Regular readers know that we warned of the dangers of investing in Allbirds (BIRD) well before its IPO. In case you’re not aware, here’s our track record:

- In September 2021, pre IPO red flags and caution that the stock was significantly overvalued.

- In February 2022, don’t catch the falling knife that was Allbirds’ stock price.

- In October 2022, added Allbirds to our Zombie Stock list, which features stocks likely headed to $0.

- In November 2023, we closed our Danger Zone position after the stock outperformed the S&P 500 by 94% as a short. The stock wasn’t cheap, but it traded below $1 (pre-stock split) at the time, which left little upside left for a short position.

The Final Nail in the Coffin

On March 31, 2026, the company’s latest 10-K filing confirmed what our fundamental analysis showed years ago: the business is worth next to nothing.

Allbirds is selling, pending shareholder approval, substantially all its assets for just $39 million. The sale price is just 1% of its $4 billion peak valuation and less than 2% of its $2+ billion IPO valuation.

Additionally, the company’s latest 10-K includes a going concern disclosure, with management citing “substantial doubt about the Company’s ability to continue as a going concern” and stating plainly that it does not expect to continue operations after the Asset Sale closes.

We suspend the Stock Rating for any company that issues a going concern disclosure to ensure our clients are aware of the material development.

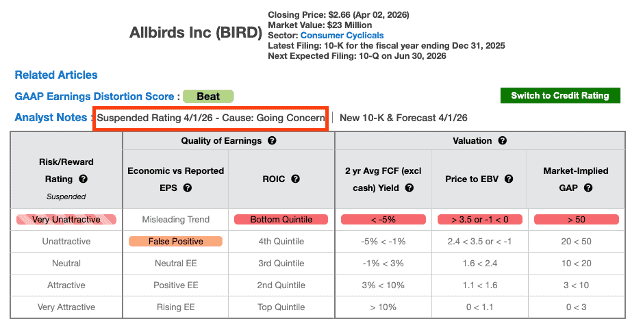

Figure 1: BIRD Going Concern Suspended Rating

Sources: New Constructs, LLC and company filings

As Lynyrd Skynyrd once sang, “This bird you cannot change.” Allbirds never did. Neither did the speculators who fell for the hype.

From $4 Billion to $39 Million

American Exchange Group agreed to pay $39 million in cash for substantially all of Allbirds’ assets and certain liabilities. The deal must be approved by stockholders and is expected to close in Q2 2026.

Let’s put that $39 million in perspective:

- Allbirds’ IPO valuation: ~$2 billion

- Peak valuation: $4 billion in November 2021, right after its IPO

- Current asset sale price: $39 million

- Value destruction: 99%+

Since our pre-IPO Danger Zone warning, investors who ignored our research and bought at the IPO price (or almost any other price) have watched their investment evaporate. In our initial pre-IPO report, we suggested the company was worth as little as $119 million, which turned out to be too generous.

Following the asset sale closing, Allbirds intends to dissolve and distribute whatever proceeds remain to stockholders after settling liabilities and transaction costs.

Equity investors will be lucky to recover a few pennies on their dollars.

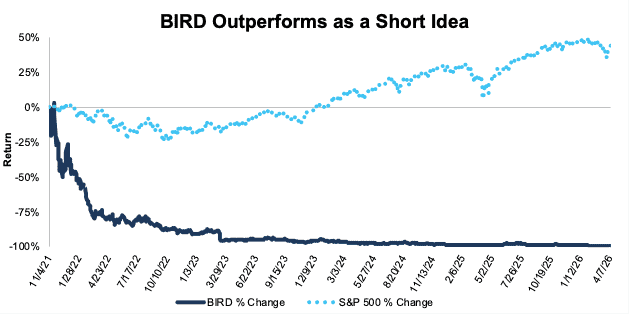

Figure 2: BIRD Performance Since IPO

Sources: New Constructs, LLC and company filings

Bonusing Executives to Supervise the Funeral

On March 30, 2026, Allbirds’ board approved an Executive Retention Plan. CEO Joseph Vernachio gets a one-time $500,000 payment to stay through closing. CFO Ann Mitchell gets $400,000.

That’s $900,000 in retention awards for executives to oversee the company’s liquidation. Shareholders who bought at IPO and held on will watch nearly $1 million go to management while their own holdings become worthless.

The irony is not lost on us.

The Deteriorating Fundamentals We Predicted

You may wonder, how could we have seen the downfall of Allbirds even before its IPO when Wall Street was touting the next great direct-to-consumer business model?

The answer is unconflicted, superior fundamental research. Our pre-IPO research showed Allbirds couldn’t scale profitably. Its costs were headed in the wrong direction, it faced stiff competition, and we predicted that the company’s losses would only get worse at it invested heavily in a costly brick-and-mortar strategy.

The business model we criticized in 2021 never improved, it just ran out of runway.

In Q1 2026, Allbirds closed all remaining full-price retail stores in the United States. The company now operates just two outlet stores in the US and two full-price stores in London.

The brick-and-mortar expansion failed, exactly as we predicted.

Profitability never improved either. The company currently earns a return on invested capital (ROIC) of -45% and its net operating profit after-tax (NOPAT) margin is -50%. The company’s economic earnings, or the true cash flows of the business, sit at -$92 million as well.

The Lesson: Fundamentals Always Matter, Eventually

Allbirds is a textbook case of what happens when investors chase narrative and ignore fundamentals. The sustainable materials, the DTC model, and the celebrity endorsements might look good in IPO investor presentations. But, none of it was enough to support the economics of the business.

Allbirds isn’t the only company we’ve warned investors about. In fact, we have many more calls like this one. Get access here.

This article was originally published on April 10, 2026.

Disclosure: David Trainer, Garrett O’Grady, and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.