Our Most Attractive and Most Dangerous stocks for July were made available to the public at midnight on Wednesday. June saw some strong performances from our picks. Most Attractive Small Cap stock Renewable Energy Group (REGI) gained 14%, and last month’s feature Syntel (SYNT) was up 9%.

The biggest decliner in our Most Dangerous portfolio was recent Danger Zone pick DreamWorks Animation (DWA), which fell 17%.

These successes underscore the benefit of our diligence. Being a true value investor is an increasingly difficult, if not impossible, task (see “Secrets to Annual Reports”). By scrupulously analyzing every word in annual reports, our research protects investors’ portfolios and allows our clients to execute value investing strategies with more confidence and integrity.

5 new stocks make our Most Attractive list and 8 new stocks fall onto the Most Dangerous list this month.

Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

Most Attractive Stock Feature For July: Neustar Inc. (NSR: ~$26/share)

Neustar (NSR) is one of the additions to our Most Attractive stocks for July. NSR has dropped 45% so far this year, including 11% in June, over fears that its contract to provide number portability services for North American Portability Management (NAPM), a telecom industry group, might not be renewed.

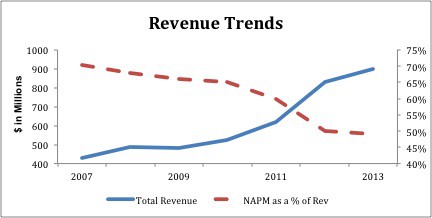

The loss of this contract would be hugely impactful, as it accounted for 49% of NSR’s revenue last year, but the market has still overstated the potential impact. Neustar has other profitable and growing businesses that, on their own, constitute a decent value at the current share price. Figure 1 shows how the NAPM contract has steadily declined in importance as NSR’s revenues have grown.

Figure 1: Other Businesses Booming

Sources: New Constructs, LLC and company filings.

Sources: New Constructs, LLC and company filings.

Neustar’s strong growth in its other businesses, which include marketing analytics, website monitoring and security, and data management, have helped it grow after-tax profit (NOPAT) by 16% compounded annually over the past nine years. NSR also earns a top-quintile ROIC of 15%.

Investors also shouldn’t fret over NSR’s Q1 earnings miss this year. NSR spent $3.6 million extra on advertising in Q1 in a campaign to try to keep the NAPM contract, a discretionary, non-recurring cost. Remove that $3.6 million expense and NSR likely meets its earnings estimates. Focusing on quarterly earnings beats and misses is a good way to get caught up in the noise and miss the true profitability of a company.

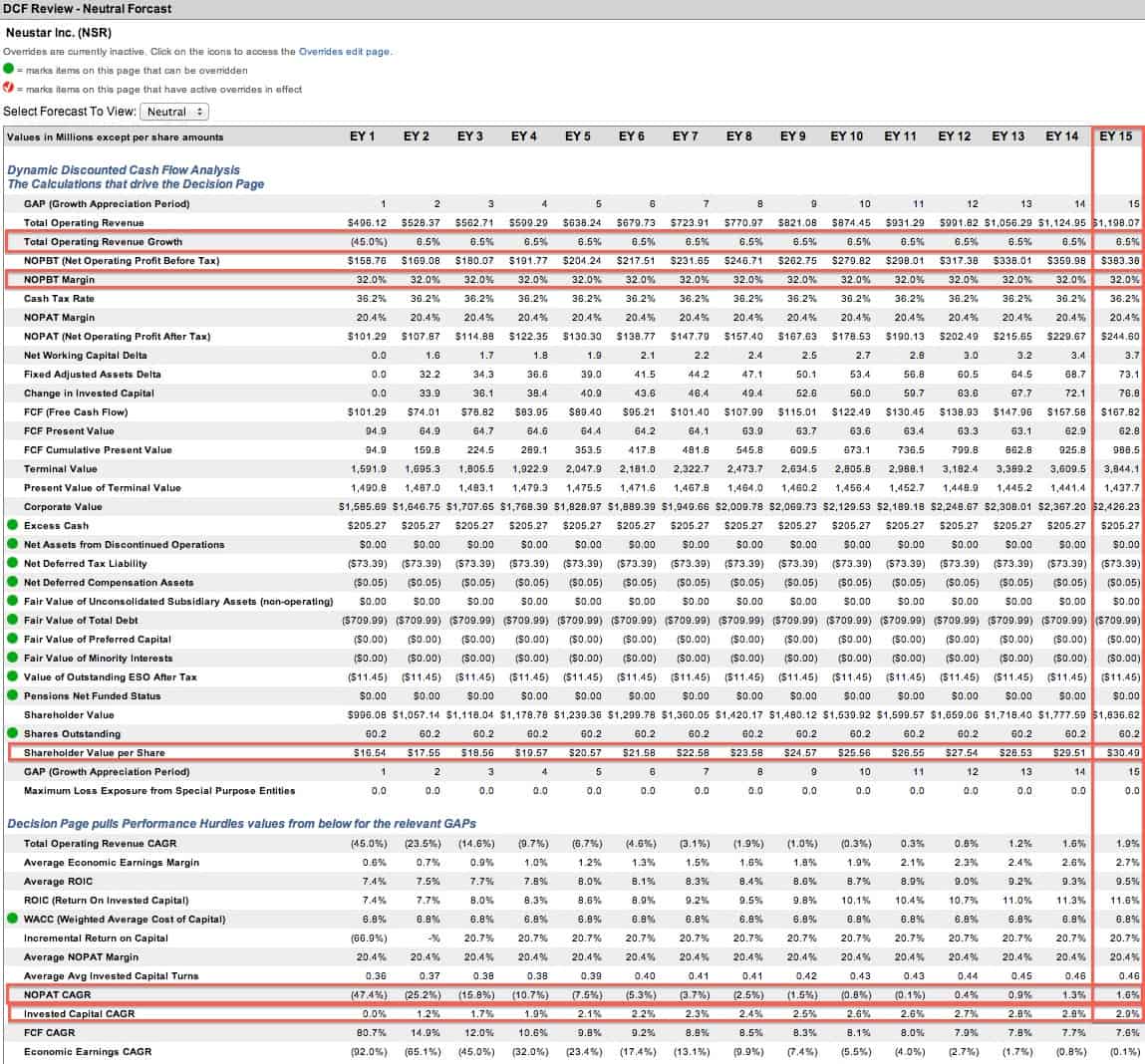

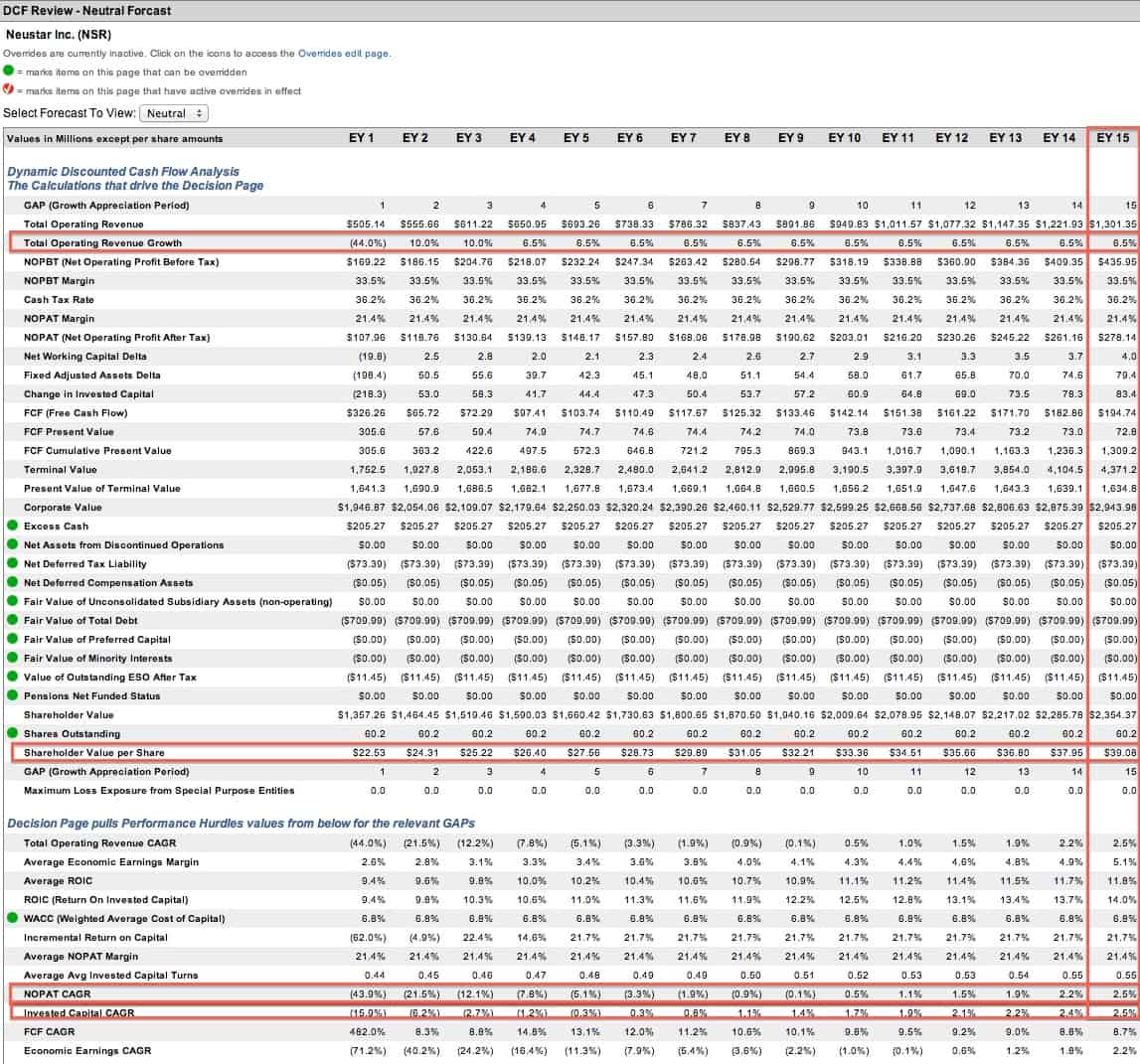

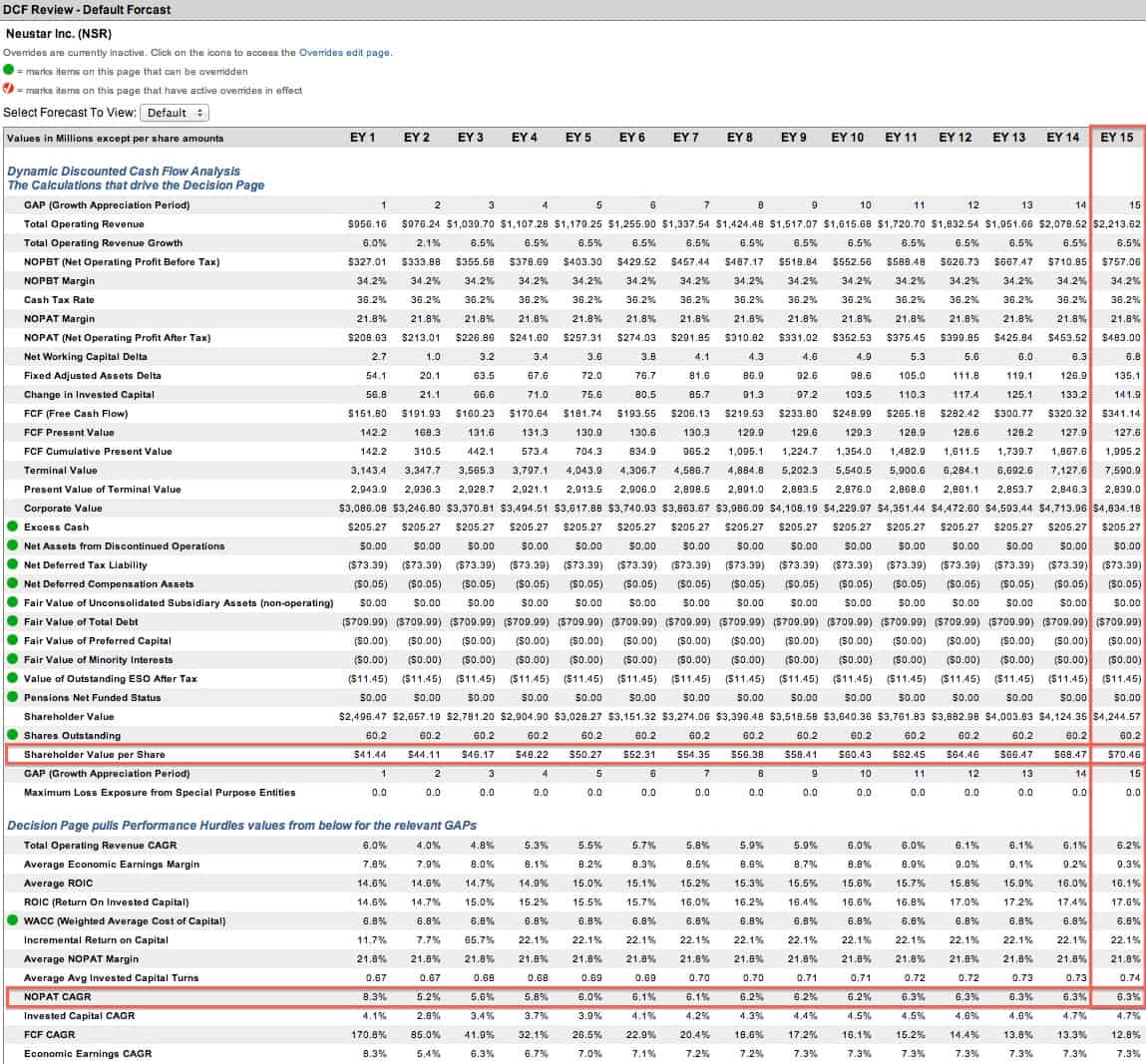

Given the uncertainty around NSR’s near-term future, it makes sense to model out multiple different discounted cash flow scenarios to try to approach a fair value for the stock. Here are three potential scenarios, from most pessimistic to most optimistic. All scenarios use a growth appreciation period (GAP) of 15 years.

- NSR loses the contract. In addition, its margins contract slightly, it is unable to generate any cash flow by selling off assets related to the NAPM business, and its remaining business grows sales at a long-term rate of 6.5%. Even with this pessimistic scenario, NSR still has a fair value of ~$30/share, or about 10% upside from its current valuation.

- NSR loses the contract. However, its margins remain intact, it is able to generate some cash by selling off assets, and its remaining business grows sales at 10% (the prior year rate) for the next few years before leveling off at 6.5%. In this scenario, NSR has a fair value of ~$39/share.

- NSR holds onto the contract. Nothing significant about its fundamentals changes and the company grows NOPAT at 6% compounded annually for the next 15 years. In this scenario, NSR has a fair value of ~$70/share.

{kind=link}

{kind=link}

{kind=link}

The North American Numbering Council has already advised the FCC to choose NSR’s competitor, Telcordia, for the contract, so scenario number three doesn’t look highly likely. However, the ultimate decision remains up to the FCC, so NSR could still retain the contract. The potential upside if this occurs is massive, over 150%.

Even under the most pessimistic scenario, NSR still looks slightly undervalued. It’s a case of heads you win big, tails you win small. No matter how heavily the odds are weighted towards tails, you come out ahead.

Most Dangerous Stock Feature For July: Exar Corporation (EXAR: $11/share)

Exar Corporation (EXAR) is one of the additions to the Most Dangerous list this month. The turnaround story is growing stale for this company that hasn’t earned consistent profits in years.

EXAR has not earned positive NOPAT for two consecutive years since the late ‘90s. In the past 15 years, it only managed to break even in 2013, when it earned less than $1 million in NOPAT.

The stock began to perk up in late 2011 and early 2012 when “turnaround specialist” Louis DiNardo was announced as CEO. Since DiNardo’s appointment, Exar has exhibited all the usual signs of a company trying to engineer a short-term bump in its stock price rather than long-term value creation.

Discretionary costs have been slashed. Selling, General, and Administrative costs have fallen by 27% since 2011, while Research & Development costs are down 46%. Naturally, when you cut your selling budget and stop developing new products, sales also fall, and revenues for the company are down 14%.

To counteract the revenue decline, EXAR has attempted to create buzz through a series of acquisitions, none of which have had a material impact on EXAR’s bottom line. However, they have created numerous opportunities for EXAR to exclude “one-time” acquisition and restructuring costs in order to report positive non-GAAP earnings. The 2014 acquisition of Cadeka Technologies also allowed EXAR to earn an income tax benefit of $6.8 million, which made GAAP net income positive while NOPAT was negative.

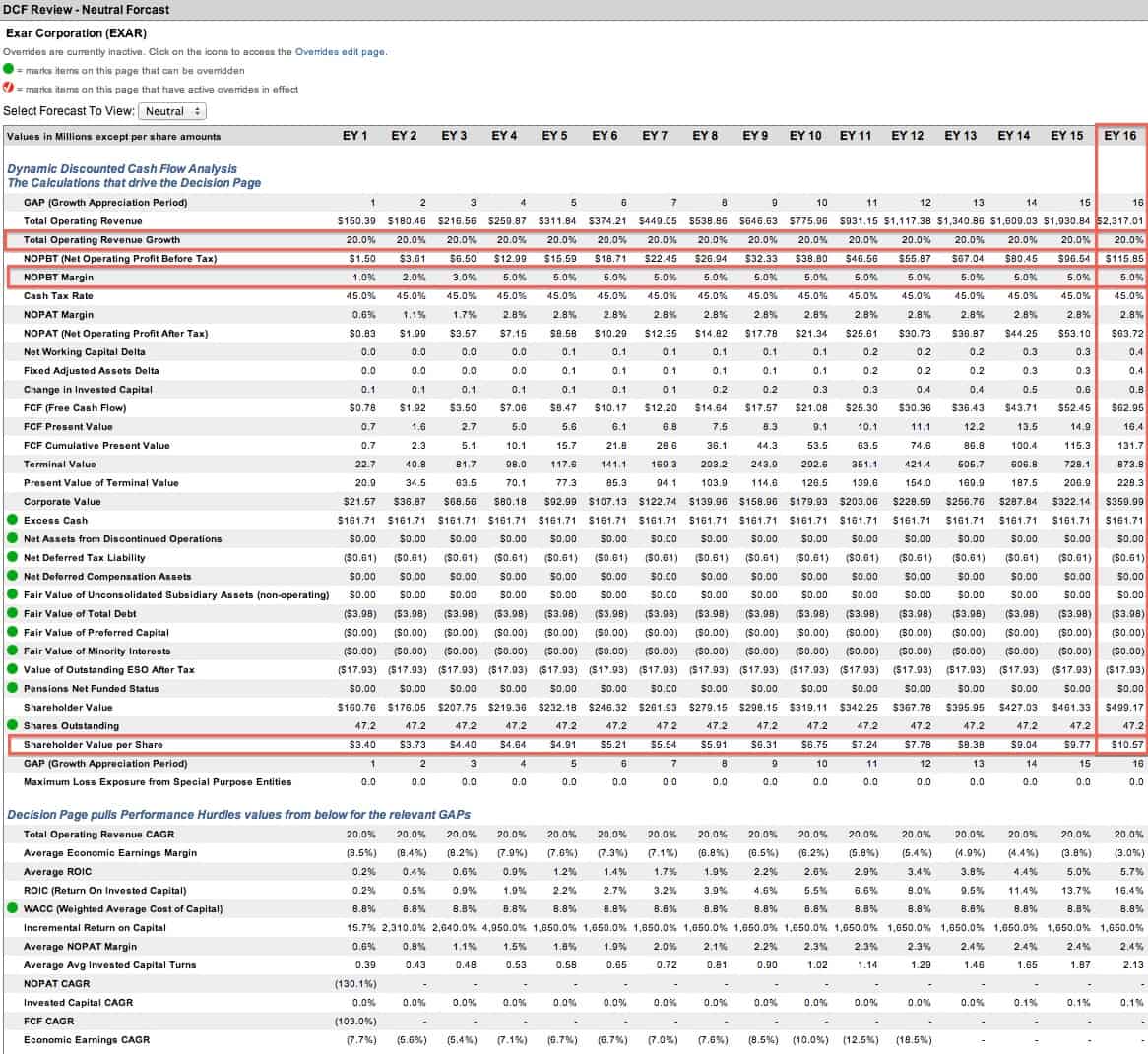

When one looks at the stripped down financials of EXAR without any of the accounting distortions, it becomes clear how significantly overpriced this company is. In order to justify its current valuation of ~$11/share, EXAR would need to achieve pre-tax profit margins of 5% while growing revenue by 20% compounded annually for 16 years. Remember, this is a company with no recent track record of consistent profitability and declining revenue.

{kind=link}

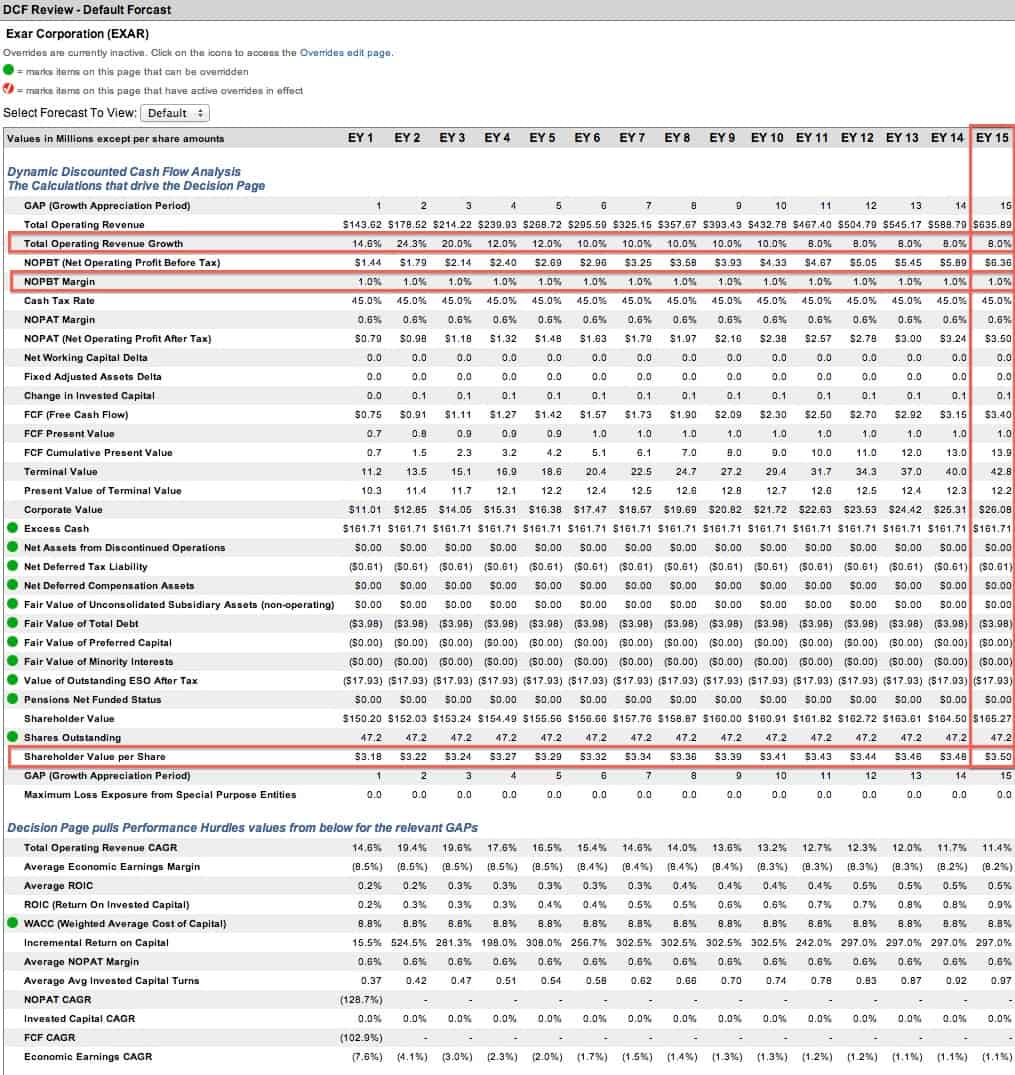

If EXAR can manage to just barely break even while growing revenue at a more measured rate of 11% compounded annually for 15 years, it has a fair value of just $3.50/share. Given the company’s track record, even this modest expectation seems unlikely.

{kind=link}

EXAR’s significant cash position and low debt mean that it’s not in danger of going to zero anytime soon, but it also doesn’t look as if this company is ever going to create significant value for shareholders.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.