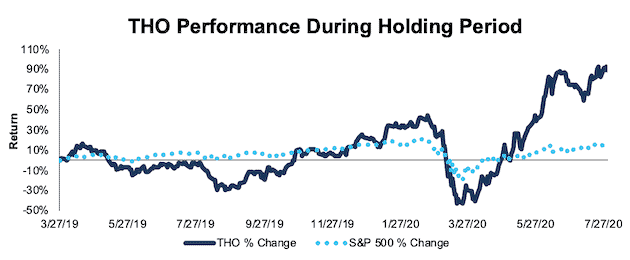

Thor Industries (THO) – Closing Long Position – up 90% vs. S&P up 16%

Thor Industries (THO: $116/share) was featured as a Long Idea on 3/27/19. At the time, Thor Industries received a Very Attractive rating. Our long thesis highlighted the firm’s industry leading profitability, long-term secular demand for RVs, and the stock’s cheap valuation.

This report, along with all of our research[1], utilizes our superior data[2] to get the truth about earnings, as shown in the Harvard Business School and MIT Sloan paper, “Core Earnings: New Data and Evidence.”

During the 492 day holding period, THO outperformed as a long position, rising 90% compared to a 16% gain for the S&P 500.

Thor’s profitability fell in 2019, as inventory and demand returned to more normal levels after a record 2018, and that trend has continued into the trailing-twelve-month (TTM) period. The firm’s return on invested capital (ROIC) has fallen from 17% at the time of our report to 6% TTM.

The deterioration in fundamentals, coupled with a soaring stock price (+60% year-to-date) due to optimism over RV demand during and after the COVID-19 pandemic, means THO no longer presents the same risk/reward. The firm now receives our Very Unattractive rating. We believe it is time to take the gains and close this long position.

Figure 1: THO vs. S&P 500 – Price Return – Successful Long Call

Sources: New Constructs, LLC and company filings

Note: Gain/Decline performance analysis excludes transaction costs and dividends.

This article originally published on July 31, 2020.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

[2] Our core earnings are a superior measure of profits, as demonstrated in Core Earnings: New Data & Evidence a paper by professors at Harvard Business School (HBS) & MIT Sloan. The paper empirically shows that our data is superior to “Operating Income After Depreciation” and “Income Before Special Items” from Compustat, owned by S&P Global (SPGI).