After months of delay, the Department of Labor’s fiduciary rule will finally go into effect on June 9. Labor Secretary Alexander Acosta confirmed the rule’s implementation on Monday in a Wall Street Journal op-ed.

The move surprised many observers that expected the Trump administration to kill this Obama-era rule, but it’s always been the case that those opposed to the fiduciary rule were fighting a losing battle. All the debate over the rule only raised investors’ awareness of the potential conflicts in the investment industry and heightened their desire for a fiduciary level of service. As Michael Kitces recently tweeted “…Can’t unring this bell now…”

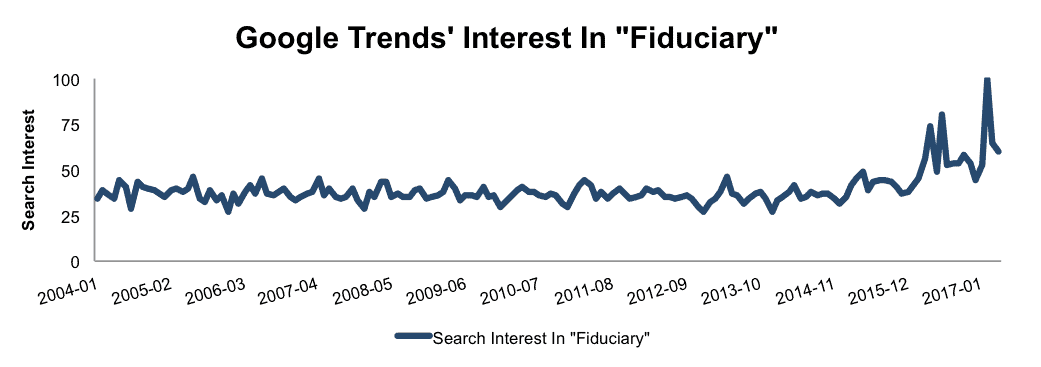

Interest In Fiduciaries Driven To New Highs

Figure 1 provides the data behind the term “fiduciary” reaching all time highs as measured by Google Trends.

Figure 1: Interest In “Fiduciary” Remains Elevated

Sources: New Constructs, LLC and company filings.

Major wealth management firms [e.g. Fidelity and Bank of America Merrill Lynch (BAC)] announced sweeping changes to comply with the fiduciary rule months ago. Acosta must have realized that a further delay of the rule wouldn’t stop the industry from moving towards the fiduciary standard.

Investors are better served, and the investing business has more integrity, when the fiduciary level of service is applied. Investors want advice that is aligned with their best interests. No adviser wants to be perceived as not having the clients’ best interests top of mind.

Fiduciary Duty of Care Is As Important As the Duty Of Loyalty

Most of the changes brought about by the fiduciary rule so far have focused on the Duty of Loyalty—ensuring that advisors don’t charge excessive fees and avoid conflicts of interests. With the rule now set to take effect, we expect firms to start paying more attention to the Duty of Care. By law, a fiduciary must act with “care, skill, prudence, and diligence.”

Failure to demonstrably adhere to the duty of care could leave firms and advisors open to class action lawsuits. More than ever, advisors need to make sure their investment advice is backed up by diligent research. More specifically, advisors need research that is:

- Comprehensive. All relevant publicly available (e.g. 10-Ks and 10-Qs) information has been diligently reviewed, including the footnotes and the Management’s Discussion & Analysis (MD&A).

- Objective. Clients deserve unbiased research.

- Transparent. Client should be able to see how the analysis was performed and the data behind it.

- Relevant. There must be a tangible, quantifiable connection to stock, ETF or mutual-fund performance.

That’s a tall order, but it’s not impossible

Technology Is The Key Solution To Mandates To Cut Costs And Maintain Quality

In the past, it had been nearly impossible to provide diligence at scale. Today, Robo-Analyst technology solves the scale challenge and enables a higher level of diligence at such a low cost that ignoring it is unethical.

More of the biggest names in the financial industry, such as BlackRock (BLK) and JPMorgan Chase are embracing technology to improve investment decision-making.

We think investors deserve not only a fiduciary level of service, but also the latest that technology can offer.

This article originally published on May 24, 2017.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.