We published an update on this Danger Zone pick on August 3, 2021. A copy of the associated Earnings Update report is here.

Check out this week’s Danger Zone Interview with Chuck Jaffe of Money Life and MarketWatch.com.

Tesla Motors (TSLA) is in the Danger Zone this week. Up over 350% in 2013, the electric automaker has dominated headlines and made a lot of investors very happy (and a lot of shorts very angry). At ~$150/share, it’s no secret that the stock is expensive. What most investors don’t realize is that there are some significant details buried in the footnotes of TSLA’s SEC filings that materially affect the outlook for shareholders in the company.

The Illusion of Profitability

TSLA’s impressive run began with its first quarter GAAP net income of over $11 million. Prior to 1Q13, the company had never reported a quarterly profit. Unfortunately for enthusiastic investors, TSLA’s impressive first quarter comes with some caveats. For one, the company recorded $68 million in revenue (12% of total revenues) from the sale of Zero Emissions Credits, a revenue stream that looks set to decline going forward.

Furthermore, $10.7 million of TSLA’s pre-tax income came from the elimination of a Department of Energy warrant liability after TSLA paid off its loan from the DOE ahead of schedule.

Most investors recognized these non-operating items and adjusted them out of their projections going forward.

However, very few investors seem to have recognized that a further $6.4 million in income was due to changes in foreign-currency holdings. Especially impactful was the devaluation of the Japanese yen, which shrunk TSLA’s liabilities that were denominated in that currency.

The foreign currency gain, along with the elimination of the DOE warrant liability, were bundled under “other income” and only described on page 28 of TSLA’s Form 10-Q. Without the benefit of these two non-recurring items, TSLA does not report the first quarter profit that made investors so bullish. Another $1.6 million in foreign currency gains also helped TSLA’s better-than-expected second quarter.

Who Benefits From the Hype?

Investors only looking at debt overlook other liabilities a company has on its books that keep future profits from the pockets of shareholders. For a startup like TSLA, employee stock option liabilities are worth your attention.

GAAP standards have required companies to record compensation expenses related to employee stock options since 2006, so investors don’t have to worry about companies hiding that expense (though TSLA does exclude stock option expense in its non-GAAP earnings). However, investors often ignore the dilutive potential of outstanding stock options to their current shares.

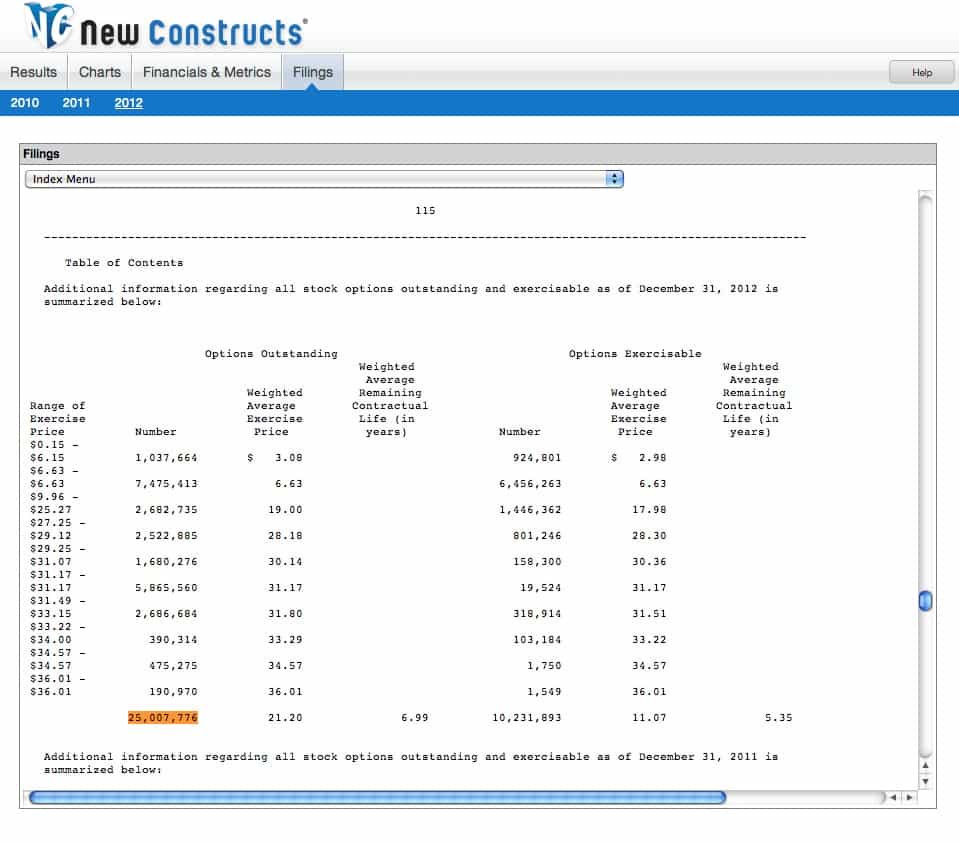

As of December 31, 2012, TSLA had 25 million outstanding options. Using the Black-Scholes model, those shares would be worth ~$3.1 billion (18% of the market cap) at TSLA’s current valuation of ~$150/share. Of course, some of those options have already been exercised recently. We found about 300,000 options exercised by employees and 500,000 options exercised by Goldman Sachs (GS). Elon Musk also bought a further 600,000 shares from the company at ~$90/share.

{kind=link}

However, the company is not making it easy to figure out exactly how many options have been exercised. The numbers in their latest 10-Q filing do not add up. First, the 10-Q shows the number of common shares outstanding has increased from 114 million to 121 million since the filing of TSLA’s 10-K while the number of outstanding options dropped from 25 million to 250 thousand. Including the exercised options detailed above, the 10-Q filing leaves about 17 million in options unaccounted for.

The company has not yet responded to our inquiry on this discrepancy. But I think it is safe to say that some TSLA and Wall Street insiders have profited quite nicely from the stock’s run-up.

Investors need to consider who is benefitting from the stock’s massive rise. Corporate insiders who can exercise their options to buy at $10 a share and sell to a retail investor at $150/share or more are having a great year. TSLA is full of hype this year, and no one has more incentive to promote that hype than those on the inside of the company.

The run-up in TSLA stock looks similar to a pump and dump scheme right now as other writers have noted. As I wrote recently, investors should protect themselves from Wall Street insiders.

Stock Is Way Overvalued

TSLA is priced for enormous profit growth despite not having demonstrated consistent profitability. The company currently has a market cap 50% higher than Harley Davidson (HOG) despite the fact that its projected revenue for 2013 is 1/3 of HOG’s and its goal of a 25% gross margin by the end of this year is one-half of what HOG achieved last year.

TSLA’s margins are going to be constrained by the amount of competition they will face in the mass market that they are trying to enter. TSLA can charge a premium price for its current models because no one else offers an electric car with the performance specs of a Model S.

As TSLA moves down market, Ford, GM, Chrysler, and other companies have huge scale advantages that enable them to undercut TSLA on price. Already this year we’ve seen price cuts from GM and Nissan on their electric vehicles, and Chrysler’s CEO admitted that the company loses money on every electric car it sells.

TSLA could definitely carve out a profitable segment for itself in the market, but it’s hard to believe they will be as dominant a player as their stock price suggests. To justify a valuation of ~$150/share, TSLA would need to achieve the margins of HOG within five years and grow revenue at 35% compounded annually for 10 years. Maybe they hit one of those expectations, but hitting both is not likely.

The $50 price mentioned in my Danger Zone interview and highlighted by MarketWatch also requires hard-to-believe future cash flow achievements. Per my model here, TSLA would have to achieve margins on par with General Motors (GM) and Ford (F) and grow revenues at 35% compounded annually for 10 years to justify $50. Again, maybe they hit one of those expectations, but hitting both is not likely.

{kind=link}

The bottom line is that this stock has gone up for all the wrong reasons. It started its surge due to a misleading profit, then benefited from a short squeeze and more unusual gains in the second quarter. None of that is sustainable. The short squeeze is dying down, and the accounting trickery cannot go on forever. TSLA is like Wile E. Coyote running out in midair. Once the market looks down and realizes there’s nothing supporting that lofty valuation, it could fall a long way.

I would not recommend investors try to short TSLA just yet. The stock still has a lot of momentum and could continue to go higher despite its poor fundamentals. Trying to short a high momentum stock is just asking for trouble. As the saying goes, “The market can stay irrational longer than you can stay solvent.”

However, investors should avoid TSLA, and those holding the stock should sell and enjoy their profits. The problem with an irrational stock is that there’s no way to predict when it will be rationally priced again. Just know that when the market comes to its senses—probably once all those option holders have cashed in—those holding TSLA are going to lose a lot of money.

Avoid These Funds

First Trust NASDAQ Clean Edge Green Energy Index Fund (QCLN) and RidgeWorth Funds: Aggressive Growth Stock Fund (SAGAX, SCATX) both allocate over 5% of their assets to TSLA and earn my Dangerous rating. Investors should steer clear of these funds, as they both would take a heavy hit from a large downward move in TSLA.

Sam McBride contributed to this article.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.

3 replies to "Danger Zone 8/12/13: Tesla Motors (TSLA)"

Inasmuch, as you say, the stock still has a lot of momentum, wouldn’t it be better to advise holders to put in a Trailing Stop Loss order, rather than sell right now?

I am quoting this post, thoughts? “RE: http://wp.me/p2BJXK-b2

One of the people where I work has a Tesla, we saw the articles about multiple Tesla fires at http://wp.me/p2BJXK-b2

I have now read that many Tesla owners have complained of fire incidents in their blogs. Do Tesla batteries blow up after they get wet? Don’t park your Tesla anywhere near your home or you may find your house burned down.

P. Summers:

I don’t have the technical expertise to comment on the risk of fires with Tesla batteries, but the market’s reaction to the news (down 15%) shows how vulnerable a story stock like TSLA can be. One bit of news that contradicts the bullish narrative can take a big chunk out of the stock’s value.