The decline in the number of refineries and global oil supply constraints are driving strong profit growth for U.S refineries. We’re here to remind investors that more upside potential remains in this winning Long Idea.

Below, we provide an excerpt from our latest Long Idea report to show how our research finds opportunities the market is missing. Get the full report a la carte here.

This stock presents quality Risk/Reward based on the company’s:

- position to profit from widening crack spreads,

- ability to serve long-term demand for refined fossil fuel products,

- high-quality balance sheet,

- strong shareholder return backed by consistent cash flow generation,

- high quality corporate governance, and

- cheap valuation that implies no growth in profits over remaining life of the company.

Crude Oil Production on the Rise

Domestic crude oil production continues to rise even after setting a new annual production record of 13.6 million barrels per day in 2025. The U.S. Energy Information Administration (EIA), in its May 2026 Short-Term Energy Outlook, projects U.S. crude oil production to grow 0.4% year-over-year (YoY) in 2026 and 3.3% YoY in 2027.

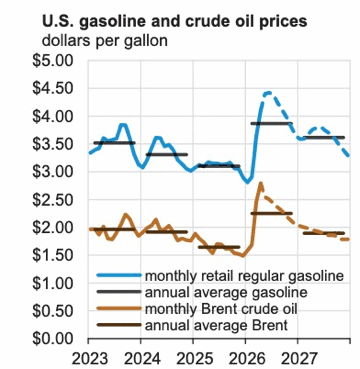

Constraints in Middle Eastern production and reduced global inventories have pushed Brent crude prices, and retail gasoline prices, materially above prior expectations. Now, the EIA projects prices will remain high compared to pre-conflict levels through at least 2027.

Higher crude and refined product prices support stronger crack spreads and profitability for refiners, particularly in periods where refined product pricing adjusts alongside tighter global supply.

Figure 1: U.S. Gasoline and crude oil prices: 2023-2027

Sources: EIA Short-Term Energy Outlook, May 2026

Rising Demand for Jet and Diesel Fuel

While gasoline demand may face long-term pressure, the International Energy Agency (IEA) projects jet fuel and diesel demand to grow through 2030. Additionally, the EIA projects diesel fuel and jet fuel prices to remain above pre-conflict levels through at least 2027.

U.S. refiners are producing jet fuel at near-record levels, recently surpassing 2 million barrels per day as companies increase capacity and shift refinery yields toward higher-margin aviation fuel. Several major refiners have announced projects aimed at expanding jet fuel output, which reflects strong industry economics and demand.

The Company completed a project at one of its major refineries at the end of 2025 that allows the facility to swing approximately 7k bbl/day between diesel and jet fuel production. This project provides flexibility to optimize product output based on market conditions.

While the IEA expects jet fuel demand to remain strong, it is more cyclical than diesel. Diesel powers essential sectors such as trucking (~72% of domestic freight is shipped via truck), agriculture, and construction, and cannot be easily replaced. As a result, the IEA, in addition to the Oxford Institute for Energy Studies, projects diesel demand to grow through 2030.

U.S. Refiners Capture More Margin

Refineries squeeze out far more value from a barrel of oil than crude oil producers. Refiners process crude oil into petroleum products and earn a “crack spread” between the price of crude oil and the price of the refined products they sell. Crack spreads are widening (see Figure 3 in the full report), and U.S. refiners are positioned to capture more of the upside than their global peers.

The Middle East primarily supplies Asian refineries, and it is the price of these crudes that has risen the most and lifted global averages. Dubai and Murban crudes, for example, trade at premiums to WTI and Brent.

By avoiding the more expensive Middle East crude, American refineries have access to cheaper, landlocked North American crude from producers more insulated from geopolitical shocks.

However, they sell refined products into markets where prices rise with global tightness, even if their feedstock costs do not, which increases margins.

Strong Fundamentals

Energy uncertainty and rising crack spreads drive strong profits for this company, even if down from record highs seen industry wide in 2022.

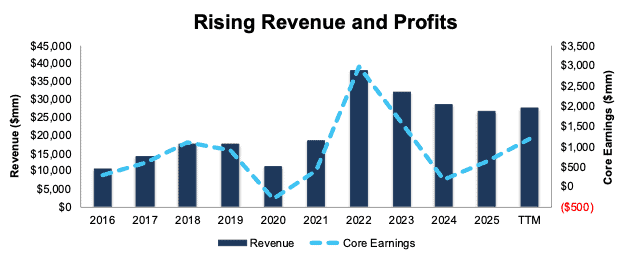

In the trailing-twelve-months (TTM) ended 1Q26, the company’s Core Earnings were $1.2 billion, which is higher than any annual period since 2016 excluding record highs of 2022 and 2023.

Longer-term, the company has grown revenue and Core Earnings by 11% and 16% compounded annually since 2016. See Figure 4. The company’s net operating profit after-tax (NOPAT) margin improved from 1% in 2016 to 4% in the TTM while invested capital turns improved from 1.2 to 1.8 over the same time. Rising NOPAT margins and invested capital turns drive the company’s return on invested capital (ROIC) from 2% in 2016 to 8% over the TTM.

Figure 4: Revenue and Core Earnings: 2016 – TTM ended 1Q26

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

Interested in starting your membership to get access to more of our research? Get more details here.