As Benjamin Franklin once said, “nothing can be said to be certain, except death and taxes.” In modern times, insurance makes a perfect addendum to the now famous quote. Whether for prudent risk management or regulatory standards, buying insurance is increasingly a requirement of life, for individuals and businesses.

This week’s Long Idea is a titan of the U.S. property-and-casualty (P&C) insurance market. The company sets itself apart through superior underwriting. Its large direct sales channel alongside its legacy agency business drives consistent top-and bottom-line growth. However, the company’s stock is priced as if its profits will fall catastrophically and never recover.

Below, we provide an excerpt from our latest Long Idea report to show how our research finds opportunities the market is missing. Get the full report a la carte here.

This stock presents quality Risk/Reward based on the company’s:

- position in the U.S. auto insurance market,

- superior underwriting profitability, including a combined ratio well above industry averages,

- durable demand supported by a growing market with mandatory auto insurance requirements,

- strong free cash flow that supports shareholder return, and

- cheap stock price that implies a permanent 40% profit decline.

Insurance Market Growth Supported by Vehicle and Driver Trends

Several demand drivers support growth in the auto insurance market, including:

- a large and growing U.S. vehicle fleet,

- a deep base of licensed drivers,

- high reliance on personal vehicles, and

- legal requirements that make auto insurance effectively mandatory across most of the country.

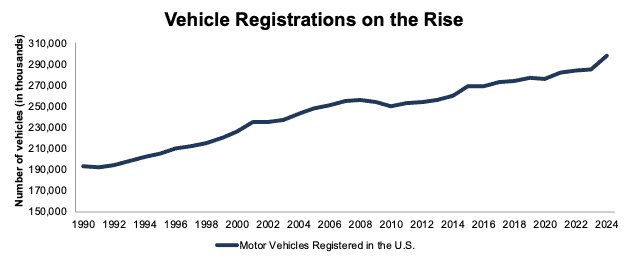

Per Statista, the number of motor vehicles registered in the United States increased from 193 million in 1990 to 298 million in 2024. See Figure 1. S&P Global estimates the U.S. vehicle fleet grew an additional 1% year-over-year (YoY) in 2025.

Figure 1: Number of motor vehicles registered in the United States: 1990 – 2024

Source: New Constructs, LLC and Statista

Data-Driven Underwriting Drives Superior Combined Ratio

Most insurance looks commoditized to consumers, especially when shoppers compare policies primarily on price. For insurers, however, the economics depend on risk selection, pricing accuracy, claims forecasting, expense discipline, and the ability to adjust quickly when loss trends change.

This company leverages telematics, such as driving habit measurement programs, to write data-driven policies, enhance risk segmentation, and maximize pricing (to balance growth vs. profitability) across both its agency and direct channels. Rather than simply chasing premium growth, the company focuses on writing policies that meet its return targets.

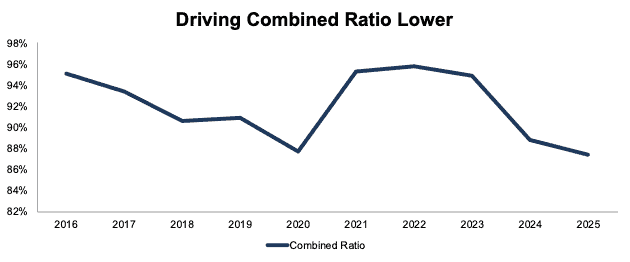

As a result, the company has consistently driven its combined ratio lower, outside of a post COVID spike. The combined ratio measures underwriting profitability by comparing claims and expenses relative to earned premiums. The lower a combined ratio, the more profitable the policies.

In 2025, the company generated a companywide combined ratio of 87.4%, which is down from 95.8% in 2022 and below the 87.7% combined ratio of 2020. For reference, the combined ratio across the entire U.S. property & casualty industry was roughly 96% in the first half of 2025 (latest data available).

In other words, this company is not just a large insurer benefiting from higher premiums. It is a quality underwriting franchise that uses customer data to operate more efficiently and drive superior profitability.

Figure 2: Combined Ratio: 2016 to 2025

Sources: New Constructs, LLC and company filings

Profitable Across All Cycles

This company operates in a cyclical industry, but its long-term profitability record reflects the strength of its underwriting model. Auto insurers can face sharp swings in claims costs, repair inflation, catastrophe losses, and pricing cycles, but this company has remained profitable across a wide range of market conditions.

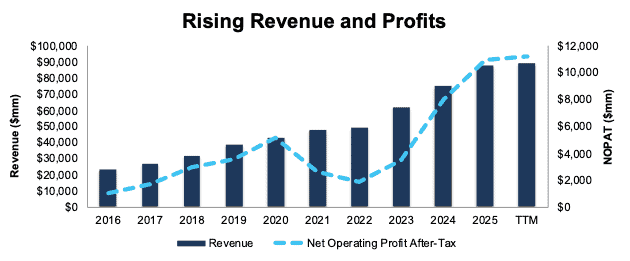

The company has generated positive net operating profit after-tax (NOPAT) every year since 2016. In fact, the company has generated positive NOPAT in all but one year (2008) going back to 1998.

Since 2016, the company has grown revenue and NOPAT by 16% and 29% compounded annually, respectively.

The company improved its NOPAT margin from 4.4% in 2016 to 12.5% over the TTM while invested capital turns remained at or above 3.0 over the same time. Rising NOPAT margin and consistent IC turns drive the company’s return on invested capital (ROIC) from 14% in 2016 to 38% over the TTM.

In other words, the company’s profitability isn’t only through balance sheet efficiency or a temporary spike in industry pricing. The company has paired consistently high capital turns with improving margins, which drive consistently higher ROIC, even during tougher underwriting years.

Figure 5: Revenue and NOPAT: 2016 – TTM ended 1Q26

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

Interested in starting your membership to get access to more of our research? Get more details here.