Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and MarketWatch.com.

Each quarter we rank, the 12 investment styles in our Style Ratings For ETFs & Mutual Funds report. For the second quarter of 2016 rankings, we noticed a new trend: in five of the past six quarters, the Mid Cap Growth style has received our Dangerous rating. Within that group, we found a particularly bad fund.

Of the five worst funds in this style, one in particular stands out for the high level of its assets under management (AUM). When a low quality fund has low AUM, we are comforted that investors are avoiding the poor fund. But, when a fund has over $3.4 billion AUM and receives our Very Dangerous rating, it’s clear that investors are missing pertinent details. The missing details are deep analysis of the fund’s holdings, which is the backbone of our ETF and Mutual Fund ratings. After all, the performance of a fund’s holdings drive the performance of a fund. As such, Franklin Small-Mid Cap Growth Funds (FRSGX, FRSIX, FSMRX) are in the Danger Zone due to alarmingly poor holdings and excessively high fees.

Poor Holdings Makes Outperformance Unlikely

The only justification for mutual funds to have higher fees than ETFs is “active” management that leads to out-performance. How can a fund that has significantly worse holdings than its benchmark hope to outperform?

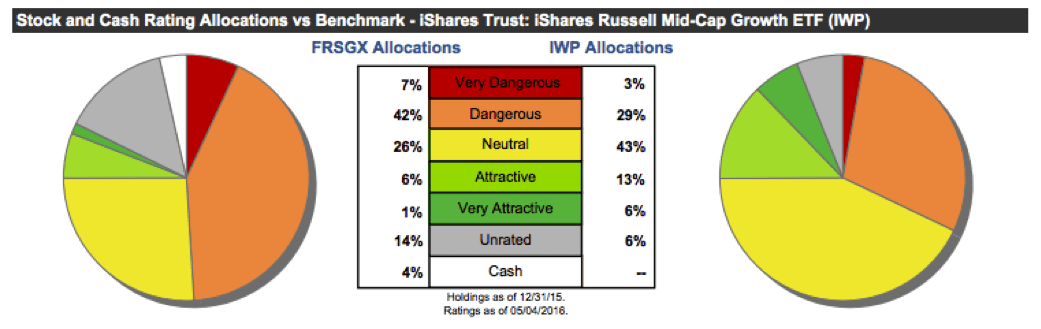

Franklin Small-Mid Cap Growth Fund investors are paying higher fees for asset allocation that is much worse than its benchmark, the iShares Russell Mid-Cap Growth ETF (IWP).

Per Figure 1, at 49%, Franklin Small-Mid Cap Growth Fund allocates more capital to Dangerous-or-worse rated stocks than IWP at just 32%. On the flip side, IWP allocates more (at 19% of its portfolio) to Attractive-or-better rated stocks than FRSGX at only 7%.

Figure 1: Franklin Small-Mid Cap Growth Fund Portfolio Asset Allocation

Sources: New Constructs, LLC and company filings

Furthermore, 7 of the mutual fund’s top 10 holdings receive our Dangerous rating and make up over 12% of its portfolio. Two stocks in particular raise enough red flags that we have featured them previously: Constellation Brands (STZ) and Willis Towers Watson (WLTW).

If Franklin Small-Mid Cap Growth Fund holds worse stocks than IWP, then how can one expect the outperformance required to justify higher fees?

Chasing Performance Is Lazy Portfolio Management

Franklin Small-Mid Cap Growth Fund managers are allocating to some of the most overvalued stocks in the market. We think the days where investing based on past price performance (or momentum) leads to success have passed for the foreseeable future. Managers have to allocate capital more intelligently, not based on simple cues like momentum.

The price-to-economic book value (PEBV) ratio for the Russell 2000 (IWM), which includes all small and mid cap stocks, is 3.5. The PEBV ratio for FRSGX is 4.6. This ratio means that the market expects the profits for the Russell 2000 to increase 350% from their current levels versus 460% for FRSGX.

Our findings are the same from our discounted cash flow valuation of the fund. The growth appreciation period (GAP) is 32 years for the Russell 2000 and 22 years for the S&P 500 – compared to 50 years for FRSGX. In other words, the market expects the stocks held by FRSGX to earn a return on invested capital (ROIC) greater than the weighted average cost of capital (WACC) for 18 years longer than the stocks in the Russell 2000 and 28 years longer than those in the S&P 500, home of some of the world’s most successful companies.

This expectation seems even more out of reach when considering the ROIC of the S&P is 18%, or double the ROIC of stocks held in FRSGX.

Significantly higher profit growth expectations are already baked into the valuations of stocks held by FRSGX.

Beware Misleading Expense Ratios: This Fund Is Expensive

With total annual costs (TAC) of 3.36%, FRSGX charges more than 84% of Mid Cap Growth ETFs and mutual funds. Coupled with its poor holdings, high fees make FRSGX even more Dangerous. More details can be seen in Figure 2, which includes the two other classes of the Franklin Small-Mid Cap Growth fund that receive our Very Dangerous rating. For comparison, the benchmark, IWP charges total annual costs of 0.28%.

Figure 2: Franklin Small-Mid Cap Growth Fund Understated Costs

Sources: New Constructs, LLC and company filings.

Over a 10-year holding period, the 2.42 percentage point difference between FRSGX’s TAC and its reported expense ratio results in 27% less capital in investors’ pockets.

To justify its higher fees, the Franklin Small-Mid Cap Growth Funds must outperform its benchmark by the following over three years:

- FRSGX must outperform by 3.1% annually.

- FRSIX must outperform by 1.71% annually.

- FSMRX must outperform by 1.15% annually.

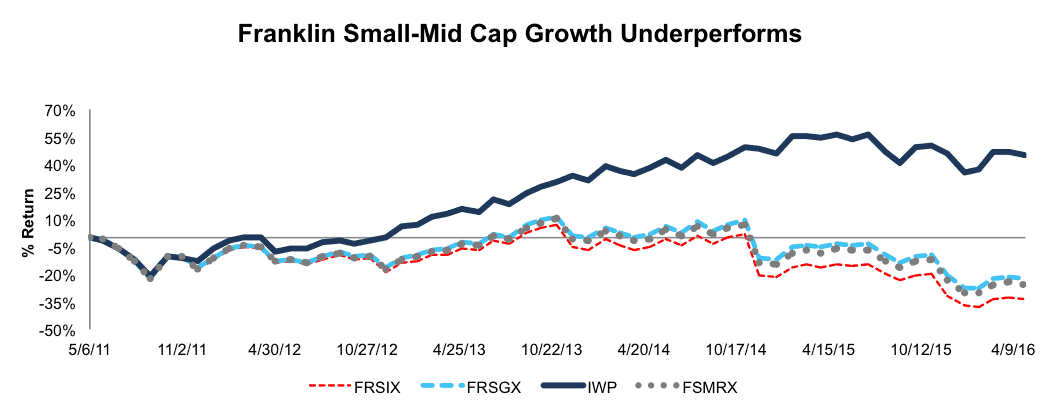

The expectation for annual out performance gets harder to stomach when you consider how much the fund has underperformed already. In the past five years, FRSGX is down 24%, FRSIX is down 35%, and FSMRX is down 27%. Meanwhile, IWP is up 44% over the same time. Figure 3 has more details. The bottom line is that with such high costs and poor holdings, we think it unwise to invest in the belief that these mutual funds will ever outperform their much cheaper ETF benchmark.

Figure 3: Franklin Small-Mid Cap Growth Funds’ 5 Year Return

Sources: New Constructs, LLC and company filings.

The Importance of Proper Due Diligence

If anything, the analysis above shows that investors might want to withdraw most or all of the $3.4 billion in Franklin Small-Mid Cap Growth Funds and put the money into better funds within the same style. The top rated Mid Cap Growth mutual fund for 2Q16 is Congress Mid Cap Growth Funds (IMIDX and CMIDX). Both classes earn a Very Attractive rating. The fund has only $375 million in AUM and IMIDX and CMIDX charge total annual costs of 0.95% and 1.23% respectively, both less than half of what FRSGX charges. Without analysis into a fund’s holdings, investors risk putting their money in funds that are more likely to underperform, despite having much better options available.

Without proper analysis of fund holdings, investors might be overpaying and disappointed with performance.

This article originally published here on May 9, 2016.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.

Click here to download a PDF of this report.

Photo Credit: Wirawat Lian-udom (Flickr)