Navigating today’s retail landscape is challenging, with rising inflation, consumer uncertainty, and geopolitical crises impacting corporate growth. Yet, one unconventional footwear company continues to buck the trend.

With strong pricing power and an efficient manufacturing process, this brand has transformed a controversial design into a dominant, cash generating, market force.

We’re here to remind investors, this stock still looks cheap and holds strong upside potential.

Below, we provide an excerpt from our latest Long Idea report to show how our research finds opportunities the market is missing. Get the full report a la carte here.

This stock presents quality Risk/Reward based on the company’s:

- position to profit from rising footwear demand,

- steadily increasing sales across its core brand,

- turnaround opportunity with other brands,

- superior profitability vs. peers,

- strong cash generation that supports shareholder return, and

- cheap stock valuation.

Consumers Need Shoes

This company sits directly at the center of a global phenomenon and is positioned to profit from a growing total addressable market spread across three key global sectors. Specifically, the

- casual footwear market is forecast to grow ~4% compounded annually through 2034,

- clogs market is forecast to grow ~12% compounded annually through 2034, and

- sandals market is forecast to grow ~5% compounded annually through 2034.

Resilient Market Share Growth

This company has consistently grown its brand awareness and popularity across the globe. The company aims to expand in what management calls “Tier 1 Markets”, which include The United States, West Europe, India, China, Japan, and South Korea.

The company breaks down its 2025 market share into three distinct categories:

- Growing markets: less than 1% share in China, France, and Japan.

- Emerging markets: between 1% and 2% share in Germany and India.

- Established markets: greater than 2% share in the U.K., the U.S., and South Korea.

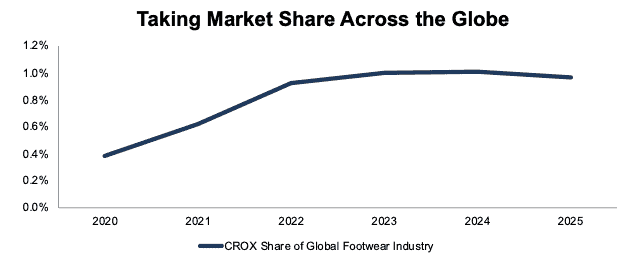

When we look at the entire global footwear market, the company’s ability to take market share (as measured by revenue as a % of overall industry sales) in a highly fragmented market shines. The company has grown its share of the global footwear industry from 0.4% in 2020 to 1.0% in 2025. See Figure 1 from the full report.

Figure 1: Global Market Share: 2020–2025

Sources: New Constructs, LLC and company filings

Cash Flows Support Capital Returns

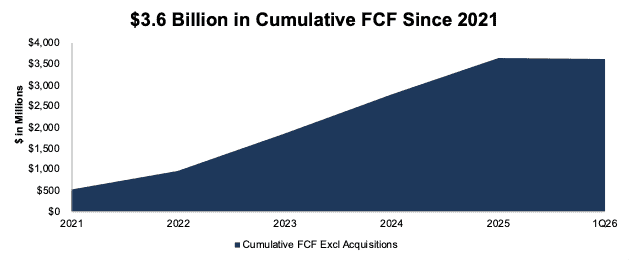

The company generated a cumulative $3.6 billion in free cash flow (FCF) excluding acquisitions (47% of its enterprise value) from 2021 through 1Q26. See Figure 6.

More recently, after a large acquisition in 2022, the company generated $2.7 billion in FCF from 2023-1Q26, or 15% more than the money the company spent on share repurchases.

Figure 6: Cumulative FCF Excluding Acquisitions Since 2021

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

Interested in starting your membership to get access to more of our research? Get more details here.