Our Most Attractive and Most Dangerous stocks for September were made available to the public last night. Last month saw some strong performances from our picks. Volterra Semiconductor Corp (VLTR) led the way for the Most Attractive stocks, up 52% on news of its impending acquisition by Maxim Integrated Products (MXIM). 32 out of the 40 Most Dangerous stocks declined last month, paced by Tredegar Corporation (TG), which dropped over 20%. Cabela’s (CAB) had the largest drop of our Most Dangerous large caps, declining over 8%.

September sees 16 new stocks make our Most Attractive list and 14 new stocks fall into the Most Dangerous category. Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

DirecTV (DTV) is one of the new additions to the Most Attractive list this month. DTV’s ranking increased due to the 5% decline in its price last month, which made it cheap enough to qualify for the list.

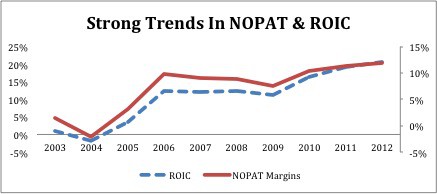

DTV scores very well in the criteria that drive our stock ratings. It has a top quintile ROIC of 21%, and it has increased ROIC in each of the pas three years. DTV’s strong ROIC has been driven largely by its ability to grow its margins. Figure 1 shows the correlation between DTV’s expanding margins and its ROIC.

Figure 1: DirectTV (DTV): Expanding Margins Drive ROIC

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Part of DTV’s success comes from its superior customer service. As this survey from the American Customer Satisfaction Index shows, DTV ranks second among all subscription TV providers, well ahead of its largest competitors like Comcast (CMCSA), Time Warner (TWX), and Dish Network (DISH). DTV’s higher quality service allows it to charge a premium price and retain more customers.

While the increase of streaming content puts pressure on DTV’s US business, it still has significant potential for growth in Latin America. DirecTV Latin America currently has over 10 million subscribers, and affiliate Sky Mexico adds another 5 million. Given the relatively low percentage of homes with pay TV services in Latin America and the region’s high projected economic growth, DirecTV Latin America should increase its subscriber base significantly over the next few years.

At ~$59/share, DTV represents a solid value buy. It currently has a price to economic book value ratio of 0.8, meaning that the market expects its profit (NOPAT) to permanently decline by 20%. Strong fundamentals and a cheap valuation land DTV on the Most Attractive list despite the competitive pressures it faces.

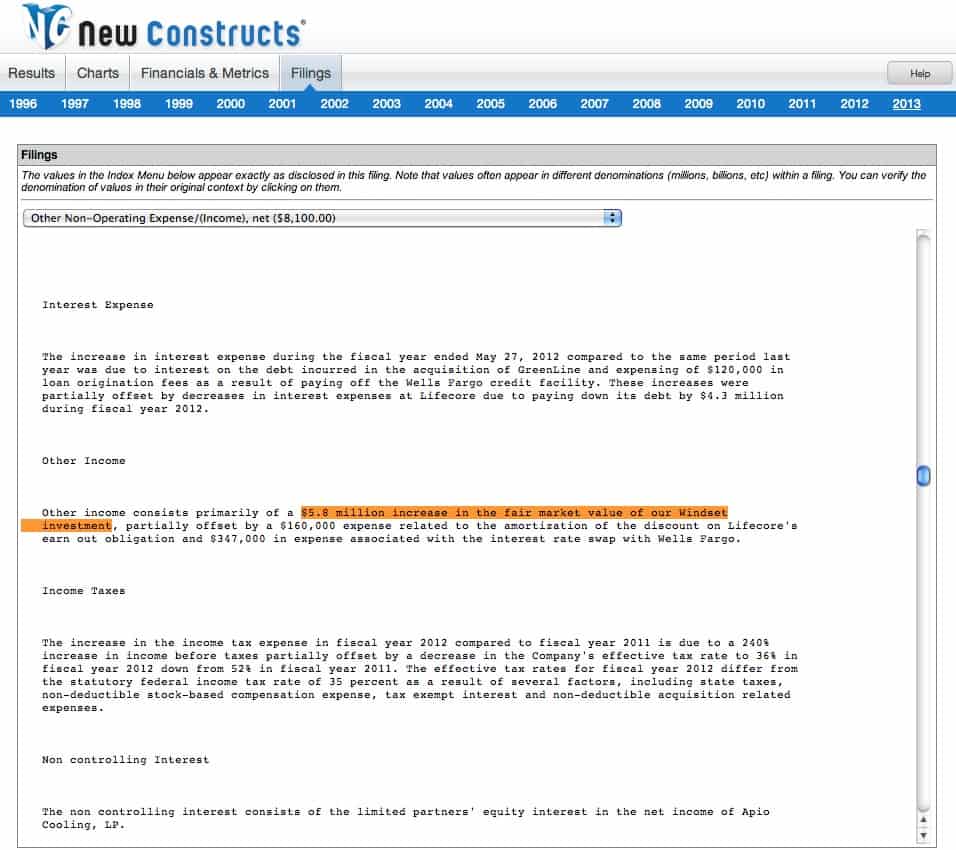

On the other side of the coin, Landec Corporation (LNDC) made its way onto the Most Dangerous stocks list for September. LNDC released its 2013 Form 10-K in August, and our research found some non-operating items that make LNDC appear more profitable than it really is.

LNDC had $8.1 million classified as “other income”, which mostly came from a $5.8 million increase in the value of its investment in another company, Windset. All of this income is non-operating income, as it derives from sources that LNDC cannot control or sustain.

{kind=link}

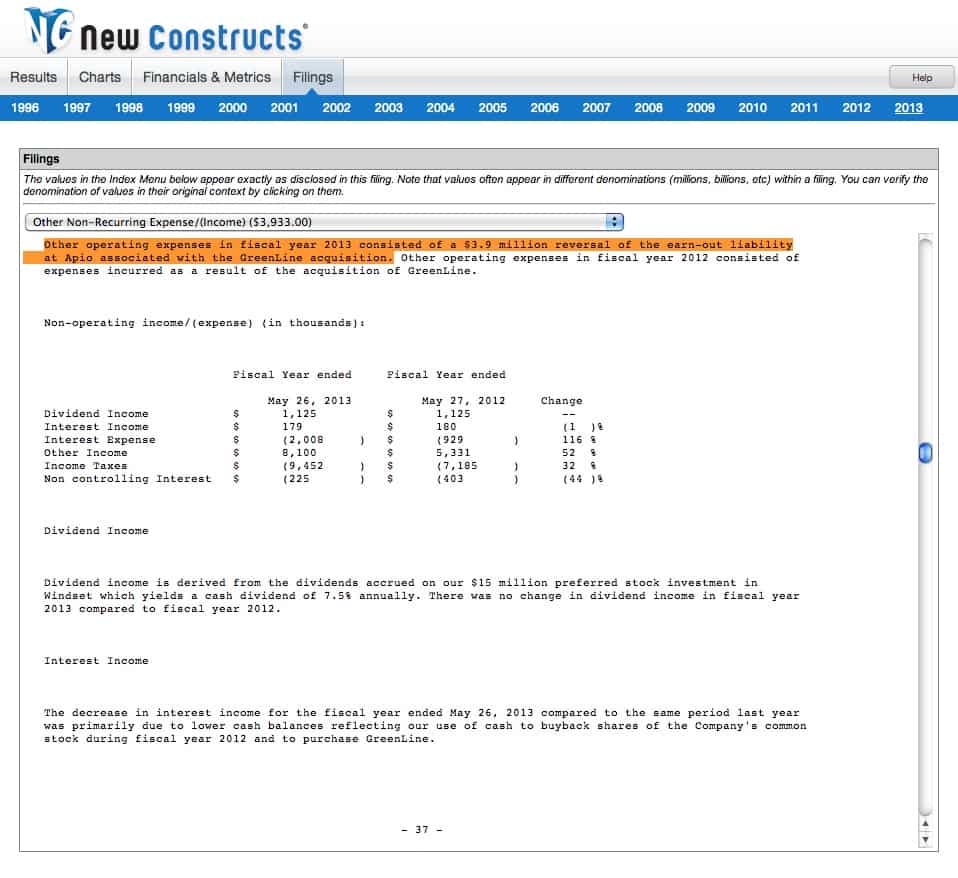

In addition, LNDC had a further $3.9 million in income bundled in “other operating expenses” due to the reversal of a contingent consideration liability. This liability reflected a potential payment LNDC would have been obligated to make if recent acquisition GreenLine Foods had met a certain earnings target. That target was not reached, so LNDC can remove that $3.9 million liability and record it as income despite not actually earning any cash.

{kind=link}

In total, LNDC earned roughly $11 million in pre-tax non-operating income last year. As a result, LNDC’s earnings show a misleading trend. Its accounting earnings increased by nearly 75%, but its ROIC actually declined by one tenth of a percentage point.

LNDC’s long-term history does not paint a positive picture of the overall quality of the business. In the past 18 years, LNDC has earned positive economic earnings just once in 2008. Investors should look for companies that do a better job of adding value for investors especially given LNDC’s expensive valuation.

To justify its current price of ~$13/share, LNDC would need to grow NOPAT by 15% compounded annually for 17 years. With so much growth embedded in its valuation, LNDC has priced out most of the reward for investors while leaving significant downside risk.

The Most Dangerous Stocks report for September can be purchased here, while the Most Attractive Stocks can be purchased here. To gain access to these reports one week earlier each month, e-mail us at subscriptions@newconstructs.com to request a subscription.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.