2 replies to "Wal-Mart: Still Offering Great Value"

Gill

June 6, 2013

Thank you for your analysis and recommendation, which has been a great call. I’ve struggled calculating economic book value, in particular: goodwill & real estate market value – thanks to FASB’s LCM approach. Can anyone recommend how I can learn to make the adjustments?

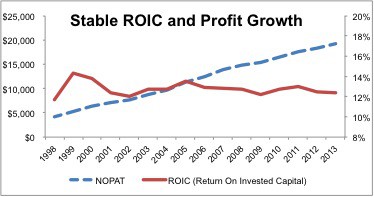

As far as WMT’s competitive risk, I believe most of it can be attributed to Costco, TGT, and the dollar stores – with DG, DLTR & FDO taking most of WMT’s domestic share losses. But as the ROIC of WMT’s smaller stores continues to rise, now matching that of it’s supercenters, it will allow management to continue expansion and regain lost share. And with the recent sell off in consumer staples WMT now trades at a TTM EV to EBITDA of only 8.10 and a price to cash flow of 9.3.

Gill:

Thanks for your comment.

Our formula for economic book value is at the link below.

Valuing goodwill is a rather low-utility task. The stock price is more about the cash flows that assets generate than the value of specific assets, ergo our economic book value formula focuses on NOPAT.

Valuing real estate is easier to calculate – just need to get the fair market values – but that info can be hard to obtain.

2 replies to "Wal-Mart: Still Offering Great Value"

Thank you for your analysis and recommendation, which has been a great call. I’ve struggled calculating economic book value, in particular: goodwill & real estate market value – thanks to FASB’s LCM approach. Can anyone recommend how I can learn to make the adjustments?

As far as WMT’s competitive risk, I believe most of it can be attributed to Costco, TGT, and the dollar stores – with DG, DLTR & FDO taking most of WMT’s domestic share losses. But as the ROIC of WMT’s smaller stores continues to rise, now matching that of it’s supercenters, it will allow management to continue expansion and regain lost share. And with the recent sell off in consumer staples WMT now trades at a TTM EV to EBITDA of only 8.10 and a price to cash flow of 9.3.

Gill:

Thanks for your comment.

Our formula for economic book value is at the link below.

Valuing goodwill is a rather low-utility task. The stock price is more about the cash flows that assets generate than the value of specific assets, ergo our economic book value formula focuses on NOPAT.

Valuing real estate is easier to calculate – just need to get the fair market values – but that info can be hard to obtain.

https://www.newconstructs.com/2012/06/18/price-to-economic-book-value-or-price-to-ebv/