This report shows how well Financials ETFs and mutual fund managers pick stocks. We juxtapose our Portfolio Management rating on funds, which grades managers based on the quality of the stocks they choose, with the number of good stocks available in the sector. This analysis shows whether or not ETF providers and mutual fund managers deserve their fees.

For example, if a fund has a poor Portfolio Management rating in a sector where there are lots of good stocks, that fund does not deserve the fees it charges, and investors are much better off putting money in a passively-managed fund or investing directly in the sector’s good stocks. On the other hand, if a fund has a good Portfolio Management rating in a sector where there are lots of bad stocks, then investors should put money in that fund assuming the fund’s costs are competitive.

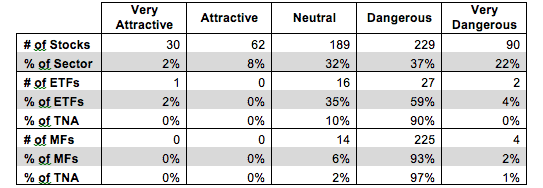

Figure 1 shows how many good stocks, according to our nationally-recognized ratings, are in the sector and their market cap. Next, it juxtaposes the Portfolio Management ratings of the ETFs and mutual funds in the sector. We think investors can gain an advantage with our forward-looking fund ratings since past performance is not a reliable predictor of future returns.

Figure 1 shows that 92 out of the 600 stocks (only 10% of the market value) in Financials ETFs and mutual funds get an Attractive-or-better rating.

The main takeaway from Figure 1 is only 2% (1 out of 46) of ETFs allocate enough to quality stocks to earn an Attractive-or-better Portfolio Management rating. Mutual Fund managers have done even worse with 0% (0 out of 243) of mutual funds allocating enough of their assets to quality stocks to earn an Attractive-or better rating. ETF providers and mutual fund managers need to do a better job to justify their fees.

With no quality ETFs it should come as no surprise that investors are putting their money into low quality ETFs and mutual funds. However, even more troubling is that only 10% of total net assets are located in the ETFs with a Neutral Portfolio Management rating. Investors are allocating to the worst ETFs in the sector. The picture is worse for mutual fund investors as only 2% of investor assets are allocated to Neutral-rated funds. The rest sits in funds that earn a Dangerous-or-worse Portfolio Management rating.

It is unfortunate to see such a large percentage of total net assets allocated to Dangerous-or-worse rated funds

Figure 1: Financials Sector: Comparing Quality of Stock Picking To Quality Of Stocks Available

Sources: New Constructs, LLC and company filings

PowerShares KBW Property & Casualty Insurance Portfolio ETF (KBWP) has the highest Portfolio Management rating of all Financials ETFs and earns my Very Attractive rating. KBWP stands out in a sector with many poorly rated ETFs. Fidelity Select Portfolios: Consumer Finance Portfolio (FSVLX) has the highest Portfolio Management rating of all Financials mutual funds and earns my Neutral rating.

iShares FTSE NAREIT Industrial/Office Capped Index Fund ETF (FNIO) has the lowest Portfolio Management rating of all Financials ETFs and earns my Very Dangerous rating. World Funds Trust: REMS Real Estate Value-Opportunity Fund (HLPPX) has the lowest Portfolio Management rating of all Financials mutual funds and earns my Very Dangerous rating.

Allstate Corporation (ALL) is one of my favorite stocks held by Financials ETFs and mutual funds and earns my Very Attractive rating. Allstate also lands on the Most Attractive stocks list for October. Allstate has grown after-tax profits (NOPAT) by 32% compounded annually over the last four years. Over the same time period, Allstate increased its return on invested capital (ROIC) to 14% in 2013 from 6% in 2009. Allstate has continued these positive trends into 2014 by growing revenues in 2Q14 by 5% year over year (YoY) and operating income by 55% YoY. At its current price of ~$62/share, Allstate has a price to economic book value (PEBV) of 0.8. This ratio implies the market expects Allstate’s NOPAT to permanently decline by 20% from its current level. This expectation seems extremely unlikely given Allstate’s impressive track record of NOPAT growth over the past four years. We think your money is in good hands with ALL.

Northfield Bancorp, Inc. (NFBK) is one of my least favorite stocks held by Financials ETFs and mutual funds and earns my Very Dangerous rating. NFBK is also on the Most Dangerous stocks list for October. Over the past five years, NFBK has failed to grow NOPAT. The company’s ROIC has fallen to 3%, which ranks in the bottom quintile of all companies I cover. Despite not growing NOPAT, NFBK has increased invested capital by 13% compounded annually over the last five years. Not growing profits while rather aggressively expanding one’s balance sheet translates into serious cash flow hemorrhaging and shareholder value destruction. Worse yet, the stock remains highly valued. To justify its current price of ~$14/share, NFBK would have to grow NOPAT by 13% for the next 21 years. Given this company’s recent history of negative cash flow, the expectations in the current stock price seem unrealistic.

Many ETFs and mutual funds managers do a poor job identifying quality stocks. They allocate heavily to overvalued stocks like NFBK and don’t hold high quality stocks such as ALL. These funds are not worth owning at any cost.

The emphasis that traditional research places on low costs is a positive for investors, but low fees alone do not drive performance. Only good holdings can. Don’t fall prey to the index label myths. Even “passive” investors should be analyzing the holdings of their funds.

Our Best & Worst ETFs and Mutual Funds for the Financials Sector report reveals our predictive ratings on the best and worst funds in the sector.

Kyle Guske II contributed to this report.

Disclosure: David Trainer owns ALL. David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector, or theme.

Click here to download a PDF of this report.