TWTR is up 17% since June 10 when Microsoft (MSFT) announced intent to buy LinkedIn (LNKD) for about $20 billion, $153/share more than it was worth. The media has named Alphabet (GOOGL) as a likely candidate to overpay for Twitter as MSFT did for LNKD. But, we think management at Alphabet is a better steward of shareholder value. The bottom line is that there is a limit for how much Alphabet should pay for TWTR (as there are limits for the price of any asset) in order for the deal to be economically profitable. Even in the most optimistic scenario for TWTR’s future cash flows, Alphabet should pay no more than $1.1 billion, or $1.55/share, for Twitter, which is 91% below the current price.

Twitter Remains Unprofitable

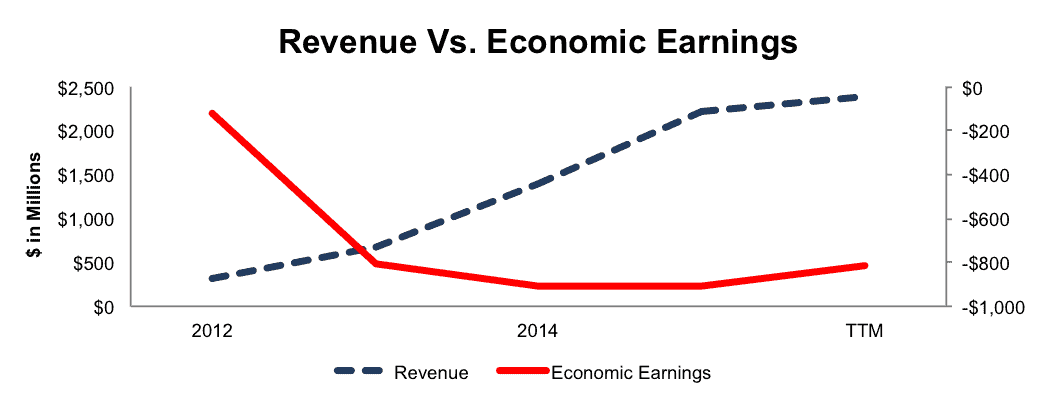

When we first analyzed Twitter in June 2015, we noted that the company has been great at growing revenue while increasing cash losses. Since then, losses have slightly improved, but remain large (-38% of revenue). Figure 1 shows that while revenue has grown from $317 million in 2012, to $2.4 billion over the last twelve months, economic earnings have declined from -$122 million to -$816 million over the same time.

Figure 1: Twitter’s Negative Economic Earnings

Sources: New Constructs, LLC and company filings

How Could Twitter Create Value For Alphabet?

For those that care about intelligent capital allocation, acquisitions must create synergy (i.e. profits that could not otherwise be achieved by the two standalone companies). The profits of the acquired company, including synergies, must be high enough to earn a return on invested capital (ROIC) higher than the acquiring company’s weighted-average cost of capital (WACC). If those conditions are not met, the deal should not be done – assuming one cares about intelligent capital allocation.

When it comes to creating value for Alphabet, Twitter is starting from a tough spot with negative $812 million in economic earnings over the last twelve months. The combination with Alphabet would have to, rather drastically, improve the core profitability of the business and more.

We do not think any of the speculated reasons for Alphabet to acquire Twitter will improve profits at Twitter enough to justify a purchase price of more than $1.55/share, assuming Alphabet cares about capital allocation and creating shareholder value.

We doubt Twitter could improve Google Plus or Alphabet’s social media business that much. Alphabet already has access to most, if not all, of Twitter’s data since it integrated Twitter Ads into Google’s Ad server, DoubleClick, in 2015.

The main challenge for Alphabet’s management to overcome in justifying any price for TWTR is Twitter’s flawed business model, which we address in our Danger Zone report. The flaw is that the best interests of the users (i.e. quick, easy access to the content of their choosing) are not aligned with the best interests of advertisers (i.e. getting more attention of users not necessarily looking for them). Until this fundamental flaw is addressed (and we are not sure it can be), it is hard to make a straight-faced argument for anyone to buy Twitter.

Acquisition At Current Price Would Be Poor Use of Capital

Alphabet has a long history of acquiring firms, such as YouTube or more recently Nest, and integrating them into the larger corporation successfully. Alphabet’s high ROIC (26%) reflects management’s intelligent approach to capital allocation, and we see no reason for that to change especially after the re-alignment of the company last summer.

Fortunately, the math behind determining an appropriate acquisition price is simple.

If Alphabet were to acquire Twitter at its current price of $16/share, it would be spending $13.9 billion total ($11.4 billion equity, $2.5 billion net liabilities) to acquire -$320 million in after-tax profit (NOPAT). The ROIC earned on this deal would equal -2%, well below GOOGL’s top-quintile 26% ROIC and less than the firm’s 8% weighted average cost of capital (WACC). To justify paying $16/share, Alphabet would need, at a minimum, Twitter’s NOPAT (assuming no capex) to reach $1.1 billion or 8% of the total potential purchase price. At that level, the deal would earn Alphabet an ROIC equal to its WACC, which is still a low and value-neutral hurdle, but at least the deal would not destroy value. For reference, the highest ever NOPAT earned by Twitter was -$49 million in 2012.

How Much Should Alphabet Pay?

To get a sense of how much Alphabet should pay for Twitter and not destroy shareholder value, we can look at reasonable scenarios for how much Alphabet can improve Twitter’s business to generate some cash flow. First, we account for liabilities that investors may not be aware of that make TWTR more expensive than the accounting numbers would suggest.

- $761 million in off-balance-sheet operating leases (7% of market cap)

- $118 million in outstanding employee stock options (1% of market cap)

Next, Figures 2 and 3 show the implied stock prices that Alphabet should pay for Twitter to achieve separate ‘goal ROICs’. Each implied price is based on different levels of revenue growth; 23%, 33%, and 43%. These revenue levels are equal to or higher than the consensus estimate for 2016 (23%). In each scenario, we conservatively assume that Alphabet can grow Twitter’s revenue and NOPAT without any additional capital spending beyond the purchase price.

Each scenario also assumes Twitter immediately achieves and maintains 7% NOPAT margins, which are the average between Alphabet, Facebook (FB), LinkedIn (LNKD) and Twitter. TWTR’s current TTM NOPAT margin is -13.5%.

Figure 2: Implied Acquisition Prices For GOOGL To Achieve 8% ROIC

Sources: New Constructs, LLC and company filings. $ values in millions except per share amounts. $ value destroyed equals the difference between implied total purchase price and current market price

The first ‘goal ROIC’ is 8%, which is equal to Alphabet’s WACC. The big takeaway from Figure 2 is that even if Twitter grows revenue by 43% compounded annually for the next five years, the most Alphabet should pay to ensure an ROIC equal to WACC is $13/share, or $2.3 billion (20%) less than the current market value. For reference, consensus estimates peg revenue growth at 23% in 2016 and 21% in 2017. Note that any acquisition that earned an 8% ROIC would be value neutral and not create shareholder value.

Figure 3: Implied Acquisition Prices For GOOGL To Achieve 26% ROIC

Sources: New Constructs, LLC and company filings. $ values in millions except per share amounts. $ value destroyed equals the difference between implied total purchase price and current market price

The next ‘goal ROIC’ is 26%, which is Alphabet’s current ROIC. In Figure 3, we see that even in the most optimistic scenario, the most Alphabet should pay for TWTR is $1.55/share, or 91% below the current price. Any price above $1.55/share would destroy shareholder value and decrease Alphabet’s ROIC.

The bottom line is that Alphabet’s management would have some explaining to do to justify an acquisition at $16/share, the current price of TWTR.

Conclusion

Until investors hold management accountable for intelligent capital allocation, they can expect companies to continue to destroy shareholder value without feeling any accountability to their investors. Given our analysis above, acquiring Twitter at any price near current valuations would be a very poor allocation of capital and would simply be a transfer of wealth from GOOGL shareholders to TWTR shareholders.

This article originally published here on June 27, 2016.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Photo Credit: Tom Raftery (Flickr)

1 Response to "Alphabet Should Pay No More Than $1.1 Billion For Twitter"

I think you are crazy wrong on this. Its funny how some people are writers and they know nothing. You base your uneducated opinion based on twitter.com. NOT Twitter Inc.

You think Twitter Incorpration is going to sell twitter.com, vine, periscope and fabric for 1.1 billion? You are out of your damn mind.

Periscope, as we saw the last few weeks is a HUGE asset. In congress plus the Nfl streaming, and the fact their revenue has gone up each qtr?

A blogger wouldnt know what stock based comp. Or Depr and amort. Exp Is and they wouldnt know how to account for it.

They have gotten more cash then lost the last 5 qtrs.

Income statement is fixed to benefit twtr.

Facebook, instagram and snapchat are social media.

Twitter is live.