This company holds peer-leading profitability, 15 years of inventory at break-evens well below projected prices, and a strong shareholder capital return program. Yet, its stock is priced as if profits will permanently fall 60% from TTM levels.

The disconnect between business fundamentals and stock valuation provide Very Attractive Risk/Reward.

Below, we provide an excerpt from our latest Long Idea report to show how our research finds opportunities the market is missing. Get the full report a la carte here. Learn how our Long Ideas drive our #1 ranking for stock picking.

This stock presents quality Risk/Reward based on the company’s:

- position to profit from steady global demand for natural gas and steadily rising prices,

- inventory with a break-even well below EIA’s long-term forecast of prices between $4-6 MMBtu,

- peer-leading profitability,

- strong free cash flow that supports shareholder return, and

- cheap stock price that implies permanent profit decline.

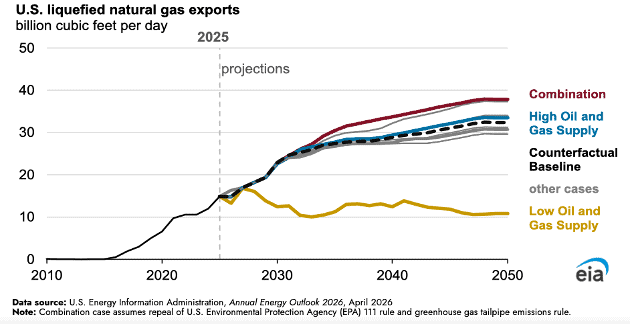

LNG Exports Put Upward Pressure on Prices

U.S. liquified natural gas (LNG) exports are the long-term force draining domestic storage. The EIA forecasts “most” of the 20-40% growth in natural gas production between 2025 and 2050 will serve international markets.

The EIA projects U.S. LNG exports will grow from 15 billion cubic feet per day (Bcf/d) in 2025 to more than 30 Bcf/d in 2050. The growth in exports tightens U.S. supplies and puts upward pressure on domestic prices.

Figure 1: U.S. LNG Exports Expected to Rise Through 2050

Sources: EIA

Higher Prices Will Persist

Greater demand for U.S. LNG and natural gas, along with continued domestic consumption supports higher overall U.S. prices.

The EIA anticipates Henry Hub spot prices averaging $3.50/MMBtu in 2026 and $3.18/MMBtu in 2027 due to higher Permian gas-to-oil ratios and delays in train 2 and 3 of the Golden Pass facility.

The Henry Hub futures curve confirms a similar near-term path, but shows consistent premium prices during winter periods. As of May 18, 2026, the January 2027 contract settled at $4.58/MMBtu, with each December, January, and February contract from 2026 through 2031 settling above $4/MMBtu.

Longer-term, the EIA expects Henry Hub spot prices will range between $5/MMBtu and $6/MMBtu across the early 2030s.

Strong Profit Growth

This company has grown both revenue and net operating profit after-tax (NOPAT) by 7% compounded annually since 2022.

Since natural gas pricing bottomed in 2024, the company’s NOPAT margin improved from 12% in 2024 to 41% in the TTM. The company’s invested capital (IC) turns, a measure of balance sheet efficiency, increased from 0.4 to 0.7 over the same time.

Improving NOPAT margins and IC turns drive the company’s return on invested capital (ROIC) from 5% in 2024 to 28% over the TTM.

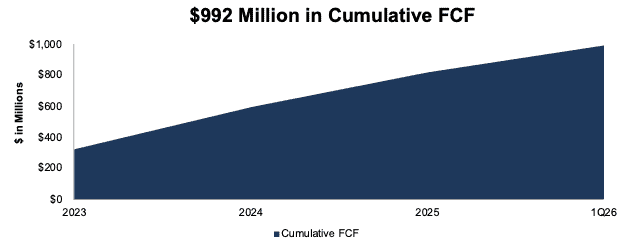

Strong Free Cash Flow Too

The company’s cash flow generation easily covers its repurchase activity.

From 2023 through 1Q26, the company generated $992 million in free cash flow (FCF), which equals 24% of the company’s enterprise value. See Figure 8 from the full report.

The $992 million in FCF since 2023 is more than enough to cover the company’s $808 million in share repurchases over the same time.

Figure 8: Cumulative FCF: 2023 – 1Q26

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

Want one full Long Idea and one Danger Zone report delivered directly to your inbox each month? Our Long Idea & Danger Zone Report Bundle is now open to investors at a sharp discount for the first time.