Check out this week’s Danger Zone Interview with Chuck Jaffe of Money Life and MarketWatch.com.

Utility sector ETFs and mutual funds are in the Danger Zone this week. The pickings in this sector are slim as every single ETF and mutual fund earns a Dangerous or Very Dangerous rating. The Utilities sector ranked last in our Sector Rankings report.

In this market environment, it’s not unusual for a sector to not have any Attractive funds. In fact, only Consumer Staples and Financials currently have any Attractive-or-better rated funds. However, the inability of any Utilities fund to even earn a Neutral rating is surprising. Every other sector manages to have at least one fund with a Neutral rating.

We put the Utilities sector in the Danger Zone towards the end of 2012, and sure enough it lagged the market significantly in 2013. However, as momentum stocks have turned over in 2014, investors have fled to high dividend Utilities. This rotation has driven the Utilities SPDR (XLU) up 14% so far this year. The false equivalency that dividends=safety has led investors to ignore the significant risks and bloated valuations of the stocks that Utilities funds hold. The truth is that Utilities funds have poor holdings and should continue to underperform the market going forward.

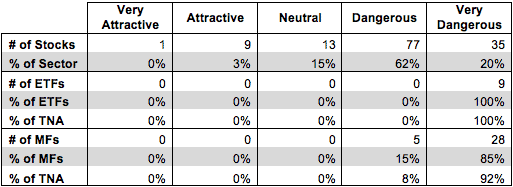

In fairness to Utility fund managers and ETF providers, there is a paucity of quality stocks in the sector. Figure 1 shows the breakdown of our ratings for Utilities stocks, ETFs, and mutual funds.

Figure 1: Utilities Sector Landscape For ETFs, Mutual Funds & Stocks

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Figure 1 actually overstates the quality of the stocks available in the Utilities sector. The one Very Attractive stock, Inteliquent (IQNT) is actually a Telecom stock, and 7 of the 9 Attractive stocks are actually outside the Utilities sector as well, like Master Card (MA) and Verizon (VZ). In the search for quality stocks, fund managers seem to be broadening the definition of “Utility”.

Good Utility stocks are hard to find because dividend-seeking investors have bid the prices up well beyond their fair valuations. Too often, investors evaluate stocks primarily based on dividend yield rather than looking at the underlying fundamentals first. This habit causes them to miss potential red flags. If the stock is overvalued, it will likely underperform, even with the dividend.

However, fund managers should still be doing better. Only two Utilities ETFs, XLU and First Trust Utilities AlphaDEX Fund (FXU) allocate more than 3% to Consolidated Edison (ED), one of the two Utilities stocks to earn an Attractive rating. No ETF or mutual fund in the Utilities sector allocates even 0.5% to Otter Tail Corp (OTTR), the other Attractive-rated Utility stock.

Instead, funds like the Rydex Series Funds: Utilities Fund (RYUTX) allocate heavily to poor stocks like Dominion Resources (D). D is one of my least favorite stocks held by Utilities ETFs and mutual funds and earns my Very Dangerous rating. Unsurprisingly for a Utility, D is a low growth company. Over the past decade, it has only grown after-tax profit (NOPAT) by 2% compounded annually, while its return on invested capital (ROIC) has fallen from 6% to 4%.

If D was cheap, these issues would not be as severe, but D is far from cheap. In order to justify is current valuation of ~$72/share, D would need to grown NOPAT by 6% compounded annually for 20 years. Given this utility’s track record, such a high growth expectation seems overly optimistic. The fact that D has nearly $25 billion (60% of market cap) in debt and a free cash flow yield of less than 1% should also raise questions over its ability to sustain its dividend.

RYUTX’s heavy allocation to D and other Dangerous and Very Dangerous stocks drives its Very Dangerous rating, as does the fund’s high costs. In addition to its 1.83% expense ratio, RYUTX charges investors a 1.8% front end load and transaction costs add another 1.16% in annualized costs. Combined, these add up to a total annual cost of 4.79%.

RYUTX is far from the only Utilities fund to charge high fees. In our Sector Rankings report, Utilities was one of only three sectors that failed to earn either an Attractive or Very Attractive total annual costs rating. The average Utilities sector ETF or mutual fund charges total annual costs of 1.84%, whereas in Consumer Staples, the cheapest sector, the average ETF or mutual fund charges total annual costs of just 1.45%.

These high fees are the final nail in the coffin for Utilities funds. Fund managers and ETF providers in the sector should be picking better stocks, but they do have fairly limited options considering the poor state of the sector overall. However, the fact that these managers and providers are charging such high fees for low-quality portfolios is inexcusable. Investors looking for exposure to the Utilities sector should focus on individual stocks.

Otter Tail Corp (OTTR) is my top pick in the Utilities sector. OTTR’s 9% ROIC is the highest out of all 82 Utilities stocks I cover. OTTR has also grown NOPAT by 10% compounded annually over the past decade. One would think these solid fundamentals would command a premium valuation, but that’s not the case for OTTR. At ~$29.50/share, OTTR has a price to economic book value ratio of just 0.9, which implies a permanent 10% decline in NOPAT. OTTR should easily surpass these low expectations.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.