This week’s Danger Zone pick recently dropped 28% in one day after missing both top and bottom-line estimates.

We’re here to warn investors again though: don’t catch this falling knife. Despite opening more stores and improving “adjusted” non-GAAP metrics, we believe that the cash flow expectations baked into its (now much lower) stock price are still much too high.

Below, we provide an excerpt from our latest Danger Zone report to show how our research helps you see danger before it crushes your portfolio. Get the full report a la carte here.

This stock could fall further based on:

- misleading “adjusted EBITDA”,

- premium-priced products in an increasingly price-conscious environment,

- profitability well below key competitors,

- consistent cash burn that puts the company in the Zombie Stock crosshairs,

- ongoing shareholder dilution, and

- stock price that implies the company will grow profits nearly 7x TTM levels.

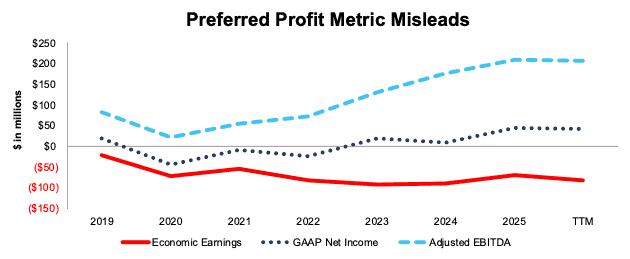

Adjusted Metrics Mislead Investors

This company presents many different versions of profitability, all of which mask the true economics of the business.

However, investors wouldn’t know that if they only analyzed the company’s preferred non-GAAP metric, Adjusted EBITDA. The company’s Adjusted EBITDA increased from $82 million in 2019 to $206 million over the TTM. Over the same time, GAAP net income increased from $20 million to $41 million, while economic earnings fell from -$21 million to -$80 million over the same time.

It’s a big red flag when a company’s preferred profitability metric is rising while economic earnings are declining.

Figure 2: GAAP Net Income vs. Economic Earnings vs. Adjusted EBITDA

Sources: New Constructs, LLC and company filings

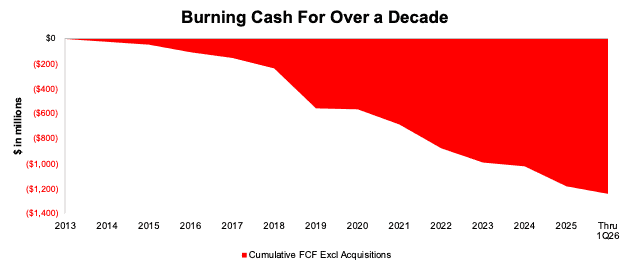

Cash Burn Problem Isn’t Solved

We took this company off our Zombie Stocks List in October 2024 list because the company’s free cash flow (FCF) burn slowed enough that it had more than 24 months of cash on hand before running out of cash. That is no longer the case.

The company burned $194 million in FCF over the TTM ended 1Q26. The company can only sustain such cash burn for 19 months based on its cash on hand as of April 1, 2026.

However, we’re not adding the company back to our Zombie Stocks list because it does not have a negative interest coverage ratio, which is the second criteria needed to quality as a Zombie Stock. Investors should be aware, though, that the company cannot maintain its cash burn forever, and should cash burn increase, a dilutive capital raise could be required.

Since 2013, the company has burned through $1.2 billion in cumulative FCF.

Figure 4: Cumulative Free Cash Flow Since 2013

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Danger Zone reports.

Interested in starting your membership to get access to more of our research? Get more details here.