user base.

Most of LinkedIn’s utility comes from access to its members and their contributions. I am not sure how much incremental utility or value that LinkedIn adds. The company is trying to package the content of its members and serve as a news aggregator as well, but in both cases the site just serves as the platform for someone else’s content. There are too many sites already serving as aggregators of content for LNKD to really achieve a dominant position in this space.

The point is that success for LinkedIn requires more than just building a big following. The company must monetize that following. Given its competition and the lack of substantive value-add to its members, I have a hard time seeing how LinkedIn will monetize what it has built so far.

Valuation Is Utterly Disconnected From Reality

I focus on LinkedIn’s need to monetize its network because the valuation of its stock implies the company will do so at rather astounding levels.

My point is that even if you believe LinkedIn will monetize its network, I think it is hard to make a straight-faced argument that it will do so to the degree already baked into its stock price.

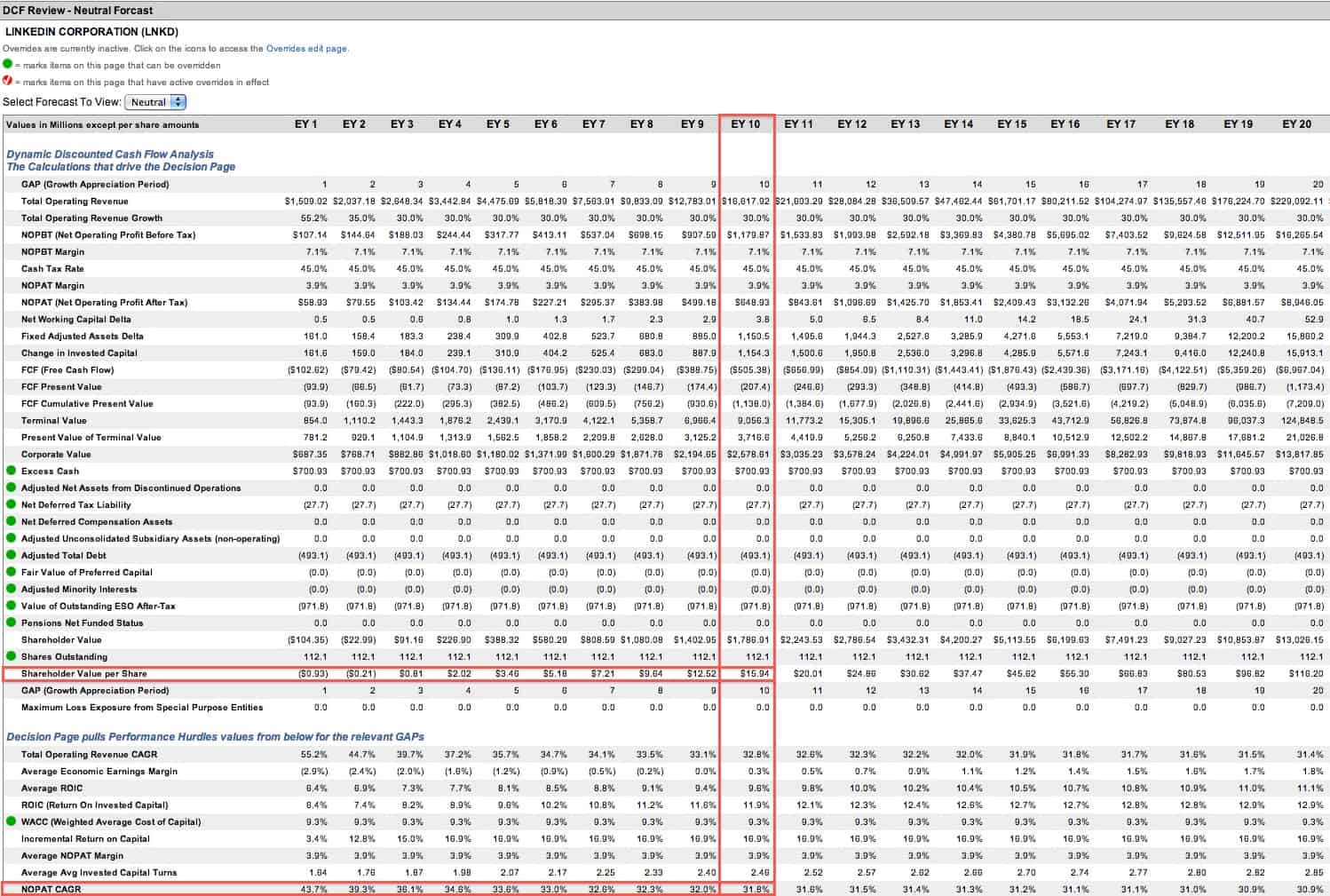

To justify its current valuation of ~$240/share, LNKD must grow after tax profit (NOPAT) by 30% compounded annually for 24 years.

If LNKD actually grew by that much, it would have $800 billion in revenue and nearly $30 billion in NOPAT. For comparison, Google (GOOG) had $50 billion in revenue and $11 billion in NOPAT in 2012. Investors in LNKD are betting on the company becoming significantly larger than Google is now. I don’t see the same level of innovation and differentiation at LNKD to make that kind of growth possible.

Simply put, the magnitude of success implied by LNKD’s stock price is too large to accommodate any argument that the company is currently fairly valued. Even fairly optimistic growth scenarios still leave significant downside for the company. Here are a few growth scenarios and the value of the stock if they come true.

1) ~30% compounded annual growth rate (CAGR) for NOPAT for 10 years = ~$15/share

{kind=link}

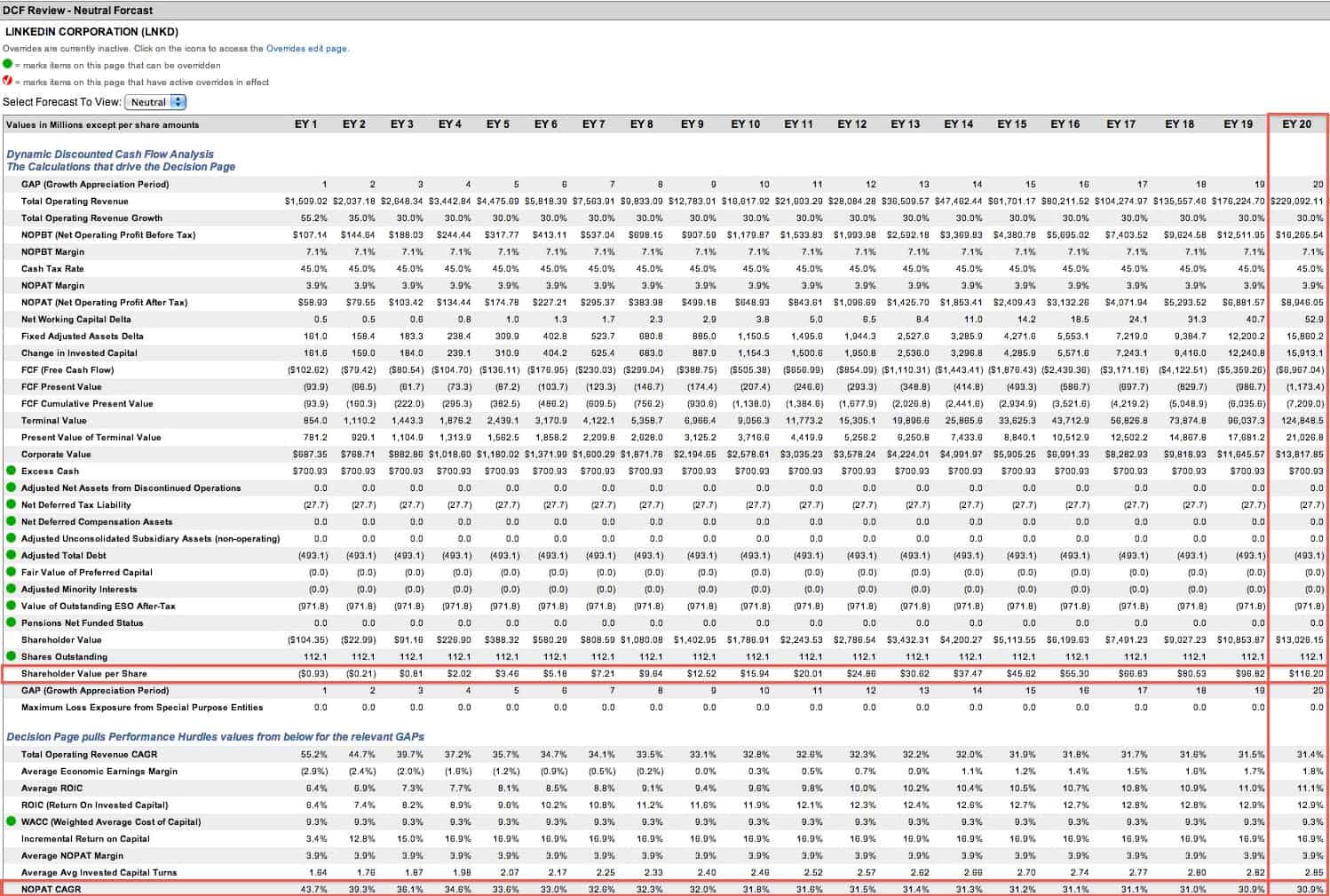

2) ~30% NOPAT CAGR for 20 years = ~$115/share

{kind=link}

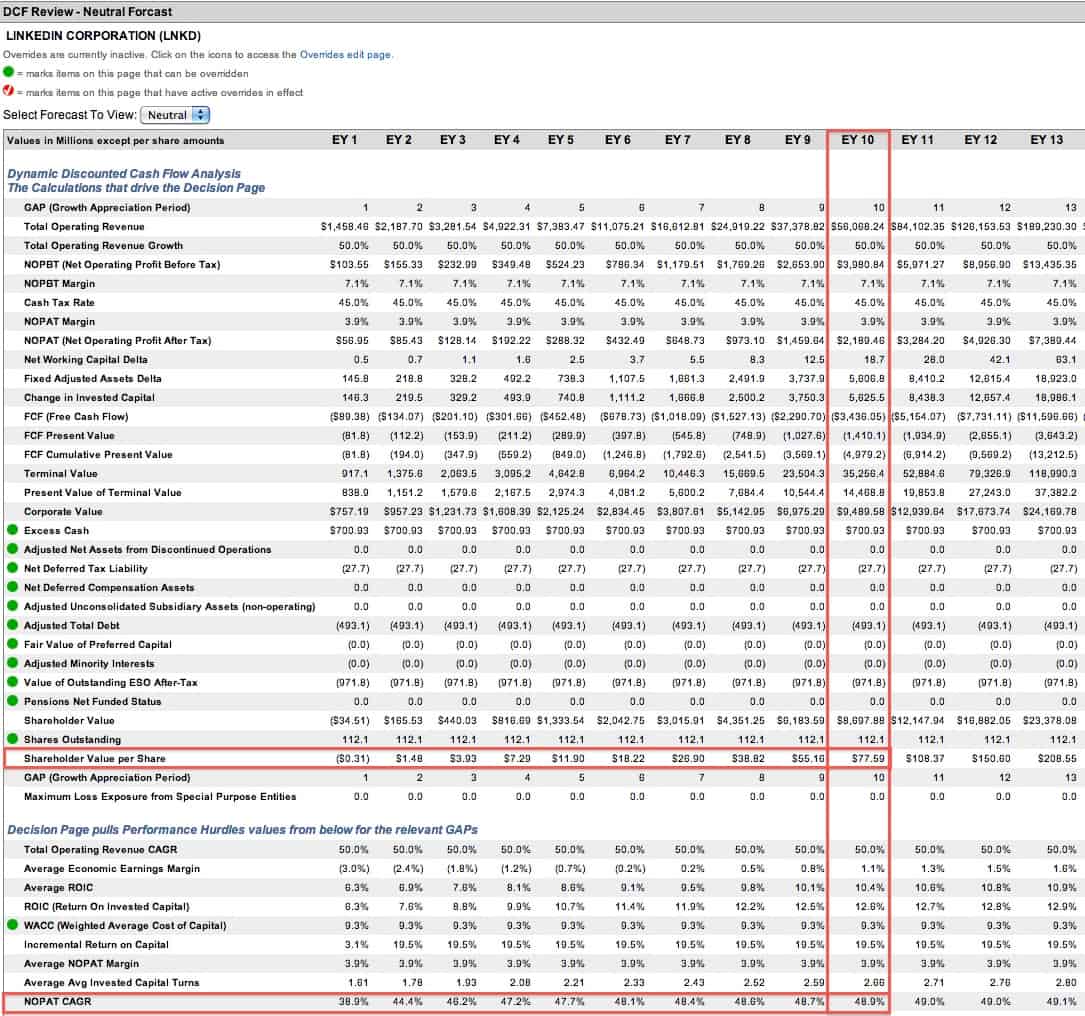

3) ~50% NOPAT CAGR for 10 years = ~$80/share

{kind=link}

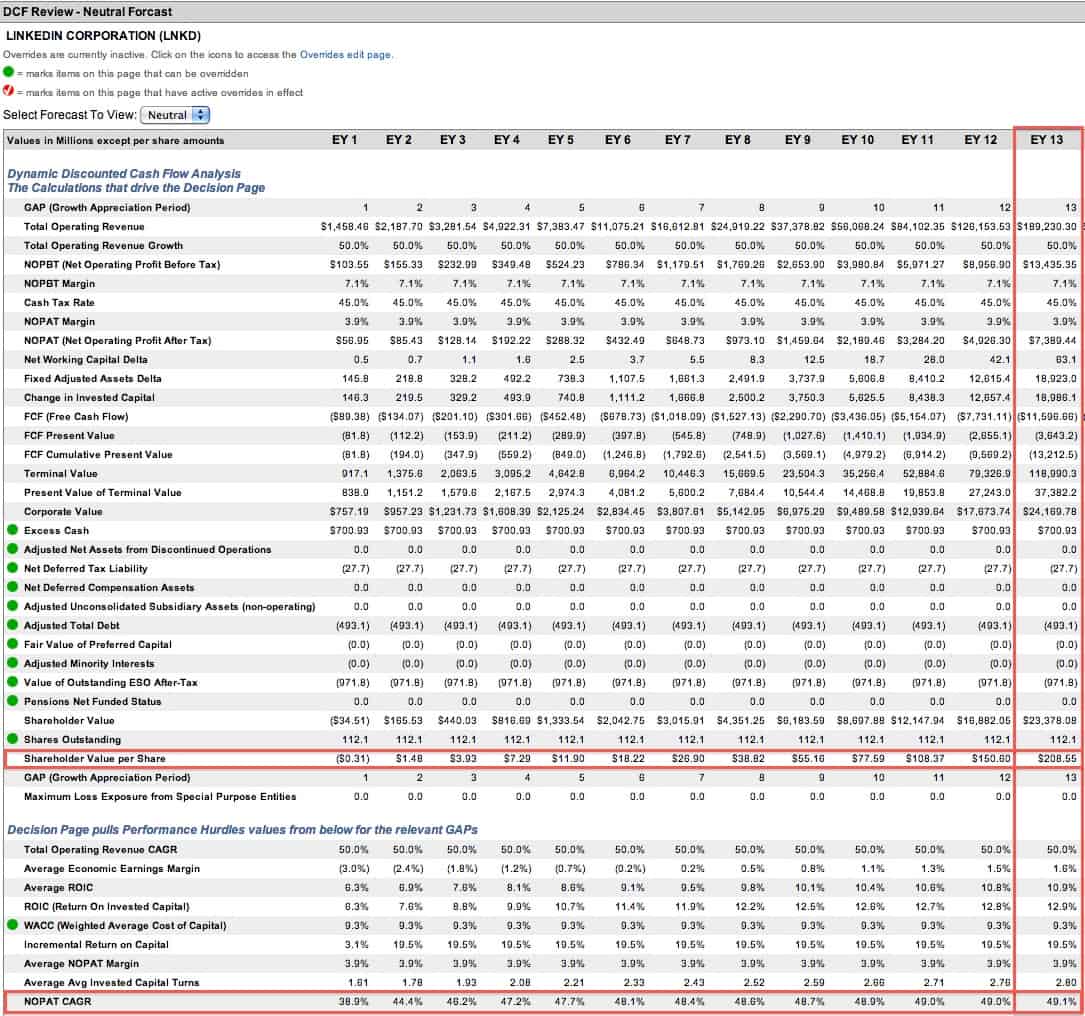

4) ~50% NOPAT CAGR for 13 years = ~$210/share

{kind=link}

There is something wrong when 50% profit growth compounded annually over 13 years results in a value 12% below the current price. Even if LinkedIn does manage to fully monetize its user base—which is far from a given—the level of growth required to justify its stock price is simply too high for it be fairly valued.

Red Flags

LNKD also has some liabilities hidden in its footnotes that decrease the value of future cash flows attributable to shareholders. Like most fast-rising tech stocks, LNKD has numerous outstanding employee stock options that dilute the value of existing shares. We calculate the liability of these outstanding options to be roughly $1 billion.

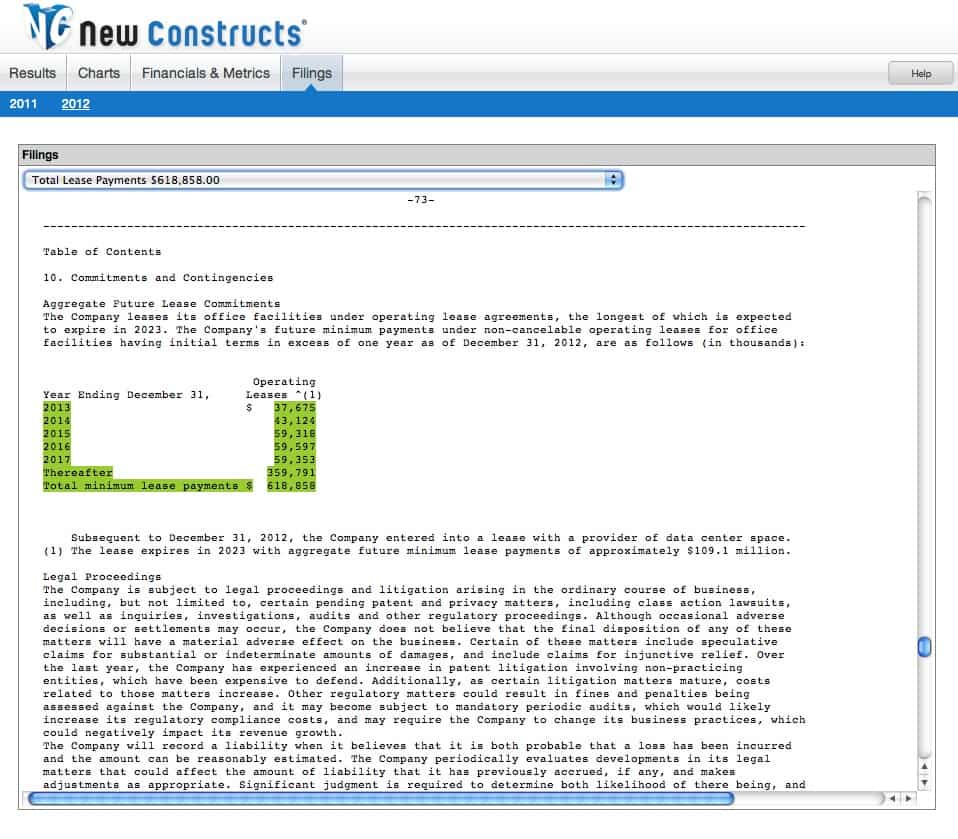

LNKD also leases all its office facilities, leading to a significant amount of off-balance sheet debt. We discount LNKD’s $620 million in lease obligations to their present value, so the total amount of off-balance sheet debt is around $500 million.

{kind=link}

These two liabilities combined represent about 5% of LNKD’s market-cap, which wouldn’t be that big a deal except for the fact that LNKD’s market cap is already very inflated. Compared to the present operations of the company, these liabilities appear much more significant. At $1.5 billion, they represent roughly 150% of reported net assets.

Considering these liabilities and the inflated valuation, it’s hard to make a serious case for LNKD as a long-term investment. Momentum investors hoping to make money by selling LNKD to a “greater fool” run the risk of being left high and dry when the stock corrects to a more realistic value. For those investors who’ve made handsome returns on LNKD this year, now is a good time to take those profits and look for better value elsewhere.

Avoid These ETFs and Mutual Funds

Investors should avoid the following ETFs and mutual funds due to their significant allocation to LNKD and Dangerous-or-worse rating.

1) Berkshire Focus Fund (BFOCX): 7.0% allocation to LNKD and Dangerous rating

2) PowerShares Dynamic Media (PBS): 6.7% allocation to LNKD and Dangerous rating

3) Dunham Focused Large Cap Growth Fund (DAFGX, DCFGX, DNFGX): 5.9% allocation to LNKD and Dangerous rating

LNKD is set up for a significant drop at its current valuation, and if it falls it will bring these funds down with it.

Sam McBride contributed to this report.

Disclosure: David Trainer is short LNKD. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.

1 Response to "Danger Zone 8/30/13: LinkedIn (LNKD)"

LNKD down nearly 25% after hours on disappointing guidance. Now down 38% since original Danger Zone.