Poultry producer Pilgrim’s Pride (PPC: $25/share) made news on Monday by announcing an unsolicited offer of $45/share for Hillshire Brands (HSH: $52/share), a 22% premium to where HSH had closed on Friday. The deal had a total value of ~$6.5 billion.

My initial reaction was that this offer significantly overvalued HSH. It offered PPC a return on invested capital (ROIC) of just 4%, while its weighted average cost of capital (WACC) stood at 11%. The deal would have been value destroying for PPC shareholders.

Fortunately, PPC has been bailed out from its mistake by Tyson Foods (TSN: $43/share), which announced this morning a $50/share bid for HSH. The ROIC on this deal would be even lower, about 3.7%. TSN has a much lower WACC than PPC at 6.7%, but this deal is still a long way away from creating value for investors.

TSN has offered the usual statements about positive synergies resulting from the deal, but unless these synergies can double HSH’s profits (not likely) the deal is bad for TSN investors.

A look at TSN’s 2014 Proxy Statement reveals why its executives may be willing to ignore the subpar returns on capital. Stock awards for executives are based largely on adjusted EBIT. Management knows that if they can grow EBIT, they will make more money, even if that earnings growth comes at the expense of shareholder value.

This focus on earnings at the expense of ROIC is harmful to companies, investors, and the economy in the long-term. There is a limited amount of capital, and when a company’s deployment of capital is suboptimal it means that higher return investments don’t end up getting funded. The misguided focus on EPS comes from a little-known accounting loophole called the high/low fallacy. We’ve written many times how this fallacy allows companies to show EPS growth from acquisitions even while the acquisition is a big shareholder value destroyer.

TSN earned an ROIC of 9% last year and has averaged an ROIC of 6% over the past decade. One has to imagine that they could earn a superior return by gradually employing capital to grow their business organically, but that wouldn’t provide the immediate EBIT (and possible executive compensation) growth that the HSH acquisition will.

TSN stock is up 5% on the news of the buyout offer, but long-term this is a bad deal for shareholders. It ties up a significant amount of capital in a low-performing asset and should add a significant amount of debt that will eat up future cash flows.

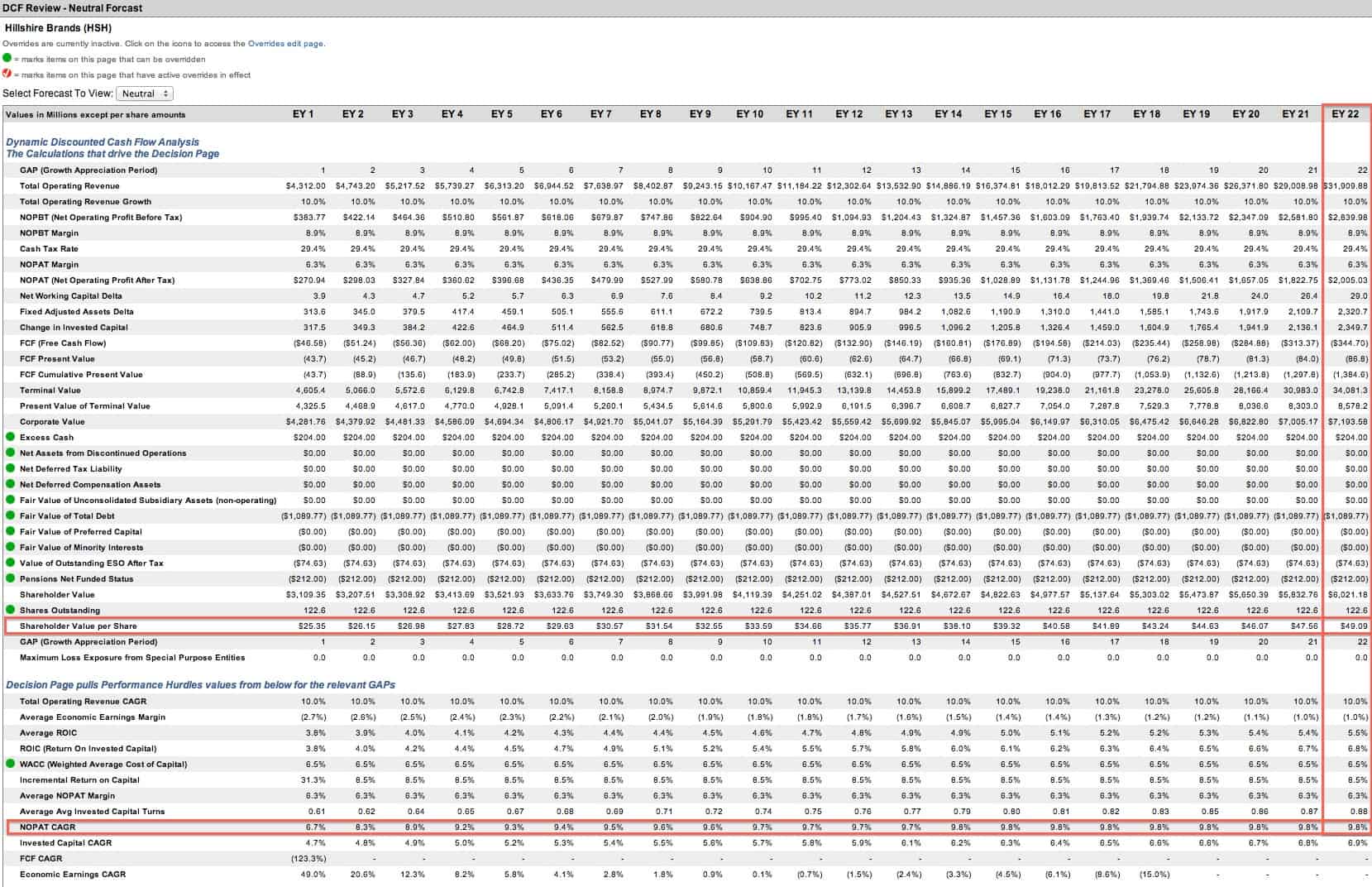

TSN investors can still hope that HSH will bail them out and reject the offer, but that doesn’t seem likely. This is a great deal for HSH, which would need to grow NOPAT by 10% compounded annually for 22 years to justify $50/share on its own.

{kind=link}

TSN’s best hope is that PPC comes back with an even higher offer. Such an offer wouldn’t make sense for PPC, but neither of the first two offers has made economic sense either. Incentive plans that encourage executives to chase short-term growth at the expense of healthy capital allocation make this sort of irrational behavior not just possible, but inevitable.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.