There’s a popular saying amongst most schools of investing: “buy the dip!” This maxim can hold especially true for value investors, who look for companies that are trading cheaply relative to their book values. This is where we fall. We like to quantify the expectations embedded in companies’ stock prices to see if these expectations are rational. If the expectations are too pessimistic based on the company’s financials, we buy in.

Now that the first quarter of 2015 is behind us, it’s prudent to examine any new investment opportunities that have arisen over the past three months. That’s why we’re looking at the stocks that saw the biggest decline in 1Q15 to see if they warrant buying at their new, lower prices.

Click here to see the in depth analysis for only $9.99.

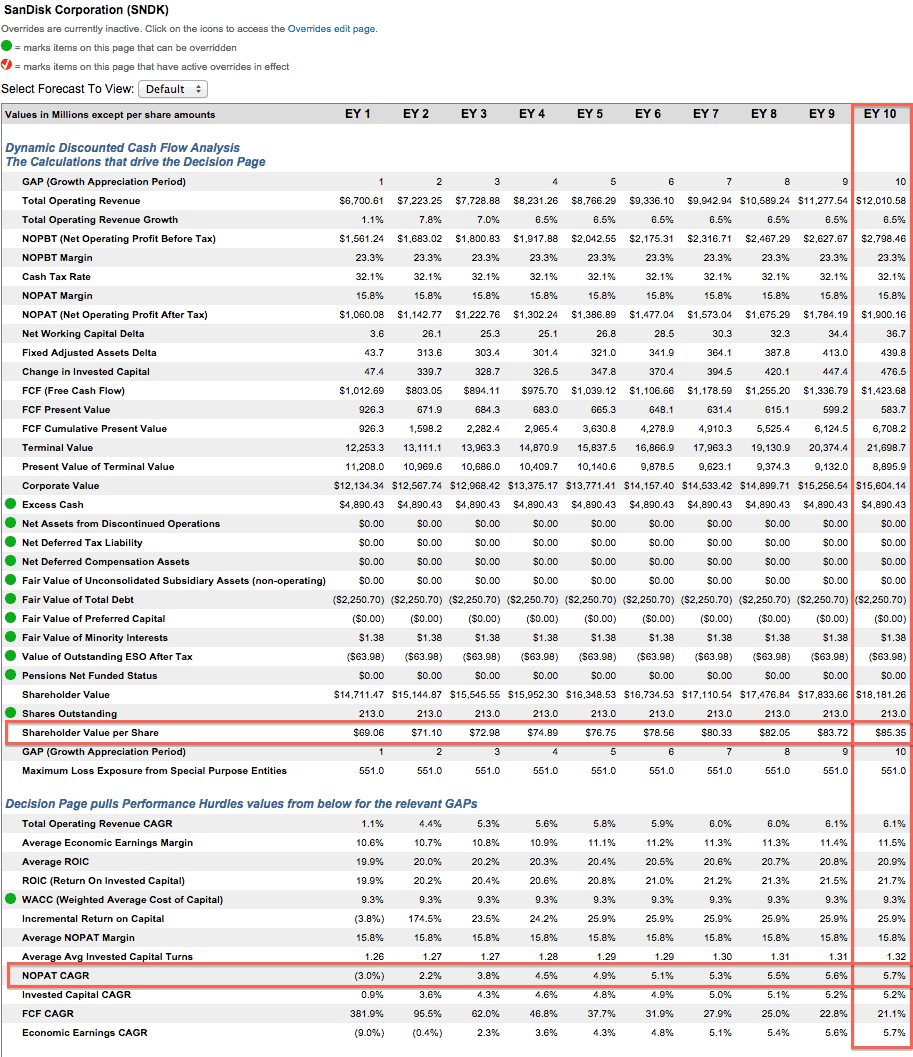

Data Storage Out of Room? — SanDisk Corp (SNDK)

SanDisk, maker of data storage products and services, “leads” this pack after dropping 35% in the first quarter of 2015. SanDisk makes and markets removable memory cards used in various portable consumer devices, solid state hard drives used in laptops and computers, and data storage products for use in enterprise markets. After revising guidance for its 1Q15 revenue, the stock plummeted more than 18%. This guidance revision comes on the heels of a similar move in the previous quarter’s earnings report. The company cited issues such as product delays, lower sales in enterprise markets, and lower pricing as the main reasons for the lowered revenue estimates. Obviously a company that keeps lowering revenue going forward is going to warrant a sharp decline in share price.

However, the decline in SanDisk may be largely overblown, as the concerns are not as serious when viewed long term. SanDisk is still one of the largest flash memory providers in the world, and the entire industry is expected to see significant growth moving forward. Despite increasing competition, SanDisk still boasts an impressive gross margin upwards of 50%, which is admittedly expected to see pressure going forward. Even if this huge margin contracts due to increased competition, it still leaves SanDisk ample room to operate and continue growing profits long term.

On top of its high margins, SanDisk has consistently grown its revenue over the last 10 years while weathering rapid advancements in technology. As emerging countries continue to get access to new technology and older storage technologies are replaced in developed markets, the usage of SanDisk’s products will continue to grow with the industry. These short-term worries have created an excellent opportunity in SanDisk shares.

Fundamentally, SanDisk is situated well to weather a decline in revenue while still delivering shareholder value. SanDisk had over $4.2 billion in current assets on its balance sheet and over $200 million in free cash flow at the end of 2014. Total debt sits at $2.2 billion, or 15% of the company’s market cap. SanDisk’s strong balance sheet should allow it to continue meeting its dividend payments, move forward with its share repurchase program, and also continue looking into avenues to grow the business even further.

SanDisk has grown net operating profit after tax (NOPAT) by 22% compounded annually over the past five years. While this may slow down going forward, SNDK’s current price is highly undervalued even when accounting for a lower NOPAT growth rate. The company’s return on invested capital (ROIC) was 23% in 2014, which places SanDisk in the top quintile of all companies we cover. SanDisk is more than efficient at deploying the capital invested into its business, and with a history of high ROIC, we expect more of the same moving forward. The company’s fundamental strengths lead SNDK to receive our Attractive rating.

At its new price of ~$67/share, SNDK has a price to economic book value (PEBV) ratio of 1.0. This ratio implies that the market expects SanDisk’s NOPAT to never meaningfully increase from current levels. The expectation that SanDisk would cease to grow profits in the high-growth flash memory industry ignores all realities of the market.

If we give SanDisk credit for only 6% NOPAT growth, compounded annually over the next 10 years, the stock is worth $85/share today — a 25% upside from current prices. The large decline in share price has created an opportunity not normally afforded in today’s market. This stock is certainly one to “buy on the dip.”

{kind=link}

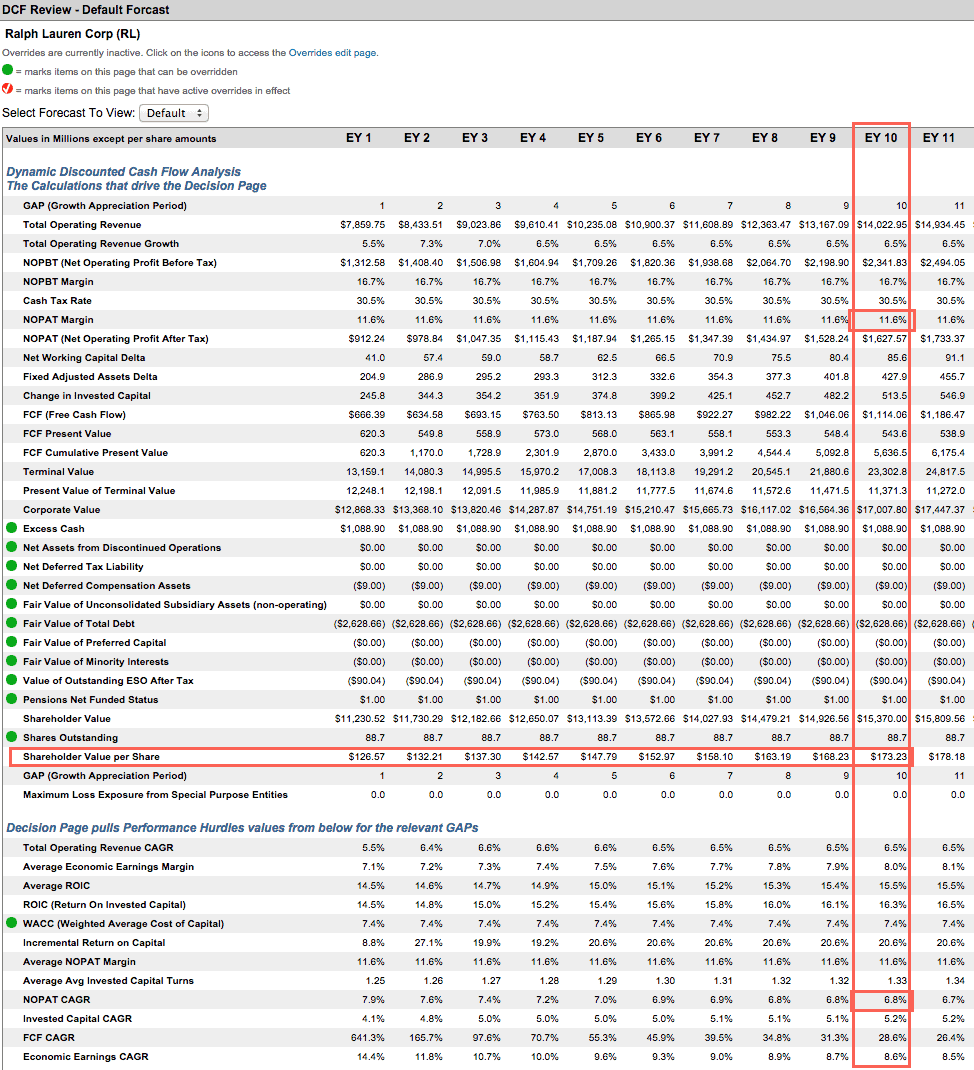

Going Out of Fashion? — Ralph Lauren (RL)

Ralph Lauren and his prancing horse logo are icons in the annals of American fashion. However, due to a number of factors, the Ralph Lauren Co.’s (RL) stock had an extremely rough start to 2015, and dropped 29% between January and March.

The luxury goods sector overall dropped in the first quarter due to concerns about consumer response to luxury pricing, especially in China, which saw luxury growth decline (-1%) for the first time ever in 4Q14. The strong dollar only added to investors’ concerns. Later on in the quarter, Ralph Lauren reported that it missed on both earnings and revenue in the last quarter of 2014, while revenue growth was up just modestly year over year, at 0.5% growth. Add the West Coast port shutdown into the mix, and it’s not surprising that RL declined in 1Q15.

However, RL’s 29% decline in the first quarter is almost certainly overdrawn, as the company’s financials are as good as they’ve ever been. Ralph Lauren’s revenue was up 5% on a TTM basis, but due to the impact of the strong dollar, NOPAT was $804 million and was flat for the period. While the dollar affected Ralph Lauren’s bottom line, it did not affect cash flow, and the company earned an all-time high of $833 million in free cash flow on a TTM basis.

All of these shifting financials have dragged down Ralph Lauren’s ROIC to 14% from its high of 16% in 2013. However, a 14% ROIC is nothing to sneeze at, and is in the top quintile of all Consumer Discretionary companies we cover. In fact, Ralph Lauren has a long history of generating returns on capital, and has had just one year of sub-10% returns on invested capital and just one year of revenue decline since 1998. This track record, along with the company’s $1.1 billion in excess cash and solid free cash flow, makes us confident that Ralph Lauren can weather the turbulence in the dollar’s value and the Chinese luxury goods market.

At its current valuation of $139/share, RL has a price to economic book value of almost 1.4, which implies that the market expects Ralph Lauren’s profits to grow by 40% for the rest of the life of the company. While this certainly isn’t cheap, it’s not particularly expensive either. If Ralph Lauren can grow profits by 7% compounded annually for the next 10 years, the stock is worth $173/share, a 24% upside. Note that Ralph Lauren has grown profits by 12% compounded annually since 1998, so this forward growth assumption is a conservative one. RL looks like an attractive pick for “buy the dip.”

{kind=link}

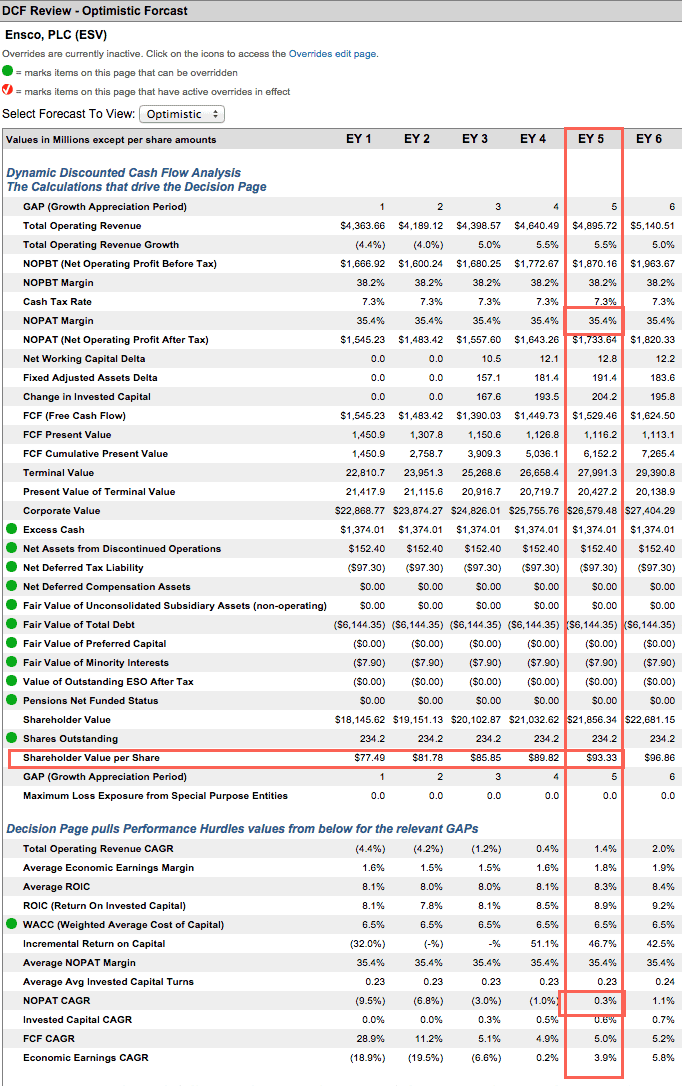

A Beaten Down Stock in a Beaten Down Sector — Ensco Plc. (ESV)

Over the last six months, energy prices have continued to decline, and investor sentiment has grown increasingly pessimistic regarding the energy sector in the United States. Adding to this uncertainty are international policy concerns with oil producing nations such as Iran and Saudi Arabia. Although these concerns are warranted, Ensco’s (ESV) stock has seen a disproportionate decline.

Just how badly is the market undervaluing Ensco, the world’s second largest offshore drilling company? First, the stock’s economic book value is $92 per share. This is the company’s value if it doesn’t grow profits from their current levels from the rest of its lifetime. When share price is taken into account, the ESV’s PEBV ratio is 0.4. The market is therefore expecting a 60% decline in NOPAT.

While in the short term this kind of decline may occur, over the long term this kind of expectation is unreasonable. Over the last 10 years, Ensco has grown NOPAT by 6% compounded annually. At the moment, Ensco receives our Very Attractive rating due to its 9% ROIC and a high 16 % free cash flow yield. Despite this consistent performance the stock has declined from $53 in 2010 to its current price of $23. This pessimism has also been driven by analysts who have forecasted consensus revenue declines of 4% for Ensco for each of the next two years.

However, even if Ensco fails to grow at all going forward, the stock I still worth a substantial amount more than $23/share. If we expect that the company can earn the same NOPAT in five years that it earned in 2014, the stock is worth $93/share today — a 300% upside from current levels. Given Ensco’s healthy balance sheet and $1.2 billion in free cash flow in 2014, it seems pessimistic to forecast the company’s profits permanently declining by 60%, as the stock’s current valuation implies. At a valuation this cheap and with a track record this strong, it’s hard not to justify taking a serious look at ESV.

{kind=link}

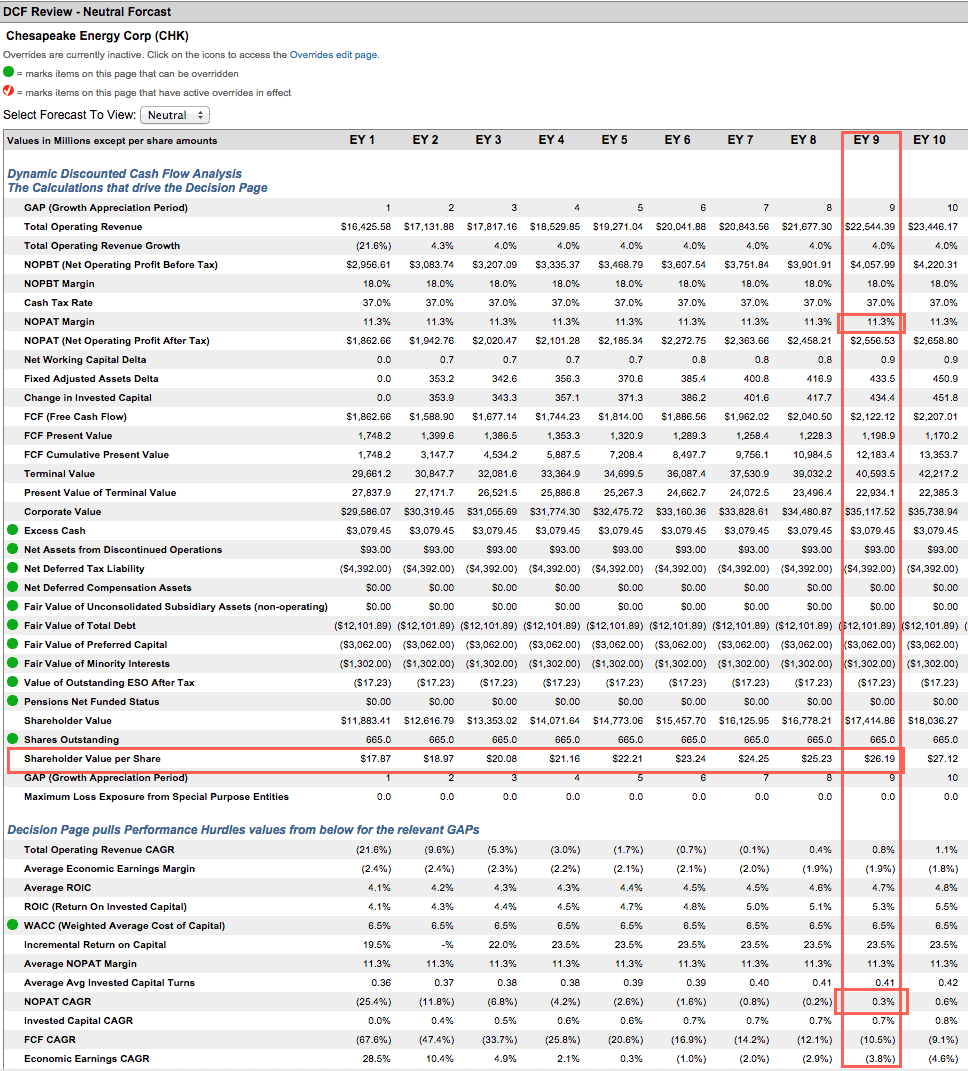

A Bet on the Energy Sector With Carl Icahn — Chesapeake Energy (CHK)

Much like its sector peer above, Chesapeake has had a rough several months in the Energy sector. During the first quarter of 2015, shares of Chesapeake Energy declined by a startling 27%. During this same period, the iShares U.S. Oil & Gas Exploration & Production Index, has actually increased by 3%.

As the second largest natural gas producer in the United States, Chesapeake Energy is heavily dependent on oil and natural gas prices to drive profitability. With WTI crude oil prices hovering around $50, and natural gas prices at around $2.80, investors are concerned with near-term company performance in a declining market. To provide perspective, in February 2014 WTI crude was priced at over $100 per barrel and natural gas was at $5.56.

To deal with this, Chesapeake is monitoring financial aspects within its direct control such as capital planning and overall activity levels. Although Chesapeake cannot directly control oil prices, it can control expenses and capital expenditures. Two weeks ago on March 23, Chesapeake announced that it would be spending $500 million less on capital expenditures due to weak commodity pricing. This represents nearly 25% of the company’s 2014 capital expenditures.

The company has made steady progress in managing its balance sheet by reducing drilling and completion expenditures by nearly $1 billion since 2013. The company also continues to divest assets that are not critical to core operations. For example, according to the company’s Feb. 25, 2015 conference call, Chesapeake divested two shale assets worth roughly $5 billion. This transaction represented only 7% of production but nearly 40% of the company’s market capitalization at the time. This is important as the company now has more financial flexibility to better manage the cyclical downturn in oil prices. Currently the company has a $4 billion cash balance, over triple its 2013 cash balance of $837 million. Chesapeake obtained another $4 billion capital cushion in the form of a new, unsecured credit facility. Chesapeake’s liquidity position is therefore very favorable. The company is not only positioned well in the current price environment, but also can take advantage of favorable investment opportunities within the industry.

Finally, insider trading from company executives has been very favorable recently. Insiders can sell their holdings for any number of reasons. However, insiders buy for only one reason: they want to make money. Insider purchases have been very positive for the company. Archie W. Dunham, chairman of Chesapeake’s board, purchased 1 million shares of common stock according to a March 31, 2015 filing, worth nearly $14 million.

Notable investor Carl Icahn has also increased his stake in the company to 73 million shares. High insider transactions, a large purchase from the Chairman, and a significant investment from an investor recognized for his ability to properly ascertain value are all positives for the stock.

In addition to the improved liquidity position and favorable insider purchases, the company has a very compelling valuation. Chesapeake has managed to generate strong NOPAT growth over the last decade at 14% compounded annually. This strong growth has occurred during varying oil and gas prices and macroeconomic cycles.

Due to the cyclical energy decline currently underway, analysts project revenue declines of 22% next year and revenue increases of 4.3% the following year. Given the uncertainty with future oil and gas prices this seems like a reasonable estimate. Assuming a revenue decline of 22% next year, and NOPAT growth of just 0.3% compounded annually for the next 9 years, the stock is worth $26/share, a 73% upside from current valuations. CHK is extremely cheap at the moment and definitely a long-term hold.

{kind=link}

No One Wants Our Toys Anymore? — Mattel Inc. (MAT)

Mattel (MAT), the longtime kids toy producer, makes our list after dropping 27% in the first quarter of 2015. Mattel makes well-known children’s toys under the Barbie, Hot Wheels, Fisher Price, and American Girl brands. Unfortunately for Mattel, 4Q14 earnings were largely disappointing, and the continued confusion within the company has created a further decline in share price. Yearly revenues declined 7% in 2014 with fourth quarter results dragging even further. Particular weakness was seen in the Barbie segment, which saw revenue decline 12% year over year, and the Fisher Price segment, which saw revenue decline 11%. Gross margin and operating margin also declined, with operating nearly halving to 12% in 4Q14.

Unfortunately for Mattel, the company’s issues run deeper than just one bad quarter. The Barbie sales decline marks the third consecutive year in which the brand’s sales declined year over year. For the entire year, Barbie sales were down 16% over 2013, even worse than the 12% decline for 4Q14. As other toy makers like Hasbro have taken market share from Mattel, there have been no clear signs of how Mattel plans to reverse course. In fact, management shakeups have become a normal event at Mattel. Mattel’s interim CEO was made permanent in early April; however this announcement comes on the heels of Mattel hiring the company’s prior CEO as a consultant and paying him more now than as CEO. Also, Mattel’s CCO and COO have also been shuffled in the past month. Executive shakeups can be a positive for a company in decline, but the lack of clarity in positions and strategy makes Mattel’s moves easy to question.

Adding to investors’ worries, Mattel recently lost the rights to produce Disney Princess products to rival Hasbro, a lucrative contract that saw enormous upside potential after the release of the blockbuster Disney movie Frozen. While Mattel still holds the rights to produce Disney Princess dolls through 2015, moving beyond that, it remains unclear how Mattel aims to make up for the lost revenue. For a few years now, Mattel has not done much innovating. Meanwhile its competitors have slowly taken their market share, and it will be up to Mattel to determine the correct response to return to its former glory.

Fundamentally, Mattel is neither good nor bad. NOPAT declined 42% year over year in 2014, but this was after five consecutive years of near double-digit growth. The company’s ROIC fell to a 14-year low of 7% in 2014. Falling profits and ROIC do not bode well for investors unless Mattel has a solid plan to reverse course. Mattel does have over $2.5 billion in total debt, which is 31% of its market cap, but also $3.1 billion in current assets and over $140 million in free cash flow for 2014.

After the large decline in price, MAT’s valuation does look more attractive. However, issues highlighted above such as its low ROIC, low free cash flow yield, and negative NOPAT growth earn this stock our Neutral rating. Given the management issues detailed above, as well as the lack of a clear plan to return to growth, Mattel does not appear to be stock to “buy on the dip.”

At its current price of ~$24/share, Mattel has a PEBV ratio of 1.2, which implies that the market expects the company to grow NOPAT by 20% over the life of the company. While this expectation may seem low, unfortunately Mattel has given no reason for investors to believe that is currently possible without drastic changes in the business.

André Rouillard, Allen Jackson, and Kyle Guske II contributed to this report.

Disclosure: David Trainer, Allen Jackson, André Rouillard and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report

Photo credit: Abdulla Al Muhairi (Flickr)