Our Company Valuation models are very sophisticated discounted cash flow and earnings quality models.

An enormous amount of works goes into every model. I wish I could offer a short-cut (beyond our ratings and reports) for understanding our models.

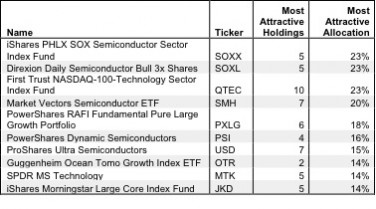

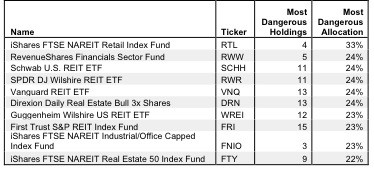

My ratings on ETFs are unique because they are based on my stock ratings for each of a fund’s holdings.

Analyzing and rating an ETF based on its holdings delivers many interesting insights:

My ratings on ETFs are unique because they are based on my stock ratings for each of a fund’s holdings.

Ergo, the “Most Dangerous” ETFs allocate the most capital to stocks on March’s Most Dangerous Stocks list, which is available for non-subscribers as of today. There are 40 stocks on the Most Dangerous list every month.

Be wary of advice from the bandwagon riders. They care more about getting more people in the bandwagon than anything else.

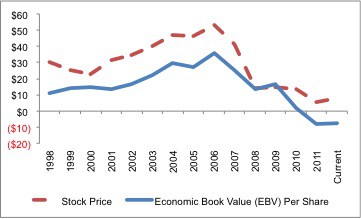

The Starbucks (SBUX) bandwagon is a big one. I am not on it.

Always flattered when a journalist, especially one as famous and respected at Mr. Taibbi, references my work. His article "Bank of America In Trouble?" incorporated the meat of my "Raising Fees Is A Desperate Measure: Sell BAC" article.

Year to date, Bank Of America (BAC) stock is up nearly 45% compared to the S&P at +about 8%. BAC stock has bounced back nicely after dropping precipitously at the end of last year.

I would call the 45% bounce a “dead cat” bounce because I expect the stock to fall right back to $5/share, where it bottomed last Thanksgiving, or lower.

When I ran across the recent article "270,033 pages later, a chance to catch our breath…", I could not help but admire footnoted.org's marketing moxy.

The article provides a count of the number of pages of 10-K filings that have poured in during the real earnings season. It also highlight a couple of the largest filings. At first glance, it is easy for one to assume that all of the 270,033 pages were also analyzed.

Recent news that Bank Of America (BAC) is considering jacking up its fees on basic checking accounts suggests the company is bad shape. As I wrote yesterday, I believe BAC stock is headed back to its lows and today’s news confirms my view that the expectations basked into the stock’s valuation are writing checks that the company cannot cash.