We’re bullish on businesses that generate profits whether an underlying commodity trades at $60 or $100. This week’s Long Idea is one such business, and the stock offers Very Attractive risk/reward.

The company gathers, processes, stores, and ships production under minimum-volume contracts running through 2033. This model drives consistent profit growth, and the business operates more profitably than its peers. However, the market prices this business as if its profits will collapse and never recover.

We see the opposite: a contractually-floored cash flow leader with a strong capital return program poised to profit for years to come.

Below, we provide an excerpt from our latest Long Idea report to show how our research finds opportunities the market is missing. Get the full report a la carte here.

This stock presents quality Risk/Reward based on the company’s:

- contractually protected cash flows,

- increasingly efficient operations,

- industry-leading returns on invested capital (ROIC),

- a potential 13% yield supported by easily adequate free cash flow,

- upside potential based on volumes, not prices, and

- cheap stock price that implies permanent profit decline

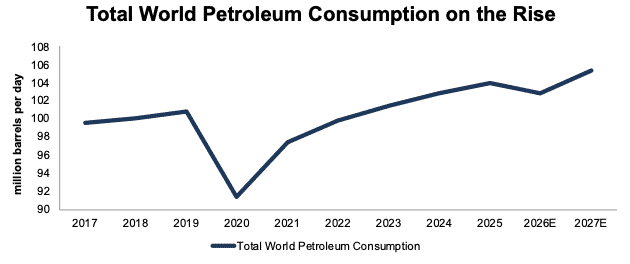

Fossil Fuel Consumption Still Rising

Even as operations in the Strait of Hormuz and the U.S. – Iran ceasefire remain uncertain, the world will consume and produce more crude oil and liquid fuels (such as gasoline) in the coming years.

The U.S. Energy Information Administration (EIA), in its June Short-Term Energy Outlook, projects global crude oil and liquid fuel consumption to grow by 2% year-over-year in 2027. Such consumption would also be 1% higher than 2025 consumption. See Figure 1.

Figure 1: Global Crude Oil and Liquid Fuels Consumption: 2017 – 2027

Sources: U.S Energy Information Administration

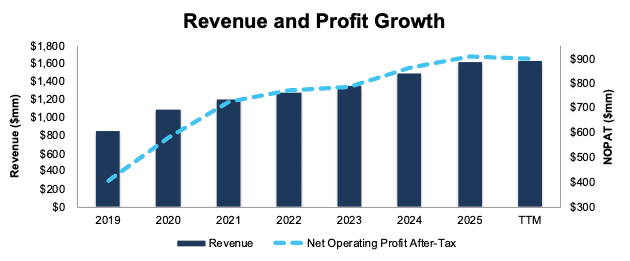

Steady Profit Growth

This company has grown revenue and net operating profit after-tax (NOPAT) by 11 and 14% compounded annually since 2019.

The company improved its NOPAT margin from 48% in 2019 to 55% over the TTM while invested capital (IC) turns, a measure of balance sheet efficiency, increased from 0.3 to 0.5 over the same time. Rising NOPAT margins and IC turns drive the company’s ROIC from 14% in 2019 to 26% in the TTM.

Figure 4: Revenue and NOPAT Since 2019

Sources: New Constructs, LLC and company filings

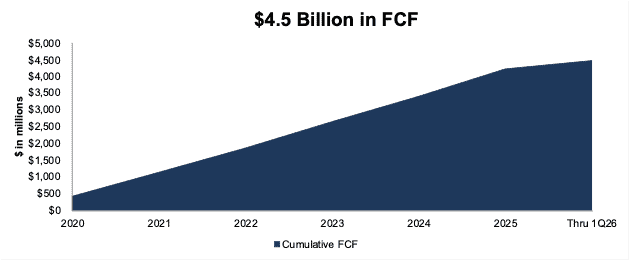

FCF Supports Distributions

From 2020 through 1Q26, this company generated $4.5 billion in FCF, which equals 53% of the company’s enterprise value. Over the TTM, the company generated $878 million in FCF. See Figure 7.

For reference, the company paid $3.5 billion in distributions from 2020-1Q26.

Figure 7: Cumulative FCF: 2020 – 1Q26

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

Interested in starting your membership to get access to more of our research? Get more details here.