This week’s Long Idea features an industry leader poised to profit from robust demand across the globe. As one of the largest producers in the U.S., this business is geographically diversified and the most profitable company amongst its peers.

However, the stock price implies profits will permanently decline by more than 50%. Despite the overhang of the poor reputation of the company’s majority owner, we see an opportunity to buy unduly low expectations.

Longer term, we see an even bigger expectations investing opportunity if the company achieves anything close to its historical growth rates.

Below, we provide an excerpt from our latest Long Idea report. You can buy the full report a la carte here.

We’re not giving you the ticker for this pick, but we are happy to share this preview so you can see how we operate.

This stock presents quality Risk/Reward based on the company’s:

- position to profit from rising protein demand and affordability,

- growing sales across all business segments,

- best in class profitability, strong free cash flow, and

- very cheap stock valuation.

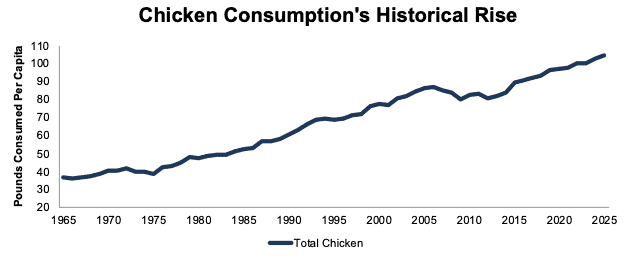

Chicken Demand Continues To Rise

Chicken has consistently gained popularity and is the most-consumed protein in the United States. In fact, U.S. chicken consumption per capita increased from 36 pounds in 1965 to 104.5 pounds in 2025. Per capita consumption is projected to rise to 104.9 pounds in 2026. See Figure 1.

Growth in chicken consumption has come largely at the expense of beef consumption, which, per capita, fell from 75 pounds in 1965 to 59 pounds in 2025.

Figure 1: Chicken Consumption per Capita in the U.S. From 1965 to 2025

Sources: The National Chicken Council

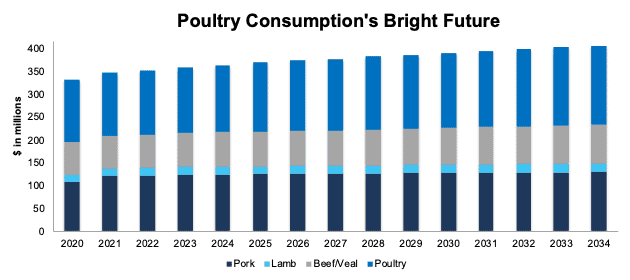

Demand Expected to Rise Too

The growth in chicken popularity is projected to continue.

Global protein consumption of pork, lamb, beef/veal, and poultry is projected to rise from 330 million tonnes in 2020 to 406 million tonnes in 2034, or 23%.

Chicken is the fastest growing protein of the group, with consumption projected to grow 28% from 2020-2034. See Figure 2.

Figure 2: Protein Consumption by Type: 2020-2034

Sources: OECD-FAO Agricultural Outlook 2025-2034

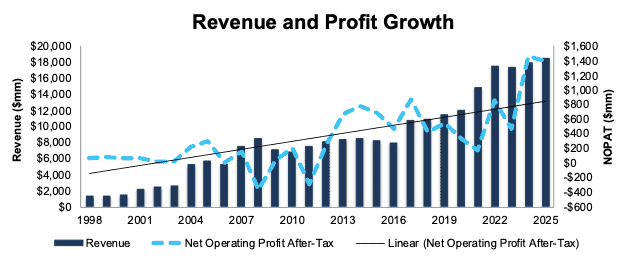

Quality Fundamentals Across Decades

This company has grown revenue and net operating profit after-tax (NOPAT) by 9% and 34% compounded annually, respectively, since 2020. The company’s NOPAT margin improved from 3% in 2020 to 8% in 2025, while invested capital turns increased from 1.8 to 2.3 over the same time. Rising NOPAT margins and IC turns drive the company’s return on invested capital (ROIC) from 5% in 2020 to 17% in 2025.

Longer-term, the company has grown revenue and NOPAT by 10% and 12% compounded annually since 1998, respectively. See Figure 5 from the full report.

Figure 5: Revenue and NOPAT Since 1998

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.