CEO David Trainer recently joined BBC News to discuss why Palantir (PLTR: $136/share) dropped despite beating on both the top and bottom lines in its 1Q26 earnings report.

The answer is quite simple: expectations.

When we use our reverse discounted cash flow (DCF) model to quantify the expectations baked into PLTR, we see that it is the poster child of “priced for perfection.”

Despite the strong earnings report, the expectations for future profit growth implied by the stock’s valuation are even stronger. As a result, downside risk dwarfs upside potential because all the good news is already priced into the stock.

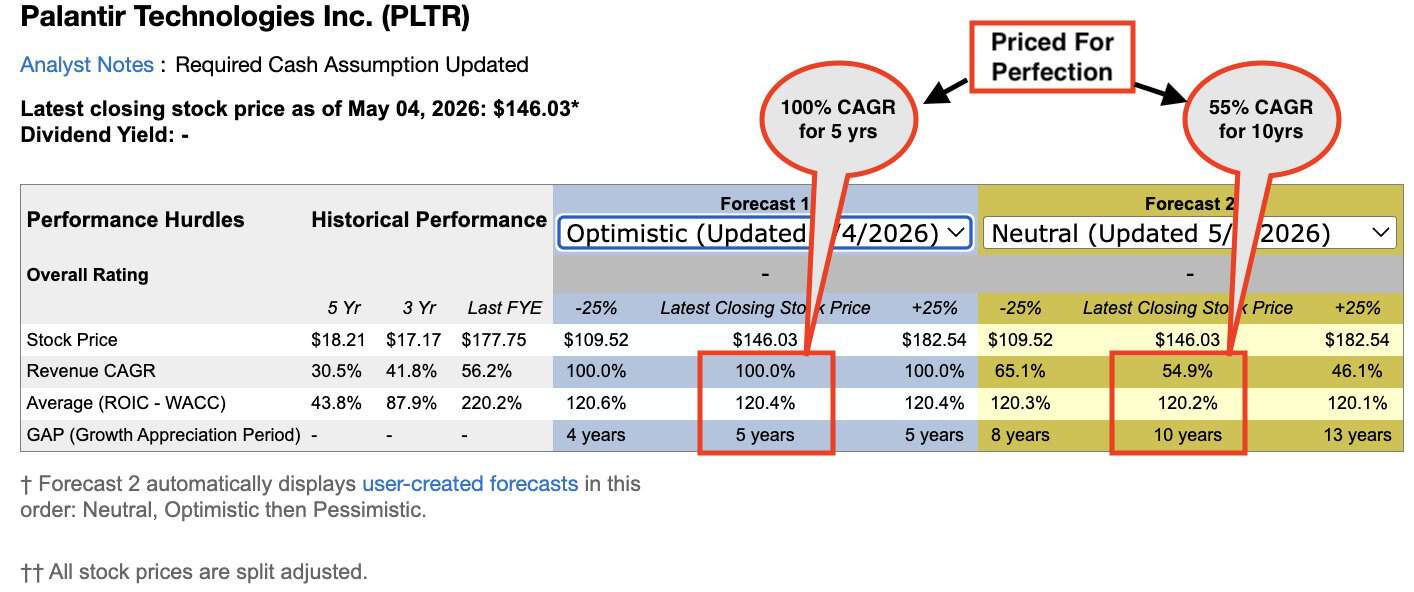

For example, in order to justify a price of $146/share, PLTR’s price prior to earnings, the company must either:

- grow revenue 100% compounded annually for five years, OR

- grow revenue 55% compounded annually for 10 years.

In both scenarios, the company must also maintain current margins despite accelerating competition. Such lofty expectations mean that even beating on the top and bottom lines is not enough to send shares higher.

Figure 1 highlights the decision page of our reverse DCF model, which shows how much Palantir must grow its revenue and economic earnings margin (ROIC – WACC) in each of these scenarios.

Figure 1: Reverse DCF Shows Palantir is Priced for Perfection

Sources: New Constructs, LLC and company filings

Expectations matter, especially when analyzing the risk/reward of a high-flying stock such as Palantir.

At New Constructs, we leverage superior fundamental data with best-in-class valuation models to provide ratings on 10,000+ stocks, ETFs, and mutual funds. Learn more here.

This article was originally published on May 5, 2026.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.