This company operates competitively advantaged refineries across the U.S. It processes cheap North American crude while selling products priced at more expensive global benchmarks. Despite peer-leading profitability and long run tailwinds, the stock is priced as if profits will permanently fall and offers Very Attractive risk/reward.

Below, we provide an excerpt from our latest Long Idea report. Get the full report a la carte here.

This stock presents quality Risk/Reward based on the company’s:

- monopoly position in a key region,

- feedstock cost advantage from discounted WCS and Bakken crude,

- integrated retail and logistics segments that provide a profit floor,

- record throughput and improving operational reliability across its refineries,

- peer-leading profitability, and

- cheap valuation that implies a permanent 40% drop in NOPAT that ignores long-term tailwinds.

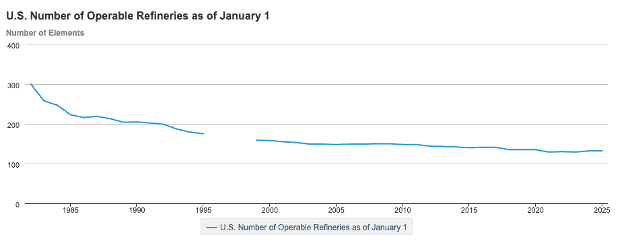

U.S. Refining Capacity Is Shrinking

The number of operable refineries in the United States has decreased from 301 in 1982 to 132 in 2025.

Since 2020, the U.S. has lost three refineries, which results in a loss of refining capacity of over 550,000 barrels a day (b/d). The last greenfield refinery in the United States came online in 1977.

Figure 1: Operable U.S. Refineries: 1982 – 2025

*EIA does not report the number of operable refineries in 1996 and 1998, which creates the gap in Figure 1.

Sources: U.S. Energy Information Administration (EIA)

Supply Disruptions = Higher Margins

The EIA noted in March 2025 that, by the end of 2026, U.S. fuel inventories would recede to their lowest levels since 2000. For refiners, tighter supply means greater margins. Specifically:

“Inventory withdrawals tend to increase wholesale and retail fuel prices because market participants must meet demand by competing for a smaller pool of refinery production. As a result, we also forecast wholesale refinery margins for the three fuels will increase.”

Flash-forward to 2026, and in its April 2026 Short-Term Energy Outlook, the EIA estimates that distillate inventories will remain below the 2021-2025 average throughout 2026 as a result of long run tightness from U.S. and European refinery closures.

The impact is seen across the entire Energy industry.

Petroleum products are in particularly dire straits, with refining margins surging as middle distillate cracks hit all-time highs. The International Energy Agency’s (IEA) executive director Fatih Birol identified jet fuel and diesel as “the main challenges,” noting shortages had already emerged in Asia and would spread.

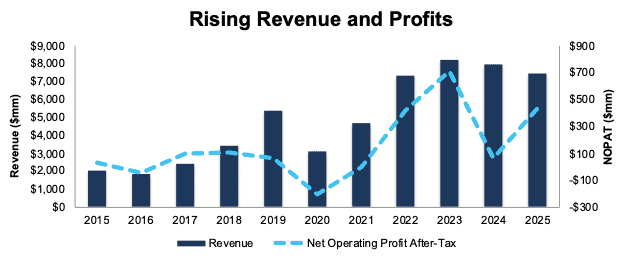

Long-Term Profit Growth

This company has grown revenue by 19% compounded annually since 2020. Meanwhile, the company improved its net operating profit after-tax (NOPAT) from -$205 million in 2020 to $432 million in 2025.

The company improved its NOPAT margin from -7% in 2020 to 6% in 2025, while its invested capital turns, a measure of balance sheet efficiency, improved from 1.4 to 2.3 over the same time. Improving NOPAT margins and IC turns drive the company’s return on invested capital (ROIC) from -9% in 2020 to 13% in 2025.

Longer-term, the company has grown revenue and NOPAT by 14% and 30% compounded annually since 2015. See Figure 4 from the full report. Over the same time, the company’s ROIC improved from 5% to 13%.

Figure 4: Revenue and NOPAT: 2015 – 2025

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

Interested in starting your membership to get access to more of our research? Get more details here.