Not Robo-Advisors, but Robo-Analysts will change the investing business the most in the coming years.

Some Background

In October of 1997, Charles Schwab (SCHW) CEO David Pottruck led 80 senior managers in a walk across the Golden Gate Bridge. Each manager wore gold trimmed jackets emblazoned with the words “Crossing the Chasm.” The walk symbolized Schwab’s transition from brick and mortar branches with human brokers to an online brokerage with self-directed trading. By cannibalizing parts of its own business, Schwab successfully made the transition into the digital age of investing and became one of the largest brokerages in the world.

Today, the wealth management industry finds itself on the brink of another chasm. In the same way online trading disrupted the distribution of investment advice, big-data analytics and machine learning will disrupt how financial advice and the research behind it is created.

The way firms respond to the new technologies transforming how research is performed and investment advice is applied will determine their future success or failure. Those that try to cling to existing business models will see their businesses decline. The winners will transform their businesses and embrace new technologies.

Winners and Losers Already Emerging

“Crossing the Chasm 2.0” began earlier this year when BlackRock (BLK), the largest asset manager in the world, announced the transition of $30 billion in assets from actively managed stock funds into funds that rely on algorithms and models. 53 stock pickers will step down with over 30 expected to leave the company.

Although this move affects only a small portion of BlackRock’s assets under management, it sends a strong signal for the future direction of the company. The era of the star fund manager is over, and computers are going to make more and more investing decisions.

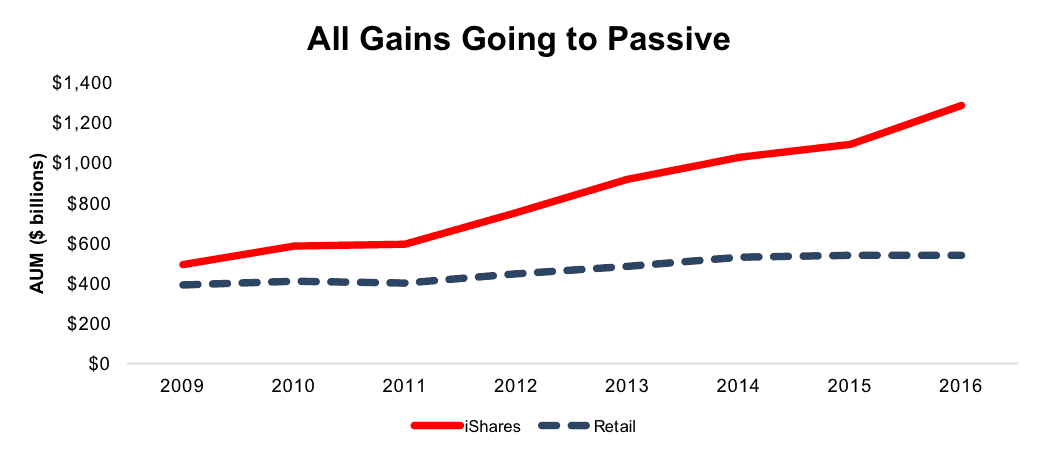

To understand BlackRock’s decision, see Figure 1 below. BlackRock’s iShares ETFs have grown assets under management (AUM) by 15% compounded annually since 2009. On the other hand, BlackRock’s retail division, which is 90% active, has grown AUM by just 5% compounded annually over the same timeframe.

Figure 1: Change in Assets Under Management: iShares vs. Retail

Sources: New Constructs, LLC and company filings.

At a closer look, the numbers get even worse for BlackRock’s active managers. In 2016, investors pulled a net $11 billion out of its retail funds. Only market-driven performance gains kept AUM stable. Overall, BlackRock’s active equity funds, both retail and institutional, saw over $20 billion in net outflows last year, while iShares equity funds had nearly $75 billion in net inflows.

Active Management Isn’t Dead, But It Needs To Change

BlackRock’s decision to acquire iShares in 2009 was wise and positioned the firm to benefit from the secular shift from active to passive. Still, neither BlackRock nor most of its peers can afford to let all their assets be siphoned into passive ETFs if they want to create value for their shareholders. The fees and margins in the passive business are far lower than for active management.

The current business model for active management revolves largely around highly-paid fund managers with discretionary authority over large sums of money. These active managers have, for the most part, significantly underperformed less expensive, passively-managed funds. This trend is a meaningful driver of the shift of assets from active to passive management.

There are still plenty of investors that want a higher level of personalization and diligence for their portfolio than passive investing can provide. However, these investors are likely to continue to refrain from investing in active management until they have faith that it can provide better price and performance.

Robo-Analyst Technology: The Only Way To Cut Costs and Improve Performance?

If the days of the highly-paid fund manager are behind us (with perhaps a few rare exceptions), then what will replace them? The answer is already manifest in the growth and success of systematic investing, a form of active management that is more science than art. Systematic investing replaces the intuition and subjectivity behind most traditional active management with analytical rigor and objectivity unmatchable by traditional active managers.

How do the systematic investors achieve so much more analytical rigor and objectivity? Meet the Robo-Analyst, a new form of technology focused on leveraging machines to analyze more data and test and produce active investment strategies that out-perform with lower costs.

The Right Response

Asset managers that have embraced Robo-Analyst technology are winning. For proof, look at the growth and performance of stand-alone quant firms like Two Sigma and Renaissance. The systematic managers at more traditional firms like Point72 and Millennium have meaningfully outperformed their old-school discretionary rivals in terms of returns and capital inflows. The secret of the success of these winners is embracing the automation and data analytics potential of machines to create cost-efficient, rigorous investing processes.

Replicating this success is not necessarily going to be easy for those looking to get into systematic investing. This new form of investing seems to require a different mentality and approach to investing than the old-school money managers. To succeed, more firms are going to have commit to BlackRock-like change. Either they cannibalize their old-school active manager and replace them with new talent to power systematic strategies or convince the old dogs to learn new tricks. Estimize founder Leigh Drogen compares this shift to Moneyball: just as baseball scouts pushed back against being replaced by algorithms, so too will fund managers. The few that thrive will be those that learn to harness the power of machines and combine it with human creativity.

BlackRock CEO Larry Fink clearly understands this dynamic, and has projected that the company’s technology platforms could generate 30% of its revenue in five years, up from 7% today. He clearly is a big believer in technology’s ability to radically improve the investing process.

The Wrong Response

Of course, for every BlackRock there are several companies that have not been as quick to embrace passive investing and clung to outdated active management for too long. The longer they wait, the more drastic the changes may have to be.

We saw a striking example earlier this month when AllianceBernstein’s parent, AXA Financial, announced a major shake-up aimed at shuttering the firm’s active management business.

Unlike BlackRock, AllianceBernstein never evolved its high-fee active management business, where under-performance led to significant investor outflows. The firm sought to stem the outflows by addressing the fee side of the equation and instituted a sliding fee scale based on fund performance. The strategy was, apparently, uninspiring. As a result, CEO Peter Kraus and nine of the company’s board members were removed on May 1.

According to the New York Times, AXA’s chairman, Denis Duverne “hinted the board of AB was not satisfied that Kraus was moving fast enough to confront the extraordinary growth of passive investing in recent years.

“In an industry that is confronting significant shifts, we need to continue transforming the business to improve the quality of our investment solutions while delivering our services more effectively,” Duverne said. (Source: The New York Times)

The marketplace is changing. Investors are not going to pay high fees for underperformance anymore. They demand low costs and a transparent, rigorous process with proven links to returns. Companies can either invest in the technology to fulfill that demand, or they can be left behind.

This article originally published on May 17, 2017.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Click here to download a PDF of this report.

Photo Credit: Tom Hilton (Flickr)