Recap from February’s Picks

Our Most Attractive Stocks (+1.5%) underperformed the S&P 500 (+2.0%) last month. Most Attractive Small Cap stock EZchip Semiconductor (EZCH) gained 11% and Most Attractive Large Cap stock Hasbro (HAS) was up 13%. Overall, 17 out of the 40 Most Attractive stocks outperformed the S&P 500 last month.

On to March’s Picks

Our Most Attractive stocks for March were made available on March 5. Our Most Attractive stocks have high and rising returns on invested capital (ROIC) and low price to economic book value ratios.

Most Attractive Stock Feature for March: Teva Pharmaceuticals (TEVA)

One of the new additions to our Most Attractive stocks list for March is Teva Pharmaceuticals (TEVA), an Israeli pharmaceutical company and the largest generic drug manufacturer in the world. The stock is up 9% this year. While Teva has a challenging 2015 ahead of it, we’re confident in this company’s ability to weather the storm and to continue to deliver value for its shareholders as it has done for years.

A Relatively Unknown Winner in Pharmaceuticals

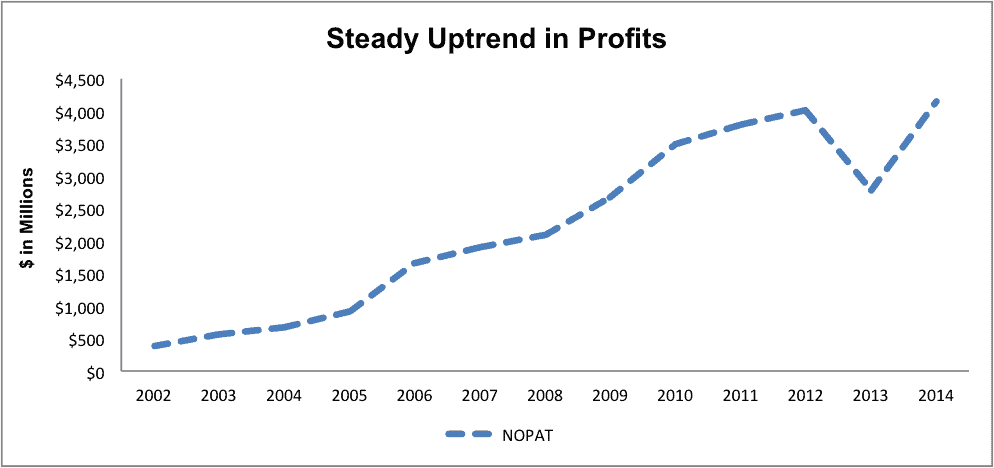

Since 2002, Teva has grown net operating profit after tax (NOPAT) by an impressive 22% compounded annually. The driving forces behind this growth have been 1) Teva’s dominance in the generic drugs market and 2) sales of Copaxone, Teva’s groundbreaking treatment for Multiple Sclerosis. In 2014, Teva produced 14% of all generic prescriptions in the United States.

Figure 1 provides a look at how Teva has grown NOPAT since its public listing in 2002.

Figure 1: Teva’s Long Term Success

Source: New Constructs, LLC and company filings

Teva currently earns an ROIC of 10%, up from 9% in 2012. NOPAT margins are near historic highs at 21% while revenue was mostly flat in 2014. 2014 also saw Teva hit new highs in terms of free cash flow, over $4.7 billion, while its margins and ROIC were strong in the face of flat sales.

Like many pharmaceutical companies, Teva has taken on a large amount of debt — $12 billion, or over 23% of Teva’s market cap — to fund its research and acquisition efforts. However, Teva’s abundant free cash flow discussed earlier should ease concerns about servicing its debt.

How Much Does This Roadblock Matter?

Teva has done a great job increasing its profitability in the face of flat sales. But what about when sales fall?

The drug that made Teva what it is today is Copaxone, a patented treatment for multiple sclerosis. As is the case with all patents, this drug’s patents must expire — this one in September 2015. The problem with this is that half of Teva’s Specialty Medicines (non-generic medicines) profits and revenues come from this single drug. Specialty Medicines makes up 42% of Teva’s revenues and 69% of its reported operating income.

Teva is currently embroiled in a legal battle over whether or not its patent that protected Copaxone until September is invalid. If the company can secure this patent, it has time to switch patients in the U.S. and especially Europe to its new, thrice-weekly version of Copaxone, patented until 2030. In 2014, 60% of Copaxone prescriptions in the U.S. were for this new version..

The expiration of the Copaxone patent will dramatically affect Teva even if it has more time to transition consumers to the new, patented version. In January, the U.S. Supreme Court overturned the federal appeals court decision that invalidated the patent, and sent it back to the court for further review, so Teva has a few more months to continue transitioning patients to its new, patented version of Copaxone.

Cheaper generics (that necessitate higher injection rates than this new version) will undoubtedly take some of the market when this patent expires. This looks to have already been priced in though, and a recent study found that higher injection rates for Copaxone would increase the amount of complications for patients.

Aside from preparing for this “patent cliff,” Teva has several other strategies it is pursuing. On top of aggressive cost-cutting measures that are expected to increase operating margins by 600 basis points in 2015, the company is pursuing niche markets in manufacturing increasingly complex generic drugs that other manufacturers tend to shy away from. The lack of competition in these niche spaces should also help soften the margin impact from the Copaxone expiration.

Current Valuation Allows for Patent Risk and Huge Upside

At its current price of ~$61/share, TEVA has a price to economic book value ratio of just over 0.8. This ratio implies that the market expects the company’s profits to permanently decline by 20%. This seems unlikely given the increasing demand for pharmaceuticals worldwide, and considering Teva’s history of profit growth in Figure 1.

Moreover, Barron’s has noted that Teva could be shopping around for a potential acquisition target, as it has thus far sat out of the recent pharmaceutical M&A boom. This provides the possibility of a large upward catalyst for TEVA, as it has done for other, less attractively valued pharmaceutical companies this year.

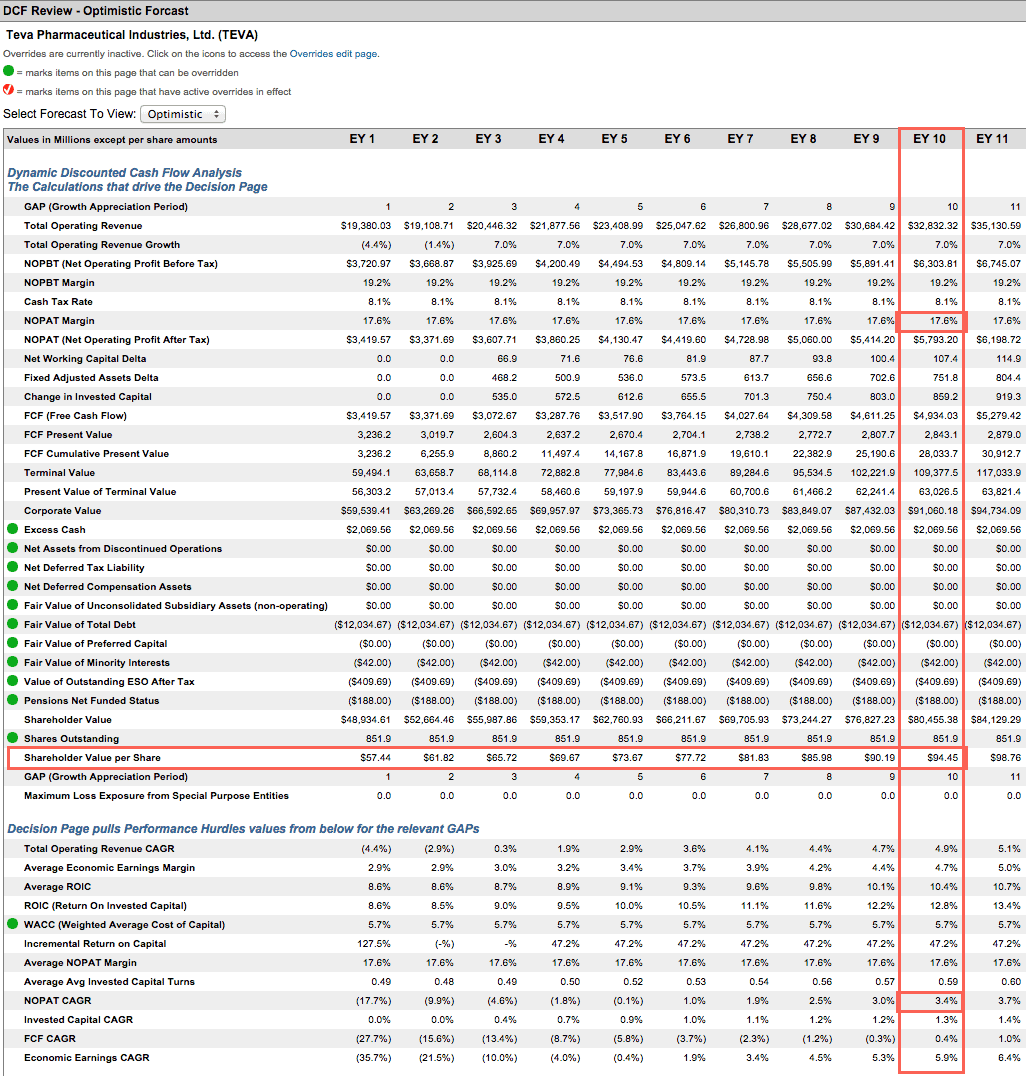

If Teva can grow NOPAT by just 3% compounded annually for the next 10 years, the stock is worth $94/share, a 52% upside from current levels. We think that Teva has the potential to do much better than even this scenario indicates, which is why it makes our Most Attractive stocks list this month.

{kind=link}

Disclosure: David Trainer and André Rouillard receive no compensation to write about any specific stock, sector, or theme.