Dan O’Connor, TechCXO Partner – Guest Contributor

David Trainer, CEO New Constructs

This article originally published here on January 30, 2017.

Executive Summary

A company’s market capitalization and enterprise value are linked together to provide alternative value measures for different stakeholders. Market capitalization reflects the value of a company from the common shareholder perspective that is translated into a share price. Enterprise value represents the sum of claims by all company stakeholders: creditors (secured and unsecured) and shareholders (preferred and common). Since US stock indexes reached all-time highs during November 2016, we were interested in analyzing the components of enterprise value to ascertain the proportion of enterprise value that is attributable to existing operations, versus expectations on a company’s ability to generate economic profits (as opposed to accounting profits) in the future.

We conducted an analysis, as of November 30, 2016, of companies included in the S&P 500 and the Russell 3000 to reverse engineer the components that make up each company’s total enterprise value. Leveraging data and analytics provided by New Constructs, we calculated for each company included in the Indexes how much of their total enterprise value was attributable to the current value of their operations and non-operating assets vs. the future value of their growth options. Previously, conducting such an analysis of both indexes simultaneously was infeasible due to technology limitations and scalability challenges. We were expecting to see the majority of enterprise value linked to companies’ future value of growth options. This is not what the analysis showed. From this analysis, there were several interesting insights, including:

- Invested Capital Represents the Largest Component of Enterprise Value

- Companies Struggle to Generate a Return on Invested Capital (ROIC) Greater than their Weighted Average Cost of Capital (WACC)

- ROIC Across Sectors Varies Significantly

- Future Value of Growth Options (FVGO) as a % of Enterprise Value was Lower than Anticipated

You create value for your company by investing capital to generate future cash flows at rates of return that exceed your cost of capital. Unless your company’s return on capital (ROIC) exceeds your cost of capita (WACC), no amount of revenue growth can create value. These principles apply equally to public companies as well as to privately-held enterprises.

For the Russell 3000, we identified 1,312 companies that have a Present Value of Economic Profit (Loss) in perpetuity totaling a negative $6.0 Trillion. If these 1,312 companies could earn a ROIC just equal to their WACC, shareholder value / enterprise value would increase by $6.0 Trillion, all other things being equal. We also identified 216 companies in the Russell 3000 that have a “negative” future value of growth options (FVGO) totaling $1.0 Trillion. If these 216 companies could reduce their “negative” FVGO to just zero, shareholder value / enterprise value would increase by $1.0 Trillion. Comparable results were obtained from our analysis of the S&P 500 Index companies.

The potential opportunity to unlock value for companies in the Russell 3000 can be even greater than the $7.0 Trillion detailed above. Think of the $7.0 Trillion as just getting back to “break-even” from an enterprise value perspective. If these companies identified above could start to earn a positive spread on ROIC vs. WACC, and convince the Capital Markets that they will create, rather than destroy, shareholder value in the future, this $7.0 Trillion opportunity could increase significantly.

We conclude this article by introducing a new paradigm for optimizing all the sources of capital of a company – monetary, physical, relational, organizational, and human capital that can be utilized by public companies as well as privately-held enterprises. This new framework can be deployed by executives at all levels throughout their organizations – Enterprise Level, Business Unit / Subsidiary level, and Individual Project Level. Strategic initiatives can be linked to their potential impact on enterprise value and share price in a transparent manner, providing “one version of the truth” that can be shared with all company stakeholders. Technology breakthroughs made by New Constructs and TechCXO allow enterprises of all size to close potential valuation gaps between their market value and intrinsic value. It is now possible to reverse engineer every part of your company’s enterprise value to isolate potential drags on your current share price and act proactively to:

- Avoid Valuation Traps

- Optimize all Components of Enterprise Value

- Improve ROIC

- Manage Innovation Initiatives as a Portfolio of Growth Options

- Align Stakeholder Expectations

The Analysis

We conducted an analysis, as of November 30, 2016, of companies included in the S&P 500 and the Russell 3000 to reverse engineer the components that make up each company’s total enterprise value.

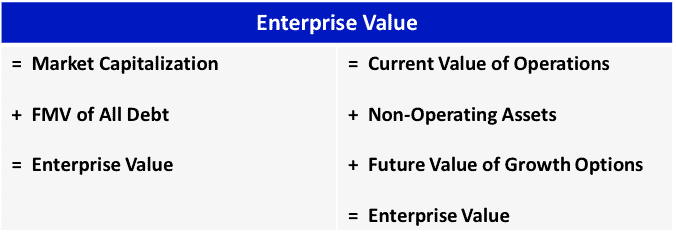

For purposes of this analysis, enterprise value is calculated in two ways:

Enterprise Value Components

Enterprise Value is a proxy for the takeover value of a company and can be difficult to calculate due to various accounting distortions, such as inventory reserves, asset write-downs, and off-balance sheet operating leases. Thus, the components of a company’s enterprise value cannot be easily extrapolated from their GAAP-based financials. For example:

- Non-Operating Assets include items such as excess cash, assets from discontinued operations, and unconsolidated subsidiary assets.

- Included in the FMV of All Debt are Executive Stock Options (after-tax), minority interests, and underfunded pension plans.

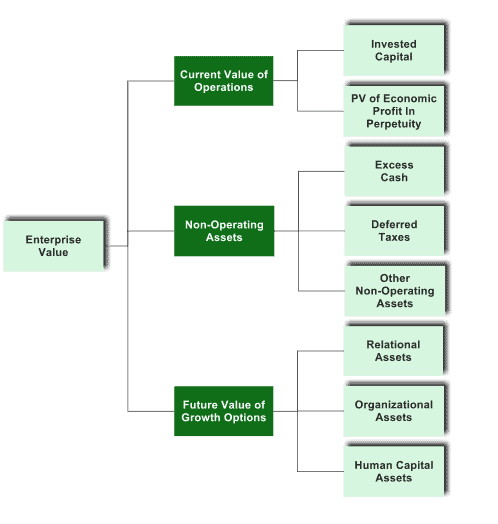

- Current Value of Operations is calculated as the sum of the company’s Invested Capital plus the Present Value of Economic Profit (Loss) in Perpetuity. Economic Profit differs significantly from GAAP-based net income as accounting distortions are removed, and a charge for the use of all capital is deducted in computing Economic Profit (Loss).

- The Future Value of Growth Options (FVGO) represents the Capital Markets’ assessment of a company’s growth initiatives. In other words, FVGO represents investors’ evaluation of the company’s “path-to-growth strategies” and their ability to create shareholder value in the future.

In summary, enterprise value can be viewed simply as the value of the company’s “Assets in Place” (Current Value of Operations Plus Non-Operating Assets) plus the value of “Assets to be Acquired in the Future” (FVGO).

New Constructs Analytics

Leveraging data and analytics provided by New Constructs, we calculated for each company included in the S&P 500 and Russell 3000 Indexes how much of their total enterprise value was attributable to the current value of their operations and non-operating assets vs. the future value of their growth options. Previously, conducting such an analysis of both indexes simultaneously was infeasible due to technology limitations and scalability challenges. New Constructs has solved the technology challenge by automating the data gathering from SEC filings (including accompanying footnotes) that are required for the proper analysis of each company’s enterprise value. Accounting distortions (30+ potential adjustments) are removed for each company, providing a standardized, “one version of the truth” to benchmark each company against peer groups and across industry sectors. New Constructs updates it data base daily, so enterprise value metrics are available in real time.

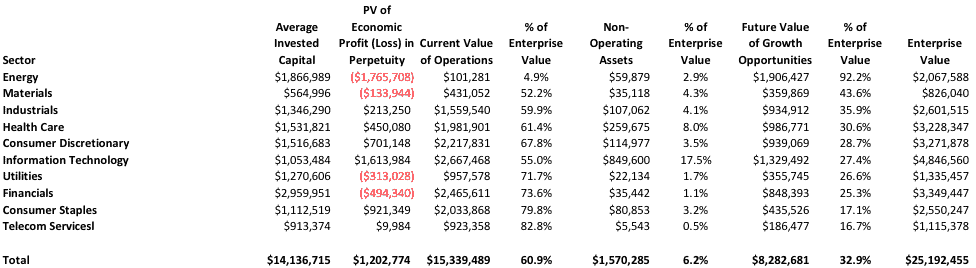

Summarized in the tables below are the enterprise value components (as of November 30, 2016,) for companies included in the S&P 500 and the Russell 3000 by sector:

Table 1: S&P 500 (Figures in Millions of USD)

Sources: TechCXO, New Constructs, LLC, and company filings

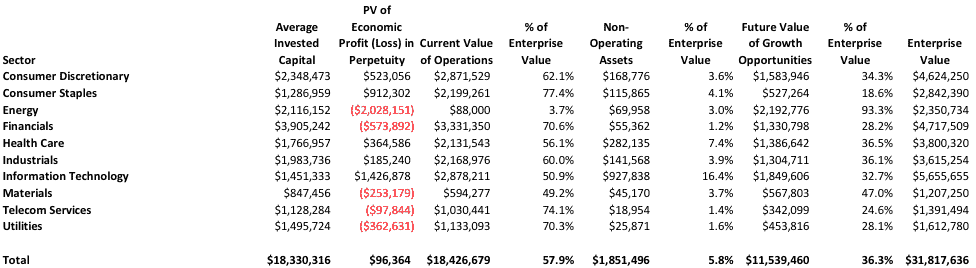

Table 2: Russell 3000 (Figures in Millions of USD)

Sources: TechCXO, New Constructs, LLC, and company filings

Since the turn of the century, the drivers of shareholder value / enterprise value have shifted away from monetary and physical assets to intellectual assets. Our objective for this study was to measure the components of enterprise value across large established companies (S&P 500) along with a broader base including small / mid cap companies (Russell 3000). In the tables above, Invested Capital includes not only traditional monetary and physical assets, but also intellectual assets reported on balance sheets such as Goodwill and other intangibles. Furthermore, New Constructs adjusts the calculation of Invested Capital to include off-balance sheet assets (i.e. operating leases), unrecorded Goodwill (due to pooling-of-interest accounting), along with asset reserves and accumulated write-downs for impairment charges. Intellectual assets – relational assets, organizational assets, and human capital assets – are usually not recorded on balance sheets due to accounting regulations, but never the less are key drivers of a company’s future value of growth options.

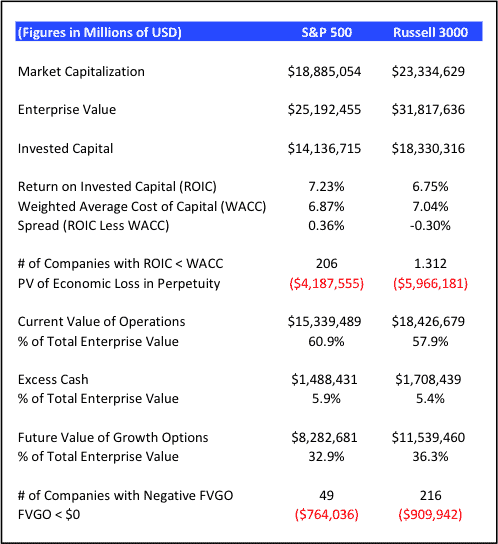

Table 3 below provides a summary of metrics comparing the S&P 500 with the Russell 3000 across key drivers of market capitalization and enterprise value:

Table 3 – Key Metrics

Sources: TechCXO, New Constructs, LLC, and company filings

Invested Capital Represents the Largest Component of Enterprise Value

Invested Capital base for the S&P 500 totaled $14.1 Trillion, or 56.1% of total Enterprise Value. For the Russell 3000, Invested Capital totaled $18.3 Trillion, or 57.6% of total Enterprise Value. As the Russell 3000 includes many emerging growth companies, it is interesting that they have a higher % of Enterprise Value attributable to Invested Capital vs. FVGO.

Companies Struggle to Generate ROIC Greater than WACC

The spread between ROIC and WACC is slightly positive for the S&P 500 (+ .36%), while the same spread for the Russell 3000 is negative (- .30%). This demonstrates that companies in both Indexes have capital efficiency challenges. Notice that the PV of Economic Profit (Loss) in Perpetuity for the Russell 3000 ($96 Billion) represents only .30% of total enterprise value. Digging deeper, there are 206 companies in the S&P 500 that have a Present Value of Economic Profit (Loss) in perpetuity totaling a negative $4.2 Trillion. For the Russell 3000, 1,312 companies have a Present Value of Economic Profit (Loss) in perpetuity totaling a negative $6.0 Trillion.

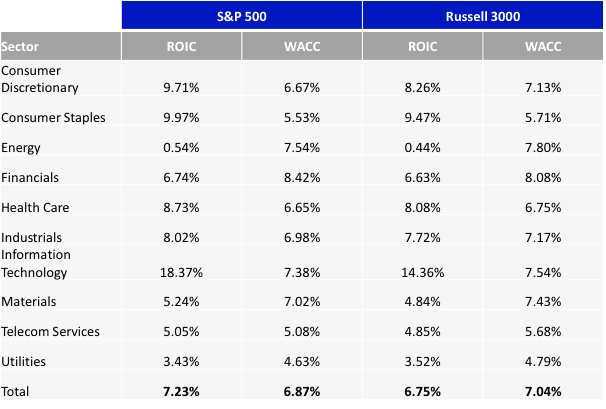

ROIC Across Sectors Varies Significantly

The technology sector had the highest ROIC for both the S&P 500 (18.37%) and Russell 3000 (14.36%). While the energy sector had the lowest ROIC for both the S&P 500 (.54%) and Russell 3000 (.44%). This is not surprising due to the precipitous drop in energy prices and large amounts of invested capital required.

Table 4: ROIC vs. WACC

Sources: TechCXO, New Constructs, LLC, and company filings

Excess Cash Holdings Dominated by Small Number of Companies

Companies in both Indexes hold a significant amount of excess cash (cash holdings greater that what is needed to operate the company). Excess cash balances for the S&P 500 totaled $1.5 Trillion (5.9% of total enterprise value) while excess cash balances for the Russell 3000 totaled $1.7 Trillion (5.4% of total enterprise value). However, our analysis revealed that over $1 Trillion of excess cash was held by just 25 large companies (i.e., Apple, Microsoft, Google, etc.) much of which is held overseas and not repatriated due to tax issues.

FVGO as a % of Enterprise Value Lower than Anticipated

The FVGO for the S&P 500 totaled $8.3 Trillion (32.9%), while the Russell 3000 future value of growth options totaled $11.5 Trillion (36.3%). We were surprised by these metrics as researchers and analysts have estimated that the majority of a company’s enterprise value is attributable to the future value of its growth options. Our analysis demonstrates that this assessment may not be valid.

The energy sector had the highest FVGO for both the S&P 500 ($1.9 Trillion) and Russell 3000 ($2.2 Trillion) along with the highest % of enterprise value – 92.2% for the S&P 500 and 93.3% for the Russell 3000. Telecom was the sector that had the lowest FVGO for both the S&P 500 ($186 Billion) and the Russell 3000 ($342 Billion). Consumer staples had the lowest FVGO % for the Russell 3000 (18.6%).

It was somewhat surprising that the FVGO as a % of enterprise value for the information technology sector – 27.4 % for the S&P 500 and 32.7% for the Russell 3000 – was not higher. Due to the continuous demands for innovation, technology companies may be unduly punished by the Capital Markets based on the accounting treatment for their investments in R&D and other intangibles that will create value in the future. Under US accounting rules, internally generated intangibles – through R&D (patents and trademarks), marketing (brands, customer relations), organizational improvements (systems, processes) or training (human resources) – are treated as expenses and charged immediately to expense. Since these investments are never reflected on a company’s balance sheet, it is difficult for the Capital Markets to assign a value to these investments, creating an undervaluation trap for technology companies. Also, researchers have shown that innovation-intensive companies are systematically undervalued due to cognitive biases of analysts – understanding innovation initiatives is difficult so they tend to overestimate downside risks.

We identified 49 companies in the S&P 500 that had a “negative” future value of growth options totaling $764 Billion. For the Russell 3000, 216 companies had a “negative” future value of growth options totaling $1.0 Trillion. Having a “negative” future value of growth options implies that the Capital Markets believe that the company will not earn a positive spread between its ROIC and WACC in the future and will destroy shareholder value. In other words, the Capital Markets are signaling to management that they do not “buy-in” to the company’s “path-to-growth strategy”.

The Opportunity

You create value for your company by investing capital to generate future cash flows at rates of return that exceed your cost of capital. Unless your company’s return on capital exceeds its cost of capital, no amount of revenue growth can create value. These principles apply equally to public companies as well as to privately-held enterprises.

Based on our analysis, if the 1,312 companies we identified in the Russell 3000 could earn a ROIC just equal to their WACC, shareholder value / enterprise value would increase by $6.0 Trillion, all other things being equal. Similar results were observed in our analysis of the S&P 500 – if the 206 companies identified could earn a ROIC equal to their WACC, shareholder value / enterprise value would increase by $4.2 Trillion.

Furthermore, if the 216 companies we identified in the Russell 300 could reduce their “negative” FVGO to zero, shareholder value / enterprise value would increase by $1.0 Trillion, all other things being equal. Again, similar results were observed in our analysis of the S&P 500 – if the 49 companies identified could reduce their “negative” FVGO to zero, shareholder value / enterprise value would increase by $764 Billion.

In summary, at the macro-level the potential opportunity for companies in the Russell 3000 can be even greater than the $7.0 Trillion detailed above. Think of the $7.0 Trillion as just getting back to “break-even” from an enterprise value perspective. If these companies identified above could start to earn a positive spread on ROIC vs. WACC, and convince the Capital Markets that they will create rather than destroy shareholder value in the future, this $7.0 Trillion opportunity could increase significantly.

At the individual firm level, the opportunities for unlocking value through improved capital efficiency and enhanced transparency in communicating the firm’s growth strategies can be in the hundreds of millions / billions of dollars. New Constructs has published a number of business cases demonstrating compelling value enhancement opportunities:

- How General Electric Can Prevent A $125 Billion Decline In Market Value

- How To Boost American Express (AXP) Value By $50 Billion

- Open Letter to Larry Ellison: How To Boost Oracle’s Value By $65 Billion

New Paradigm for Managing Enterprise Value

Even though we were surprised by the FVGO percentages of total enterprise value for both Indexes, a significant amount of enterprise value is attributable to expectations concerning growth opportunities.

FVGO is not a new concept. In their seminal 1961 paper, “Dividend Policy, Growth and the Valuation of Assets,” Merton Miller and Franco Modigliani (both Nobel Prize winners) divided company value into two components:

- Value of assets-in place – current value of operations plus non-operating assets

- Value of growth opportunities (FVGO) – assets to be acquired in the future that will earn a ROIC greater than the company’s WACC

Share prices, then are driven by two sets of expectations: the first concerns returns on existing assets; the second, returns on assets the company is in position to acquire in the future. Executives typically know a lot about how the market evaluates their company’s current operations. However, they lack an equivalent framework for assessing how the market is assessing their company’s FVGO and growth strategies.

The problem is that the assets that drive FVGO are mostly intangibles and intellectual capital assets. And part of the reason that executives lack a framework for managing FVGO is that one of their main sources of information, the existing financial reporting framework, overlooks most intangibles and almost all types of capital other than monetary and physical assets. GAAP-based financials provide no visibility into the value drivers behind a company’s enterprise value and “path-to-growth strategies”.

Until recently, there were no standard metrics to measure investors’ assessment of a company’s “path-to-growth strategy” that is reflected in its FVGO. This is the reason we have created a new paradigm for optimizing all the sources of capital of the company – monetary, physical, relational, organizational, and human capital that can be utilized by public companies as well as privately-held enterprises. Strategic initiatives can be linked to their potential impact on enterprise value and share price in a transparent manner, providing “one version of the truth” that can be shared with all company stakeholders. This new framework can be utilized by executives at all levels throughout their organizations – enterprise level, Business Unit / Subsidiary level, and Individual Project Level.

Call to Action

Technology breakthroughs made by New Constructs and TechCXO allow enterprises of all size to close potential valuation gaps between their market value and intrinsic value. It is now possible to reverse engineer every part of your company’s enterprise value to isolate potential drags on your current share price and act proactively to:

- Avoid Valuation Traps

- Optimize all Components of Enterprise Value

- Improve ROIC

- Manage Innovation Initiatives as a Portfolio of Growth Options

- Align Stakeholder Expectations

By leveraging new data analytics, along with the framework described above, executives can now take a holistic approach for optimizing each component of their company’s enterprise value.

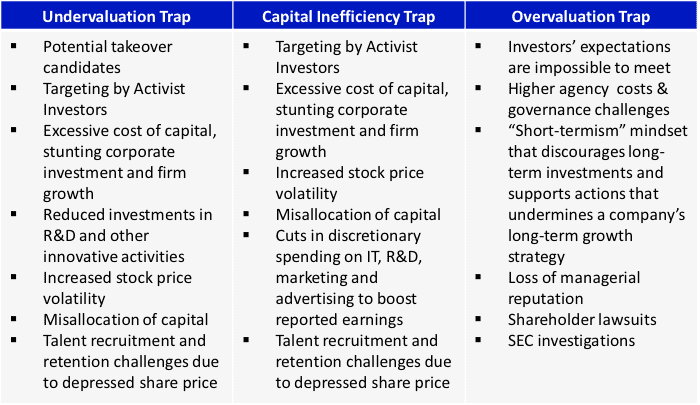

Avoiding Valuation Traps

Our analysis of companies included in the S&P 500 and Russell 3000 allowed us to quickly identify companies that fall into the following types of valuation traps:

- Undervaluation Trap

- Capital Inefficiency Trap

- Overvaluation Trap

Negative consequences are associated with each valuation trap (see Table 5), and executives need to take corrective actions immediately:

- Companies that fall into the Undervaluation Trap typically earn a ROIC greater than their WACC and the growth rate embedded in their current share price is negative, or significantly below the consensus analysts forecasted growth rate.

- Companies that fall into the Capital Inefficiency Trap typically earn a ROIC less than their WACC and the growth rate embedded in their current share price is significantly below the consensus analysts forecasted growth rate.

- Companies that fall into the Overvaluation Trap typically have a growth rate embedded in their current share price that is significantly above the consensus analysts forecasted growth rate.

Table 5: Valuation Traps

Sources: TechCXO, New Constructs, LLC, and company filings

Optimizing all Components of Enterprise Value

To avoid these valuation traps, executives should take a holistic approach for optimizing all components of their company’s enterprise value:

Current Value of Operations: Work existing assets harder (profitable revenue growth, intelligent cost reduction, working capital optimization, infrastructure rationalization).

- Non-Operating Assets: Leverage research studies to understand how Capital Markets react to various capital allocation decisions (new investments, share repurchases, dividend increases, M&A, spin-offs, divestitures).

- Future Value of Growth Opportunities: Embed “Agile” principles and “Design Thinking”, along with latest financial technologies to measure and manage growth initiatives (Product / Service Innovation, Operations Innovation, Business Model Innovation).

Improving ROIC

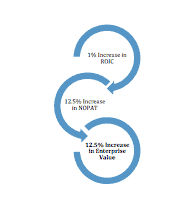

Capital allocation is a senior management team’s most fundamental responsibility. The objective of capital allocation is to build long-term value. This is a fundamental principle of value creation and applies to publicly-trade and privately-held companies at all stages of a company’s life cycle. Capital efficiency is measured by the metric Return on Invested Capital. ROIC has the most impact on Enterprise Value than any other metric. For additional insights on the importance of ROIC as driver of enterprise value, see ROIC: The Paradigm For Linking Corporate Performance To Valuation.

Increasing ROIC by just 1% can lead to significant increases in a company’s operating profits & Enterprise Value. For example, if a company’s ROIC is 8%, and its WACC is 8%, a 1% increase in ROIC leads to a 12.5% increase in Net Operating Profits and a 12.5% increase in enterprise value / shareholder value.

A New Approach for Managing Innovation Initiatives

A New Approach for Managing Innovation Initiatives

A company’s ability to optimize its FVGO is dependent on how fast it can innovate and create new products / services that will earn a ROIC greater than its WACC. However, the analysis of innovation initiatives is one of the most difficult management challenges as investments may be required over a number of years during periods of high uncertainty. Traditional Valuation Methodologies, such as Discounted Cash Flow and Net Present Value, systematically undervalue innovation initiatives since they cannot account for the value of managerial flexibility and ignore the future value of growth opportunities the investment can generate.

Advances in enabling technologies (i.e., simulation, scenario planning, optimization engines) and data analytics have provided executives with the tools they need to predict the impact of innovation initiatives on enterprise value more accurately, allowing managers to redeploy capital to more promising opportunities as uncertainties are resolved over time.

Aligning Expectations

Top management is the most informed stakeholder for setting expectations for both external stakeholders (analysts, debt holders, shareholders) as well as internal stakeholders (Board of Directors, Business Unit Managers). Executives need to explain in a transparent manner how their capital allocation initiatives align with the company’s path-to-growth strategy.

Due to the shrinking relevance of accounting information, external stakeholders (analysts, shareholders, SEC) are encouraging companies to provide Non-GAAP disclosures that provide insights into the true economic performance of the enterprise, along with transparency into the key drivers of the enterprise’s growth opportunities.

Communications with analysts, investors and advisors is complicated due to potential litigation if things don’t turn out as projected. However, recent research shows that enhanced disclosures decreases stock price volatility and mitigate the consequences of shareholder litigation.

Concentrated efforts should be made by senior executives to understand the basis of the assumptions used by analysts in evaluating their company’s current and future growth prospects. Gaps between top management and analysts’ expectations should be resolved to reduce surprises in the future. In other words, the objective is to reduce the information cost of external stakeholders and reduce the “noise” surrounding expectations.

Organizations that excel at aligning expectations realize the following benefits:

- Reduced information asymmetry

- Intrinsic value of enterprise aligned with market value

- Reduced litigation risk

- Valuation gaps reduced or eliminated

- Reduced stock price volatility and cost of capital

About the Authors

Dan O’Connor Partner TechCXO

Email: dan.oconnor@techcxo.com

LinkedIn: https://www.linkedin.com/in/dan-o-connor-ab911513

About TechCXO

TechCXO is an executive professional services firm that addresses our clients’ most critical functional and strategic issues in obtaining capital, entering new markets, increasing revenue, improving margins, and optimizing enterprise value.

David Trainer CEO New Constructs

Email: david.trainer@newconstructs.com

LinkedIn: https://www.linkedin.com/in/davidtrainer

About New Constructs

New Constructs leverages the latest in machine learning to analyze structured and unstructured financial data with unrivaled speed and accuracy. The firm’s forensic accounting experts work alongside engineers to develop proprietary NLP libraries and financial models based on the best fundamental data in the business for stocks, ETFs and mutual funds. Clients include many of the top hedge funds, mutual funds and wealth management firms. Partnerships with Thomson Reuters, Scottrade, Interactive Brokers and Ernst & Young provide leveraged distribution into multiple markets. David Trainer, the firm’s CEO, is regularly featured in Barron’s, Marketwatch.com, The Wall Street Journal and on CNBC as a thought leader on earnings quality, valuation and investment strategy.

Disclosures: David Trainer and Dan O’Connor receive no compensation to write about any specific stock, sector, style, or theme.

Click here to download a PDF of this report.

Photo Credit: Taxcredits.net (Flickr)