Despite its best efforts, the Federal Reserve has been unable to push the economy to its targeted 2% annual inflation. For four years now inflation has stayed resolutely below that target even as the Fed deployed an unprecedented program of bond buying and low interest rates in an effort to push prices up.

While the analysts that predicted the Fed’s actions would lead to significant inflation probably overstated the power the central bank has on the economy, we think the most significant cause of low inflation has had nothing to do with monetary policy.

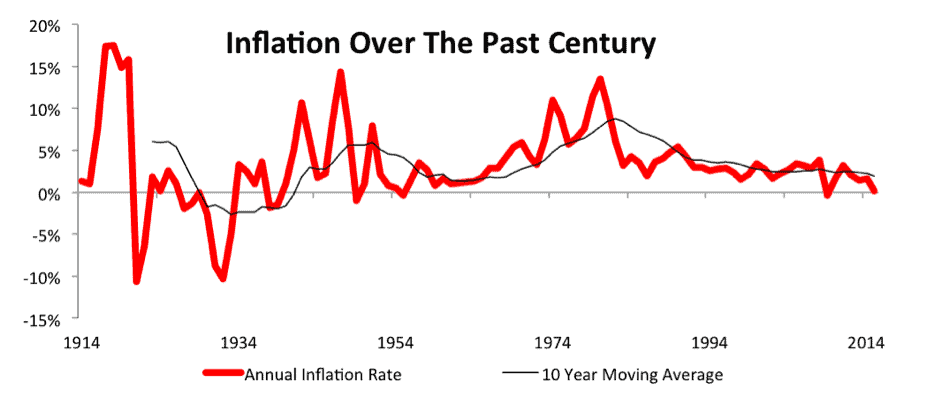

Figure 1: Trends In U.S. Inflation

Sources: Bureau of Labor Statistics

Figure 1 shows that since the early 80’s, the end of the “Great Inflation,” increases in the Consumer Price Index (CPI) have been steadily getting smaller and smaller. Compared to the wild swings of the rest of the 20th century, this trend represents a dramatic change.

This new trend coincides with a couple of major technological innovations that have had a long-term impact on prices:

- In the mid 1970’s, shortly before inflation peaked, Honeywell developed the first Distributed Control System (DCS) in the U.S., a tool that drastically increased the capability of factories to automate parts of the manufacturing process.

- In 1994, when we see a flattening of the inflation trend-line, Netscape Navigator was released. Netscape was the first web browser that made the internet accessible to the broader public and presaged the internet takeover of so many facets of the economy.

These technologies and the subsequent innovations they inspired have combined to hold down inflation by putting pressure on wages, increasing productivity, and encouraging competition.

Automation Puts Long-Term Cap on Wages

Automation puts pressure on wages by providing a substitute for low-end human labor. Industrial robots have replaced human workers in the manufacturing sector, self-service checkouts have replaced retail employees, and pretty soon more traditional white-collar workers will find themselves under pressure from technology.

At most organizations, human costs represent around 70% of total operating expenses. In the past, this structure made it hard to avoid a wage/inflation spiral, where higher wages pushed up costs, which pushed up prices, which necessitated even higher wages, and so on.

Today, it’s much harder for such a spiral to occur. In an increasing number of industries, companies can substitute technology for human labor when wages rise too fast and avoid raising prices. An increasingly educated population means that there will be high competition for the jobs that can’t be automated.

Technology Increases Productivity

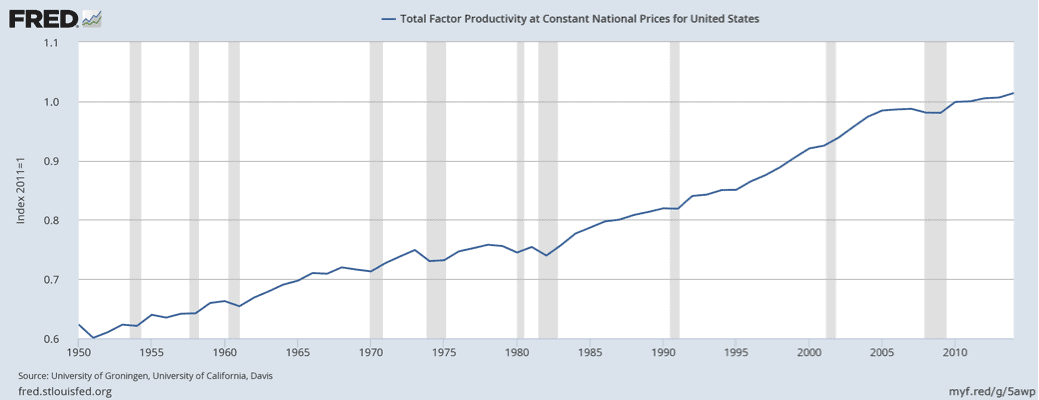

Much has been made recently about slowing productivity growth, but the longer-term view in Figure 2 shows that the U.S. has become radically more productive over the past several decades.

Figure 2: Increasing U.S. Total Factor Productivity

Sources: St. Louis Fed

Technology has contributed to that growth in many ways.

- Machines have automated many low skilled tasks, allowing workers to focus their efforts on areas where human intelligence and creativity can add more value.

- Improvements in communication technology have led to a more rapid transmission of ideas and reduced many of the frictions that impeded productivity growth and innovation.

- Our technology is constantly improving to be more energy efficient and use fewer raw materials.

- The rise of big data has yielded insights into ways to improve processes and weed out inefficiencies.

These are just some of the factors that have made the economy more productive and allowed American corporations to enjoy record profit margins even as prices stay steady.

The Internet Fosters Competition

While the effect of technology on wages and productivity have been discussed many times before, less attention has been paid to the role of the internet in fostering competition. The internet has reduced many of the traditional barriers to entry that protect companies from competition and created a race to the bottom for prices in a number of categories.

Consider the impact Amazon has had on the retail sector. Before the rise of e-commerce, many brick and mortar retailers enjoyed local monopolies or oligopolies based solely on geography. If you’re the only bookstore in the area, there’s not much pressure on you to keep prices low.

By circumventing the need for a physical location, Amazon was able to undercut retailers all over the world and rapidly achieve a scale that few others could rival. Now, every seller is competing with Amazon on price.

Moreover, all the tech giants that took advantage of the first wave of the internet to disrupt existing markets are competing with each other to dominate new categories. Google, Apple, Tesla (and now Ford) are building self-driving cars. Netflix has to compete in streaming video with Amazon, HBO, Hulu, and others. Every big tech company seems to be making bets on mobile payments, the Internet of Things, and virtual reality.

It’s easier than ever for a company with a great product to reach a wide range of customers and rapidly scale. It’s also easier than ever for dozens of copycats to immediately create their own competing versions of that product and try to undercut the prices of the original innovator.

Adjusting To The New Reality

As Jessica Rabe from Convergex points out in her “Memo From Millennials To Janet Yellen,” millennials are used to the idea of long-term low inflation.

“We live in a tech-based economy, where transparency relentlessly pressures prices. For millennials, lower prices show the economy is working well, rather than dampen consumption,” Rabe writes.

Whereas baby boomers grew up with the high inflation of the 1970’s, millennials have seen prices rise less than 2% annually since 2000. The generation that just become the largest segment of the population is comfortable with the idea of perpetually low inflation and expects more disruptive innovations that will lower costs for the broader population.

This trend towards lower prices through innovation could become even more pronounced in the future. Over the past twenty years, entertainment and luxury items have become much cheaper, but the costs of necessities such as food, housing, healthcare, education, and childcare have grown steadily.

Many in-process innovations hold the promise of bringing down the costs for these necessities. Here are a few:

- The increasing sophistication of artificial intelligence and robotics could automate some of the work done by doctors, teachers and nannies.

- Best practices in medicine, teaching and childcare can be broadcast globally at very low cost (e.g. MOOC’s and Khan Academy).

- 3D-Printed homes are already happening and could become more economical to build before too long.

- A wide array of innovations ranging from self-driving tractors to artificially created meat hold the promise of a radically cheaper food supply.

In fact, we’re already seeing some evidence for costs falling in these areas. Food prices in the U.S. have nearly set a 50-year record for the longest declining stretch. Housing inflation is starting to slow down in major cities. Numerous public and private universities are putting a freeze on tuitions.

Many business leaders are already predicting that technological innovation will have a radical impact on our daily lives. Carlos Slim, the Mexican telecom tycoon and fourth richest man in the world, believes we’re headed towards a three-day workweek.

While he acknowledges that this development may be still a ways away, it makes sense in a world of improved productivity and an increasing amount of automation. Businesses can afford to higher multiple employees with productivity so high, employees can afford to work less with a lower cost of living, and if robots keep doing more jobs there might not be enough jobs available for humans to work five days a week.

Impact On Economic Policy

The internet economy may be in the early stages of transforming our daily lives, but it’s already wreaking havoc on economic policy. As mentioned at the top of this piece, the Fed cannot manage to hit its 2% inflation target no matter how hard it tries, so maybe it should stop trying.

Historically, the Fed has had the “Dual Mandate” of maximizing employment and encouraging stable prices. If significant inflation is no longer a major worry for the economy, then all of a sudden the Fed has a very different outlook.

In my next article, I’ll dig deeper into how the internet economy has impacted monetary policy and what we should expect from interest rates going forward.

This article originally published here on September 22, 2016.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Scottrade clients get a Free Gold Membership ($588/yr value). Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.

Click here to download a PDF of this report.

Photo Credit: Beshef (Flickr)

3 replies to "How The Internet Economy Killed Inflation"

Great read!

Thank you, Sam. An excellent article with a compelling case. Much food for thought

Insightful. Well put.