Weighted average cost of capital (WACC) is the weighted average of the costs of all external funding sources for a company.

WACC plays a key role in our economic earnings calculation. It is hard to be 100% certain about the exact cost of a company’s capital. Our guiding principle when calculating WACC is that it is better to be vaguely right than precisely wrong. We make sure that WACCs are reasonable first and employ many rules to normalize the inputs to WACC to ensure none of them cause an abnormal WACC to occur in any of our models.

The formula for WACC is in Figure 1.

Figure 1: How To Calculate WACC

(Ke) * (E/TC) + (Kd * (1-T)) * (D/TC) + Kp * (P/TC)

where:

Sources: New Constructs, LLC and company filings

The primary drivers of WACC are the cost of equity and cost of debt. More details on how we calculate each of these is below:

Cost of Equity

- Based on the capital asset pricing model (CAPM).

- We use the market value of equity when calculating all total adjusted market capital ratios.

- The equity risk premium is the average of the current implied equity risk premium and the historical implied equity risk premium.

- For beta, we use industry and sector averages, which we calculate based on daily prices over the past five years. We are careful to normalize beta to avoid it having undue influence on the cost of equity.

Cost of Debt

- Risk-free-rate is approximated by 5-year zero-coupon STRIPS.

- We add the debt spread associated with the debt rating on the company’s long-term debt to the risk-free-rate.

- The resulting pre-tax cost of debt is then multiplied by (1- marginal tax rate).

- We use debt ratings from Moody’s or S&P.

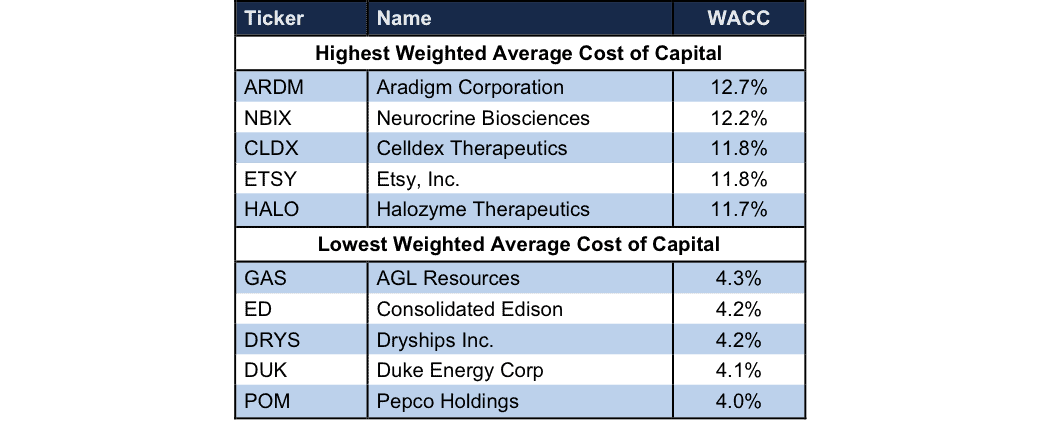

If a company fails to generate a return on invested capital (ROIC) greater than its WACC, it is destroying shareholder value. Figure 2 shows which companies have the highest and lowest WACCs.

Figure 2: Companies With Highest/Lowest WACC

Sources: New Constructs, LLC and company filings.

Aradigm Corporation (ARDM) has the highest WACC of 3000+ companies under coverage. See ARDM’s historical WACC dating back to 1998 in our model here. The company has never earned a ROIC greater than WACC in any year of our model. As such, the company has generated negative economic earnings each year as well. WACCs affect on ARDM’s economic earnings can be seen in our reconciliation of GAAP net income to economic earnings here.

Neurocrine Biosciences (NBIX), Celldex Therapeutics (CLDX), Etsy (ETSY) and Halozyme Therapeutics (HALO) rank two through five in highest weighted average cost of capital.

Pepco Holdings (POM) has the lowest WACC of all companies under coverage. See POM’s historical WACC dating back to 1998 here. Over the past decade, Pepco’s ROIC has stagnated around a bottom quintile 3%. The last time Pepco earned a ROIC greater than WACC was 2001. AGL Resources (GAS), Consolidated Edison (ED), Dryships (DRYS), and Duke Energy (DUK) round out the list of lowest WACC across all companies under coverage. WACC’s affect on ED’s economic earnings can be seen here.

Our models and calculations are 100% transparent because we want our clients to know how much work we do to ensure we give them the best earnings quality and valuation models in the business.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.