The recent popularity of the Global X Top Guru Holdings Index ETF (GURU) is a testament to the fact that investors are realizing the importance of a fund's holdings above all else.

Recent revelations about the illegalities of information flows at expert networks and hedge funds like SAC Capital signal, I hope, a long overdue decline in amoral activities that Wall Street insiders have exploited for decades to score outsized riches while the average investor is often left holding the bag.

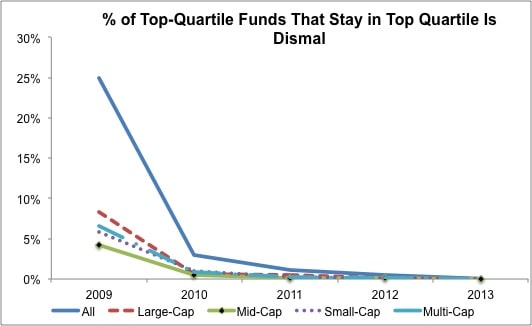

Trying to pick the next manager to get hot is not investing. It’s gambling, and the odds are heavily stacked against you. There is no substitute for good due diligence.

We applaud the Financial Accounting Standards Board's (FASB) latest proposal to change the way leases are reported. The new rules would make only the shortest-term operating leases exempt from being recorded on the balance sheet.

As the Chairman of the Financial Accounting Standards Board, or FASB, from 2002 to 2010, Robert Herz has had a much larger influence on financial markets than the average investor appreciates.

I believe the US economy is undergoing a restructuring where we, as a society, are becoming radically more productive. I think that we are entering a new economic paradigm of productivity in both our corporate and labor markets. In this new paradigm, we achieve enough gains in productivity to offset the inflationary forces of QE.

"New research on the performance of institutional portfolios shows that after risk adjustment, 24% of funds fall significantly short of their chosen market benchmark and have negative alpha, 75% of funds roughly match the market and have zero alpha, and well under 1% achieve superior results after costs—a number not statistically significantly different from zero."

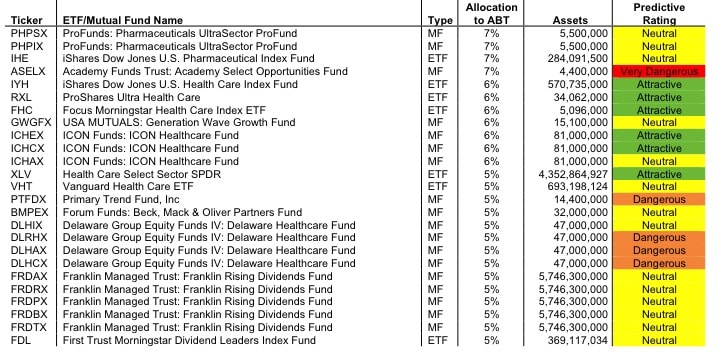

As detailed in "How To Make Money Picking Stocks", quantifying the future cash flow expectations embedded in stock prices is critical to making an informed investment decision.

My mentor, Michael Mauboussin, in his latest piece: " The Importance of Expectations – The Question that Bears Repeating: What’s Priced In?" explains more eloquently than I that the key to successful investing is to systematically distinguish between price and value – two very distinct concepts.

I explain key details behind our uniquely rigorous research process.

I also cover my top picks and pans in the "Hold It Or Fold It" portion of my interview with host Chuck Jaffe.

The advisors in Morgan Stanley Smith Barney's PMI Group are among the most sophisticated and conscientious that I have ever met. My presentation focused on how New Constructs makes diligence profitable and cost-effective.

When I ran across the recent article "270,033 pages later, a chance to catch our breath…", I could not help but admire footnoted.org's marketing moxy.

The article provides a count of the number of pages of 10-K filings that have poured in during the real earnings season. It also highlight a couple of the largest filings. At first glance, it is easy for one to assume that all of the 270,033 pages were also analyzed.

Here is the explanation behind why I suggested investors "brace" their portfolio and go net short in my "Don’t be fooled: Get short now" column on MarketWatch.com. In addition, I provide free reports on the stocks and funds I suggest shorting.