Recap from December’s Picks

Our Most Dangerous Stocks (+0.0%) remained flat, while the S&P 500 (-2.2%) declined last month and underperformed as a short portfolio.

Most Dangerous Small Cap and Danger Zone stock, Oxford Industries (OXM), fell by 19% and Most Dangerous Large Cap stock, Polypore International (PPO) fell 11%. 16 out of the 40 Most Dangerous stocks outperformed as shorts and 22 had negative returns.

On to January’s Picks

Our Most Dangerous stocks for January were made available on January 7. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

Most Dangerous Stock Feature for January: Flagstar Bancorp (FBC)

Flagstar Bancorp (FBC) is one of the new Most Dangerous stocks for January. Flagstar was placed in the Danger Zone in May 2014, and its situation has not improved. Poor historical fundamentals, coupled with disappointing quarterly results have made this stock even more dangerous than before.

Flagstar’s return on invested capital (ROIC) has been negative four of the past five years, and was -8% in 2013. In 2013, Flagstar’s after-tax operating profit (NOPAT) was -$187 million, down from $53 million the year before.

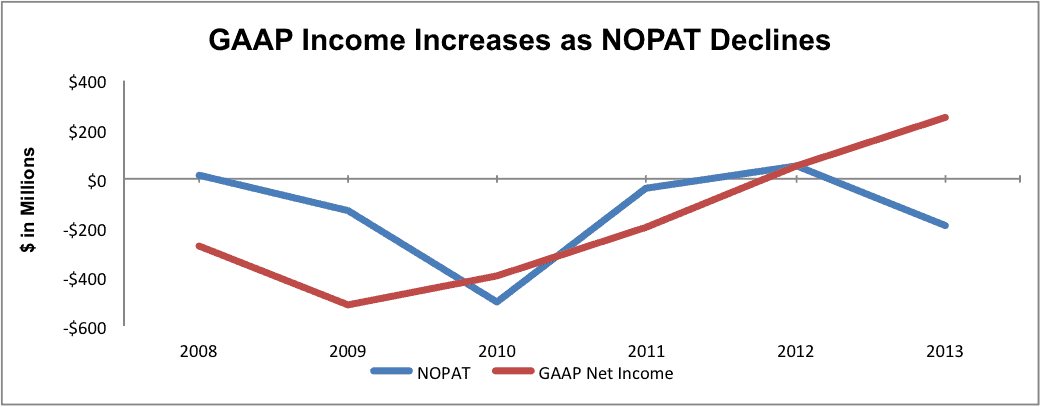

One red flag that sticks out in the company’s 2013 10-K is the drastic difference between our NOPAT calculation and Flagstar’s GAAP net income. Figure 1 highlights the difference, after many years of closely following one another. The main reasons for this large difference were a $98 million decrease in reserves added into pre-tax income and a $49 million gain on a legal settlement. These two items allowed Flagstar to artificially increase its GAAP net income, leaving investors with artificially inflated net income.

Figure 1: NOPAT and GAAP “Income”

Source: New Constructs, LLC and company filings

After the first quarter of 2014, Flagstar increased its loan loss reserves by $100 million, thereby wiping out the decrease from a quarter earlier. One has to wonder if Flagstar’s management will resort to the same accounting tricks and earnings manipulation to give the appearance of profitability when the company’s 2014 10-K is released.

Unfortunately, the rest of 2014 was not any better for the company. At the end of 3Q14, Flagstar reported that its income through 3Q14 had declined 25% year over year, and operating income was down nearly 50%.

Why Flagstar’s Valuation is Unwarranted

After taking the above into account, Flagstar is still overvalued even after a 25% decline in stock price from its highs in 2014. Flagstar remains awfully overvalued. To justify its current price of ~$16/share, Flagstar must achieve pre-tax margins of 8% (up from -31% in 2013) and grow revenues by 15% for the next 12 years. As highlighted by the company’s third quarter results, revenue growth is still in issue in 2014, and looks to be the same in 2015. It’s easy to see why Flagstar made our Most Dangerous list. The expectations embedded into the stock price are dangerously high, and the company’s accounting tricks suggest that it puts short-term earnings before long-term growth and value creation.

Kyle Guske II contributed to this report.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector, or theme.