Compared to its competitors, CALD has less scale, inferior profitability metrics, and fishy accounting to boot. The stock’s valuation is so high that our DCF model can hardly make sense of it. The stock seems to be trading largely on the hopes of an acquisition.

There are too many competitors out there for CRM to grow revenue and expand margins simultaneously to the extent that the market valuation already implies. Too much downside risk is in this stock.

Without careful footnotes research, investors would never know the amount of employee stock options that decrease the amount of future cash flow available to shareholders by diluting the value of existing shares.

I am optimistic about the U.S. economy and I don’t believe we are in bubble. Too many investors and economists are looking at the economy the wrong way.

I believe the US economy is undergoing a restructuring where we, as a society, are becoming radically more productive. I think that we are entering a new economic paradigm of productivity in both our corporate and labor markets. In this new paradigm, we achieve enough gains in productivity to offset the inflationary forces of QE.

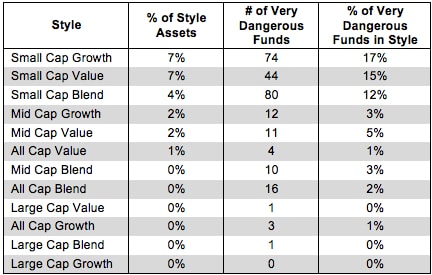

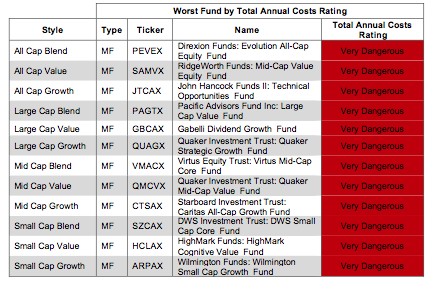

No fund style earns better than a Neutral rating at the beginning of the second quarter of 2013. My style ratings are based on the aggregation of my fund ratings for every ETF and mutual fund in each style.

Finding the best mutual funds is an increasingly difficult task in a world with so many mutual funds. Investors cannot trust mutual fund labels or names. They do not tell you enough about what you are getting when you buy a mutual fund.

This report identifies the “best” ETFs and mutual funds in January 2013 based on the quality of their holdings and their costs. As detailed in “Low-Cost Funds Dupe Investors”, there are few funds that have both good holdings and low costs. While there are lots of cheap funds, there are very few with high-quality holdings.

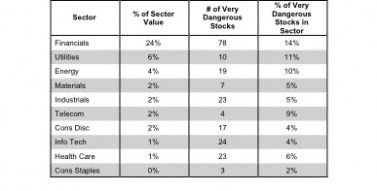

The Information Technology sector ranks second out of the ten sectors as detailed in my sector rankings for ETFs and mutual funds. It gets my Neutral rating, which is based on aggregation of ratings of 27 ETFs and 146 mutual funds in the Information Technology sector as of October 9, 2012.

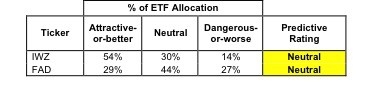

The all-cap growth style ranks fourth out of the twelve fund styles as detailed in my style roadmap. It gets my Neutral rating, which is based on aggregation of ratings of 2 ETFs and 457 mutual funds in the all-cap growth style as of April 24, 2012.

The large cap growth investment style ranks third out of the twelve investment styles as detailed in my style roadmap. It gets my Neutral rating, which is based on aggregation of fund ratings of all 771 funds in the style.

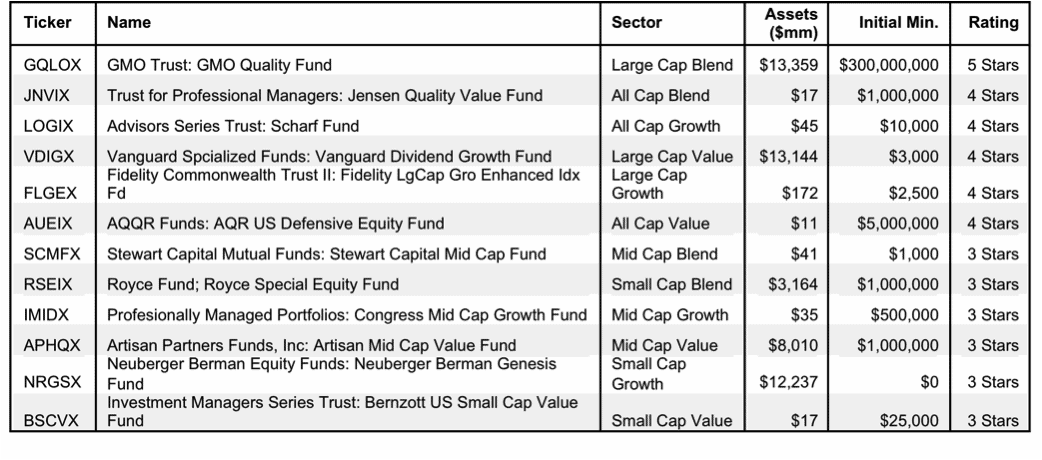

For those investors interested in rigorous research, I offer my roadmap to the best stocks and funds in the market by sector. The full sector roadmap is here.

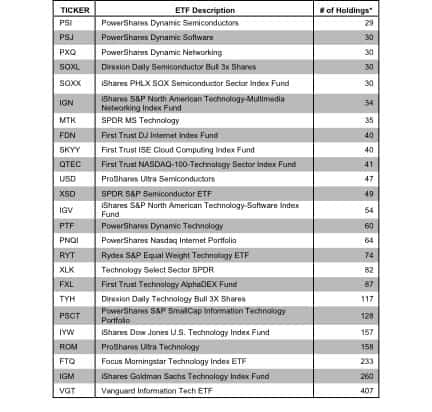

Having too many choices can be intimidating. And there are definitely lots of choices when it comes to ETFs. For example, in the equity market alone, there 30+ technology sector ETFs, or 35 ‘large cap value’ and 20 financial ETFs. A very healthy selection abounds for every category of ETF.

The problem is that these ETFs are not made the same even though they may be in the same category. There are major differences in methodologies between funds, which results in drastically different holdings even within a given sector. See Figure 1.

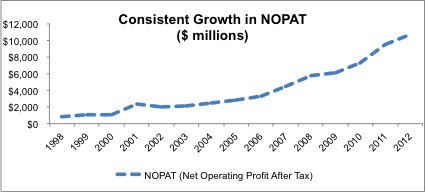

Over the past 10 years, ARBA appears as quite a success story and one of the few ‘internet bubble’ companies to survive and reach profitability, on a GAAP accounting basis at least. Looking beyond the reported accounting results, however, reveals that ARBA is not quite as profitable a company as it seems, and its valuation has out-grown its profits by a wide margin – the required combination of factors for making February’s list of most dangerous stocks.