This week’s Long Idea features a business poised to profit from robust demand as geopolitical shocks, export restrictions, and structural underinvestment tighten global supply for a product with inelastic demand.

Cost advantages, combined with centrally located assets, drive industry-leading returns on invested capital (ROIC). Despite these advantages, the stock price implies a permanent decline in profits.

Below, we provide an excerpt from our latest Long Idea report. You can buy the full report a la carte here.

We’re not giving you the ticker for this pick, but we are happy to share this preview so you can see how we operate.

This stock presents quality Risk/Reward based on the company’s:

- position to profit from inelastic demand,

- lower feedstock costs that drive industry-leading profitability,

- strong free cash flow to support high capital return potential,

- growth potential through dual feedstock flexibility and blue ammonia, and

- cheap stock valuation that implies a permanent profit decline.

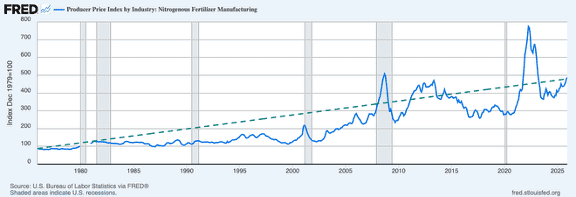

An Age of Shocks Supports High Prices

The Nitrogenous Fertilizer Producer Price Index rose 67% from December 2020 to December 2025.

Although prices have declined sharply since the April 2022 peak, they remain well above pre-2020 levels. Given ongoing supply-side shocks, prices are likely to remain elevated going forward.

Figure 1: Producer Price Index for the Nitrogenous Fertilizer Industry

Source: FRED

Since 2020, this industry has undergone multiple supply-side shocks, including:

- the COVID-19 pandemic,

- Russia’s invasion of Ukraine, which disrupted nitrogen, phosphate, and potash supplies, restricted natural gas to Europe, and ultimately increased both feedstock and product prices,

- sanctions on Belarus,

- fertilizer export quotas imposed by China and Russia, and

- the ongoing global trade war.

Global Supply Chains Remain Fragile

The world cannot simply trade its way out of the current situation.

According to the United States Geological Survey (USGS), net imports of nitrogen accounted for 6-13% of the United States’ nitrogen consumption by volume since 2020.

Brazil, one of the top three agricultural exporters of soybeans, corn, and sugar, imports over 80% of its fertilizer and has experienced significant disruptions in recent years. Its National Fertilizer Plan, which aims to reduce dependency on imported fertilizer from 85% to 50% by 2050, is expected to take decades to alleviate import dependency.

Russia increasingly diverts exports toward friendly nations. China imposed a rigorous export quota system designed to prioritize domestic food security over export revenue. This system restricts cargoes whenever domestic prices breach affordability thresholds. Most recently, the system resulted in a suspension of exports to India, leading to a jump in fertilizer prices in the region.

The top five agricultural producers, China, India, the U.S., Russia, and Brazil, account for half of the world’s nitrogen fertilizer consumption, and the push toward economic independence among major powers means that global capacity is not the same as available supply.

Strong Profit and Revenue Growth

This company has grown revenue and net operating profit after-tax (NOPAT) by 12% and 79% compounded annually, respectively, since 2020. The company’s NOPAT margin has improved from 2% in 2020 to 22% in 2025, while invested capital turns, a measure of balance sheet efficiency, improved from 0.3 to 0.7 over the same time. The combination of rising NOPAT margins and invested capital turns drives the company’s ROIC from 1% in 2020 to 15% in 2025.

Longer-term, the company has grown revenue and NOPAT by 8% and 6% compounded annually, respectively, from 2015-2025.

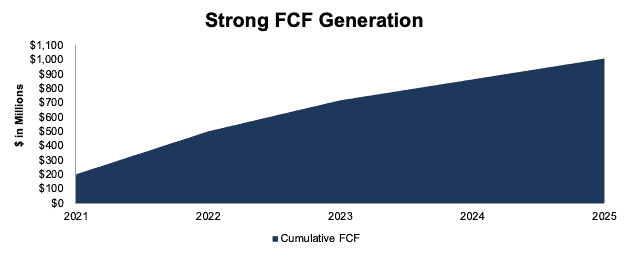

Strong Distribution Yield Supported by Strong Free Cash Flow

The company’s distributions vary quarterly depending largely on operating performance. For the full year 2025, the company’s equaled a nearly 12% TTM yield.

Between 2021 and 2025, the company paid $733 million in distributions and generated $1 billion in free cash flow (FCF).

The company generated $141 million in FCF in 2025.

Figure 7: Cumulative Free Cash Flow Since 2021

Sources: New Constructs, LLC and company filings

…there’s much more in the full report. You can buy the report a la carte here.

Or, become a Professional or Institutional member – they get all Long Idea reports.

I’ll keep sending information on quality sectors, industries, or specific companies until you’re ready to start your membership.

Interested in starting your membership to get access to all our Long Ideas? Get more details here.